Do you know, or ever meet, a Mr. Kadiddledopper? If so, you’d surely remember. He is a man of opposites. Kadiddledopper is a guy who lives in a small town, whose house looks badly in need of painting; yard needs mowing; landscaping is overgrown with tall weeds woven in; and a broken picket fence with peeling paint. Even his clothing announces a reclusive personality. The town folk don’t know how to relate to him. Mr. Kadiddledopper speaks in opposites. Understanding his talk is challenging and confusing. “Bye. Sure is cold today,” he says when greeting you on a humid 90 degree day. Caution when following his directions – turn left when he says go right; stop means go, and go means stop; up-town means down-town. When he answers “no,” he really means yes, but a most peculiar exception is “Yes” always means yes. Is there such a real-life person? Not sure; I created my fictious guy for humorous “fun” with young grandkids. Ever struggle with a toddler who says “no” to everything? Try instructing them that “no” means “yes,” and “yes means “yes.” You may still be frustrated and certain that opposites don’t work. “Don’t try it” with your spouse, and definitely not in public! You will discover it’s easy at first and gets harder with practice. [Italics will denote opposites to avoid confusion.]

“Dog Gone ’22!” – Nvest Nsights Q4 Newsletter

We hope you enjoyed a nice holiday season and are entering 2023 in good health and spirits, optimistic for what the year ahead might bring. For many investors that may feel difficult given the stormy market environment; yet we should each resolve not to give way to unreasonable pessimism either. This quarter we offer several items in our newsletter:

- “Dog Gone ’22!” – some of the most friendly words we could come up with to convey the frustration that most probably feel for the investing experience over the last year, but more importantly a quick review of the factors that influenced both the stock and bond market.

- “Snoozer Cruiser – Dreams for ’23” and “Portfolio Tactics” – We share the key items we are watching; what they might mean for investors in the year ahead; and how we are strategically positioning portfolios.

- “The Upside to Rate Hikes & Secure Act 2.0” – The Fed’s aggressive rate increases last year are not all bad… we share some ideas for how(where) you can get paid significantly more on your cash. Also, some quick highlights about the just passed Secure Act and how it may impact you.

Click here for the Printer-friendly PDF version including benchmarking and fund data

We hope these updates are helpful and encourage you to review. Please do not hesitate to call or email with questions, or to coordinate a time to visit together.

“The Upside to Rate Hikes” and SECURE Act 2.0

As shared throughout 2022, the Fed’s battle with inflation is the dominant force driving challenges in both the stock and bond markets. In addition to a challenging market, borrowers are feeling pain in the form of higher rates on mortgages, credit cards, auto loans, etc. These are the painful realities of reversing the Fed’s previous interest rate (ie. free money) and quantitative easing (QE) policies.

There is an attractive positive to higher interest rates however. For savers, cash is finally returning a “reasonable” rate… if you know where to look! Continue reading

“Horsefeathers! #$*^” – December Market Commentary

Ever hear someone say “horsefeathers”? It’s peculiar, so when it’s exclaimed a puzzled look often occurs. “Horsefeathers” is politely spoken when something did not go right – like I made a bad pickleball shot or missed an easy putt; or a goofy mistake occurred that could be anticipated. It’s amusing that I used this word for years and decades. As I considered using “horsefeathers” for the title of this commentary, I’m taken back by its age and origin – originating from the 1900s. It was used in several film gags from the Marx Brothers’ (Groucho, Zeppo, Harpo, and Chico) in “Fun in Hi Skule” (1932). “Horsefeathers” is slang for nonsense, foolishness, rubbish; indicates disbelief; like “Oh, that’s just horsefeathers, and you know it.” Sometime in the future maybe I’ll share about Mr. Kadiddledopper, or the idea of “enjoying your snooze cruiser.” [NOT, you may develop thoughts that I’m crazy.]

“Three-in-One” – November Market Commentary

Three-In-One: This commentary shares three shorter writings about the changing investment landscape. We hope presenting these ideas is helpful; we share our “radar screen” as we navigate these perplexing times. – Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

Price & Time

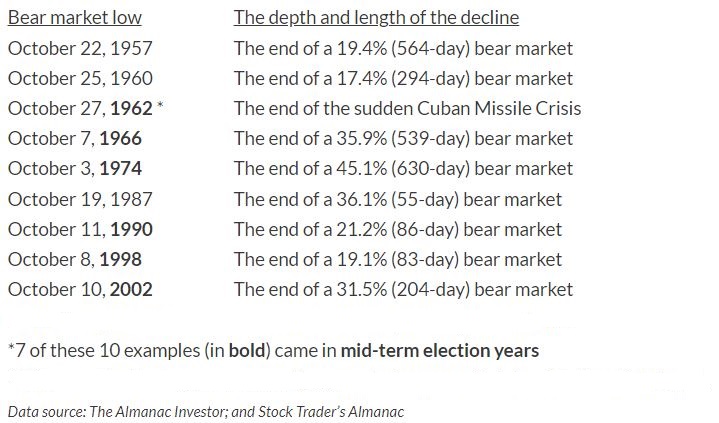

October financial market performance is often thought to be scary. That’s because some of the worst historical drawdowns occurred in October – 1929 and 1987. Interestingly a number of past bear markets also “died” in October of which several were also midterm election years.  Did you know, that September is more often a negative experience? October 2022 represents the single best performance month this year for stocks and client portfolios. It provides at least momentary respite from an otherwise trying YTD. The financial market system may be “voting” on several changing tidbits – inflation may be peak which some think should lead to a Federal Reserve pivot or pause (but that seems unlikely before 2023); company earnings are softer but better than expected; and upcoming mid-term elections may produce Washington gridlock, a condition markets generally prefer. The S&P500 advanced +8.1% during the month which generated positive client portfolio returns as well. YTD returns are still decidedly negative but improved from their quarter-end market lows.

