Below, we submit our latest quarterly installment of Nvest Nsights. The first article reviews how chaotic, volatile, and disappointing was the market’s performance during 2018. But more important from our perspective is how swift selloffs like witnessed during the 4Q can cause one to suddenly feel confused and uncertain about the future; in these times it is most critical to step back and consider facts and fundamentals to avoid short-term action based on emotion. The article “Shilly-Shally Prone” reminds how long-term investment success accrues to those who remain steadfast to a repeatable and disciplined process. There are two remarkably similar historical backdrops which suggest it is very possible that present-day concerns could resolve or fade quickly against a still-sound economy, providing swift relief to recent market volatility here in 2019. Finally, “We Work With Rock Stars” provides insight into our investment selection philosophy with rationale motivating several portfolio adjustments being executed over recent weeks and as we enter the New Year.

The full printer-friendly version of our newsletter, including data tables for selected mutual fund and ETF performance as well as portfolio benchmarking, can be downloaded here: NVEST NSIGHTS 4Q.

CONFUSED? UNDERSTANDABLE

Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

Investing in 2018 did not conclude according to investor wishes. The year was chaotic, volatile, and disappointing. The end of year and the full year were primarily influenced by the Fed and tariffs. Either subject provided sufficient uncertainty to ramp up market volatility and investor worry about the future. It seems fitting to quote famed business management author Tom Peters, from his book “Thriving on Chaos” (published the same day as October 19, 1987 stock market crash), “If you are not confused, you’re not paying attention.” I remember those two days in 1987 – it was two really bad 30% down days for the stock market. Market declines always leave investors with much uncertainty. Anxiety often moves one to draw conclusions – like recent events will end badly – which is incorrectly based for the future. The sky is not falling as Chicken Little would try to have one believe.

Let’s quickly look at key facts to answer current questions – What is the state of the US economy? What are the chances of a recession? And what represents value at current prices? First, the US economy is likely to slow some in 2019 from its fast pace in 2018. But it is still the envy of the world – unemployment rate at 3.9% (near a 50-year low) with wages rising at about 3% while core inflation is +2.2% (with oil prices falling again); worth noting that a slowing economy is very different than contracting; and a recession is very unlikely with these economic facts. Recessions normally start when the Fed tightens too much, or there is some other policy error – fiscal, regulatory, or trade; or there is some other external big event. Important to know, that while the Fed is tightening, the real (after inflation) Fed Funds rate is only +0.25% higher than the current inflation rate. Prior to the last 8 recessions (back to 1960), the real Fed Funds rate was at least +2.0% higher than inflation. Even though the markets are telling the Fed to stop, slow down, wait and watch, the Fed is a long way from the type of higher rates that are in critical full-blown error territory. We know the Fed is monitoring financial conditions closely, and we expect Fed policy to be better for the markets in 2019. Fiscal policy is still pursuing stimulation, as is regulatory policy. Trade is obviously an issue impacting a global economy which is soft. China is slowing a lot; and Europe is working through many big political and economic issues at a time when the ECB plans to start tightening monetary policy. We suspect the Administration follows the stock market’s performance closely (barometer of success). Aware of recent tough market action, the Administration should be strongly incentivized to pursue a tariff resolution with China. Finally, stocks are cheaper than bonds, and selling at levels that support attractive 12-month returns. Someone said, “If you liked it at $50, you love it at $25.” These facts should be remembered…

When confusion abounds to cloud perspective, it is appropriate to step back to review correct and historical facts. This action helps remove emotional-based thinking/decisions that can dramatically alter plans for success. We believe 2019 will be a successful investing year. The Fed understands the risks; the Administration understands the tariff impact on the US and global economy. Recent market damage will take time to repair and recover. In the near term, we could likely see more investor fear because of up/down market volatility. Thus the current drawdown process may not be complete. Fear & volatility together, will require additional time to pass for the market to complete its basing process. If the Fed evolves and tariffs resolve, 2019 should reprice on positive fundamentals toward higher levels achieved in September 2018.

SHILLY-SHALLY PRONE

The financial markets are prone to “shilly-shallying” these days. If you blink, you’ll miss it. If you take a stroll, you could miss it. If you take a nap, you may be glad you did miss it. The recent volatility of the stock market could be classified as “shilly-shally” prone – moving up/down so quickly that it is difficult to understand what is happening. The first recorded use of the term was from Sir Richard Steele’s 1703 comedy, “The Tender Husband, or the Accomplish’d Fools.” It includes “I’m for marrying her at once – Why should I stand shilly-shally, like a Country Bumpkin?” Meaning “shall I, shall I not?” Today, the verb means “failing to act resolutely or decisively; or “the government shilly-shallied about the matter.”

Despite stock, bond and portfolio performance for 2018, we are not “shily-shally” about investing. We are resolute in managing client portfolios for long term results. We understand that long term investing involves up/down movements, with some years being one that is not desired. That was how 2018 ended. The economy performed better than the stock market. Of course, the economy is not the market and the market is not the economy. The market is a discounting mechanism, or sometimes called a “voting machine” that weighs the collective investor buy/sell activity each day based upon often too short-sighted “news.” At this time, the fear is that some policy mistake – monetary or trade – is possible (some would argue, even likely).

