We hope you are enjoying summer and sunshine. Unfortunately, the financial markets remain stuck in a “storm”. After the difficult first quarter, pain accelerated during the 2Q. There was no place to hide; bonds and stocks together experienced a 2nd consecutive negative quarter each – a somewhat rare occasion.

Against this backdrop and with so many big worries without easy or quick resolution (inflation, Russia/Ukraine, Fed that is intentionally trying to slow the economy to balance supply & demand), it can become challenging to maintain a longer-term perspective. Our newsletter this quarter provides the following context:

- “GIGO” – Do your best to control the type of information you consume, as well as how you react to it. What version of “GIGO” will you be?

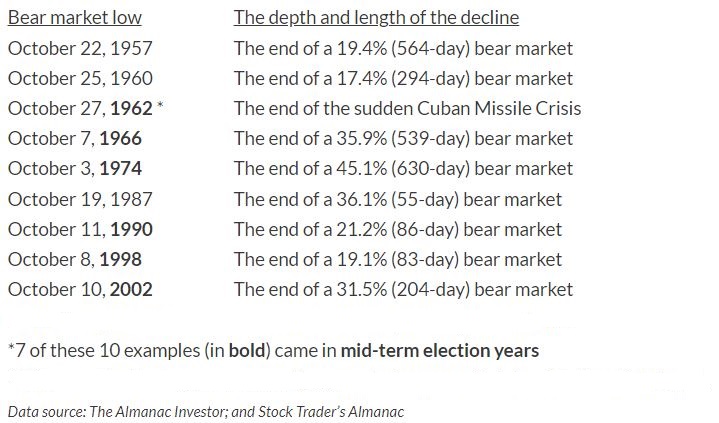

- “The World Changed” – A review of market action so far in 2022 and context from history providing clues to what might be expected from here.

- “Bills to Pay” – The “cost” of fiscal and monetary stimulus pursued by governments around the globe in response to the Great Lockdown is being paid in 2022. How is the bill being paid and how long will that last?

- “iPod, iPhone, iPad… now the I Bond” – What are I Bonds, and are they for me?

A printer-friendly version of the newsletter, including benchmarking and fund performance data, can be obtained here: Q2 Nvest Nsights.

We realize how troubling is the current market environment and are here for you. We continue to monitor the backdrop, and be intentional about managing portfolios tactically. Please do not hesitate to call, email with questions, or to coordinate a time to visit together.

Continue reading→