Did you know, that September is more often a negative experience? October 2022 represents the single best performance month this year for stocks and client portfolios. It provides at least momentary respite from an otherwise trying YTD. The financial market system may be “voting” on several changing tidbits – inflation may be peak which some think should lead to a Federal Reserve pivot or pause (but that seems unlikely before 2023); company earnings are softer but better than expected; and upcoming mid-term elections may produce Washington gridlock, a condition markets generally prefer. The S&P500 advanced +8.1% during the month which generated positive client portfolio returns as well. YTD returns are still decidedly negative but improved from their quarter-end market lows.

“A Fresh Pair of Eyes”, “Always Late”, and “Times They Are a Changing” – Nvest Nsights Q3 Newsletter

We hope this note finds you and your family well and enjoying the beginning of Fall. Unfortunately, “enjoyable” is not a word we’d presently associate with the financial markets. The 3Q marked the first time since 1976 where both stocks and bonds were simultaneously negative 3 quarters in a row. As we interact with clients, some jokingly request that we not send this quarter’s update as they are doing their best to not focus closely. That may not be the worst strategy!

Our newsletter this quarter includes the following brief perspectives:

- “A Fresh Pair of Eyes” – 2022 remains all about rates (interest & inflation), and the dynamics are very different than when the year began.

- “Always Late” – What’s it like to always be late? Maybe we should ask the Fed. Recognizing that monetary policy always acts with a lag, it is understandable the market is concerned by the aggressive changes pursued over the last 9 months. Will the Fed go too far before we see the impact of their actions?

- “The Times They Are a Changing” – What’s the market saying about the future; what can help the markets stabilize and ultimately turn the negative trend around?

- “Buckets of Time – Dead, or Alive?” – With bonds experiencing their worst stretch in over 40 years, some may be wondering if the “buckets of time” approach remains appropriate in today’s environment.

The printer-friendly version of the newsletter, including benchmarking and widely held fund performance data, can be obtained here: printer-friendly PDF version.

With so many issues affecting the current investment climate, we hope that these updates are helpful. Please do not hesitate to call, email with questions, or to coordinate a time to visit together.

Buckets of Time – Dead or Alive?

Perhaps the most unsettling aspect about 2022 is not the degree to which the stock market is experiencing pain (not that unusual), but it’s the “double whammy” of also seeing meaningful depreciation in traditional safe fixed income. A recent headline, “The worst year in US history for the 60/40 portfolio”, underscores there being no place to hide in this bear market. During these challenging days, we continue to encourage maintaining a longer-term perspective. One way to do that is recalling “buckets of time” investing. Our well-seasoned clients may recall our “buckets of time” framework to unemotionally establish the investment objective (asset mix) for each account. This process helps align a client’s time horizon and purpose to investing the account.Continue reading

Special Market Update – “Financial Market Elevators”

On April 27 we shared a Special Market Alert entitled “Escalators, Not Elevators”. Why does investing in the stock market, also add the bond market this year, feel like taking an escalator up, and riding an elevator down? Rising markets seem to be slow upward climbs, like an escalator; the rise occurs over extended time (months and years). But a correction or bear market, defined as a decline of -20% or more, occurs quickly (days and weeks, or months), like riding an elevator down. It seems to take a year to earn 10% in a rising market, but a few days to lose 10%. The elevator experience is always uncomfortable and creates anxiety. Yes, anxiety for us too as we manage client accounts with great care and effort.

Behind in the Count – September Commentary

Challenges exist for anyone playing sports when they are “behind in the count.” It’s a common experience for all athletes. Pressure builds for example, when batting with a count of “no balls and two strikes”, or behind in the football score 21-0. No competitor likes being behind, and extra effort may be pursued to bring about a positive winning outcome. Competitors strive for opportunity to succeed. Isn’t that the way with most things in life – pursue success, not failure?!

Navigating – August Commentary

GPS (Global Positioning Systems) offers us so much information about our surroundings and position in our world. On a recent vacation, we used the Navigate button in our Tesla to direct us efficiently to charging stations to help us reach our goal, home. The system calculated, like an aeronautical map used in aviation, our route with points of interest, neighborhoods, and terrain. It took a few moments as it planned our route to avoid heavy traffic, road construction, and other hazards attempting to ensure the car would have ample charge to reach the next point – charging stations and ultimately home. As we set off, the little red chevron that represented our car began following the planned route inching from right to left across our screen traveling west, north-west. The map was laid out in the standard position with North locked at the top. Our little chevron traversed across the fixed screen. I’m not fond of that traveling presentation. So, I pressed an icon on the top of the screen and suddenly our little chevron was fixed in the center pointing up (forward) as the map turned and moved under it! [Being simple minded, I prefer the chevron pointing the same direction as the car is traveling.] Which way was north, south, east west? Did I care? Cities, roads, and the world revolved around me! My real concern was that we were generally traveling west, north-west toward our goal, home.