Entering 2019 the stock market is more attractive at this point, being cheaper by about 15% on a valuation basis (past valuation discounts ranged from 15% to 18%), when a recession and bear market did not occur. We expect the year ahead will provide a positive full-year return experience, and the economy is not likely to slide into recession.

Allow me to share facts about 2 prior time intervals, wherein the market declined -15% or more and a recession did not result. The first looks back to the significant market drop in 1962 where no recession occurred. The market peaked in late 1961 after a virtually uninterrupted run of almost 10 years. In the spring of ’62, President Kennedy battled a standoff with the CEO of US Steel, which heightened market selling. Ultimately, the Kennedy Slide of -28% was short lived (138 trading days), with the market indexes hitting new highs just 14 months after bottoming. The economy did not enter a recession. More recent and perhaps relevant, the current environment appears very similar to the winter of early 2016. In 2015, the US dollar rallied (as it did in 2018); stocks were under pressure in early 2016 declining -15%; oil prices tumbled going into year-end (pushing inflation expectations sharply lower); and the Fed ended 2015 hiking rates despite rapidly tightening financial conditions (like 2018). Then, remember that stocks rallied from February 2016 for the next 2 years without so much as even a 5% pullback as those concerns were resolved or faded. It is very possible that resolution of present-day concerns will occur in early 2019 and lead to attractive and swift relief from recent market volatility.

Following many bad market historical situations, strong accumulation of stocks quickly emerge coming off the lows. Strong accumulation will be a benchmark for judging the strategic duration of any rally that develops in 2019. We know investment success accrues to long-term investors who endure “shilly-shally” volatility. History is repeat with numerous examples that reward investor endurance.

WE WORK WITH ROCK STARS

Client portfolios own a diversified mix of no-load mutual funds and ETFs (exchanged traded funds). Our ongoing efforts seek to utilize funds that employ repeatable proven investment processes, with no two funds investing the same way. Funds included in client portfolios are “rock stars”, as their strong repeatable investment processes are proven – their historical performance experience is attractive relative to peers. We seek to use funds with reasonable operating expense ratios (as expenses do weigh on investment returns), attractive tax efficiency (for personal accounts), and that are experiencing net money inflows. It is also appealing when the managers of the fund invest a significant amount of their own monies in the fund they manage; they “eat their own cooking”.

At year-end, the stock market drawdown afforded us the opportunity to swap from a couple of funds (that distributed large capital gains) into other funds and ETFs that meet various important criteria. We also worked to reduce the capital gains tax impact of these distributions by capturing some losses that developed from the distributions themselves and negative market action. These distributions also increased the level of cash. As we begin 2019, our reinvestment efforts are focused on continuing to own lower risk funds and ETFs as the current bull market is 118 months old (since March 2009). We are attracted to new funds that should assist portfolio management with good tax control. Our modifications also attempt to rebalance the portfolio strategy with small changes, to focus on funds that reside in less risky and/or undervalued market areas, like value-style stock funds. We still own growth-style stock funds; but our tactical strategy is rebalancing toward undervalued market areas.

Clients observed changes in their portfolios near year-end. They will also see some continuation of those adjustments during early 2019 as we complete reinvesting cash distributions and new deposits. Please know that our activity is oriented toward managing (minimizing) risk for the expected return opportunity. At this time, we are trying to utilize funds oriented toward providing portfolio safety. Portfolios are managed for the long term, with a close eye on current events and market valuation. If we (clients and us) established portfolio investment objectives correctly, and we utilized “rock star” funds in the portfolios, then clients should be in position to remain a long term investor.

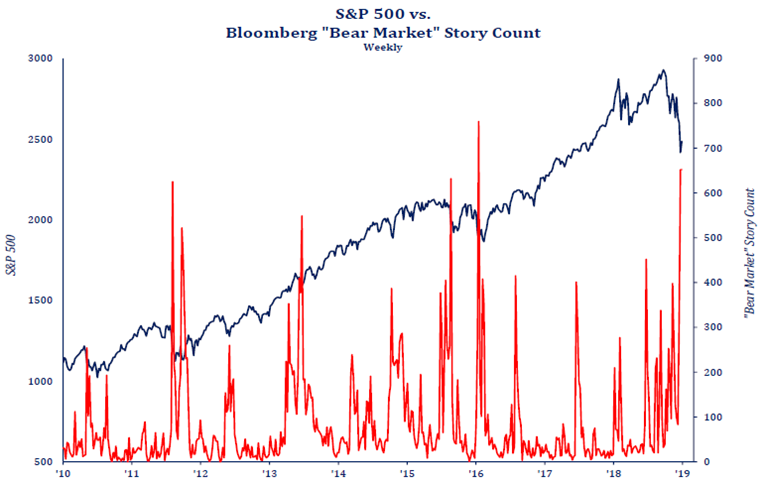

Interesting Chart (source Strategas Research Partners):

“Bear Market” word search. A word search for how many times “Bear Market” appears in investment stories provides a different look at investor sentiment. As the chart (right) shows, the word count jumps as the market undergoes big downward movements. Look at the red line “Bear Market” word count in 2015-2016, or 2011 compared to the stock market blue line. It jumps at market lows. It’s close again in 2019.