No Brakes & More Gas! | Steve Henderly, CFA

Printer Friendly PDF: Link to PDF Version

The third quarter provided big encouragement for long-term investors, defying persistent anxiety about the economy, politics, and more. Stocks and client portfolios alike enjoyed three consecutive months of decidedly positive performance. Let’s review:

“Christmas in July” – In July, markets received the gifts investors appeared to long for: passage by Congress of the so-called “OBBB” tax and spending bill making permanent tax cuts passed in 2017 and unlocking immediate expensing for business investment. Clarity on taxes relieved one of the biggest overhangs from earlier in 2025. Simultaneously, trade negotiations advanced. Framework deals were struck with the EU, Japan, UK, South Korea, and others which collectively cover over 70% of U.S. trade. Tariffs many feared would be punitive proved to be more moderate, easing pressures on global growth expectations. Those “gifts” were the easiest source to attribute 11 new record highs and +2.2% advance enjoyed by the S&P500 during July.

“All Gas, No Brakes” was our market narrative for August as investors appeared to lean fully into momentum and interest rate cut anticipation. A surprisingly weak jobs report in early August, showing just ~75,000 jobs added in the month prior PLUS large downward revisions to prior employment figures reinforced market views that the Fed was falling behind and putting the economy at unnecessary risk. As is often the case for investing, weak economic data was viewed through rose colored glasses on the belief that a more accommodative posture could be resumed by the Fed. Chair Powell’s Jackson Hole comments fortified those perspectives and the probability of a September cut soared. Despite underlying caution with respect to what is historically a challenging seasonal stretch, the S&P gained +1.9%, set new highs, and participation broadened (70% of constituents above their 200-day averages). On the fundamentals side, S&P 500 revenue expanded ~6.3% – the strongest in over a year – dampening fears that tariffs would derail earnings.

September gave us “More Gas!” In a month historically seen as the most challenging of the year from a seasonal perspective, it was the Fed that maintained investor attention and officially delivered its first rate cut since pausing at the end of 2024. The rate cut as well as comments from Fed governors seem to officially return policy to a more accommodative trajectory, citing economic data that growth conditions are sufficiently soft to justify lowering rates. This helped the traditional size-weighted S&P500 log 8 additional record highs during the month, although beneath the surface of the go-go technology sector, the ascent was decidedly more tempered with the average stock in the 500 company index climbing just 1%.

The market enters the 4Q expecting two more 0.25% interest rate cuts before year-end and two to three more in 2026. As alluded to above, market performance during the 3Q remained strongest among the Magnificent 7 and tech-sector stocks. This leadership is disconcerting for those – like us – who see that area of the market as priced for perfection and too heavily concentrated. We are encouraged to observe small-cap stocks finally record a fresh all-time high in late-September, the first new high for small cap stocks in over four years. This breakout underscores how lower interest rates are generally believed to more greatly benefit smaller companies and everyday consumers.

Read on as we dig deeper into the factors that we believe will most influence the market over the remainder of the year.

Sleep With One Eye Open

In 1991, Metallica released the song, “Enter Sandman”. Ever read the lyrics? They’re a bit disturbing (It’s October after all)… the imagery of a child getting tucked into a warm bed and ready for a night full of dreams but… “sleep with one eye open, gripping your pillow tight”. What will come next??

Many investors are comforted by strong market returns to date as attitudes so closely follow prices, but others may be feeling unsettled and haunted by markets trading near all-time highs entering the final quarter of 2025. It is natural to wonder if good times will continue. Policy uncertainty, soft employment data, and high market valuations square off against strong corporate earnings and resilient economic growth forecasts. Attempting to assess how much upside remains following the rally enjoyed over the last 6 months and current bull market which began in October 2022 is challenging. While the bull market is not old by historical norms (now beginning year 4), prudent investors are seldom comfortable for long. In fact, widespread euphoria or “comfort” often incites feelings of discomfort for savvy investors.

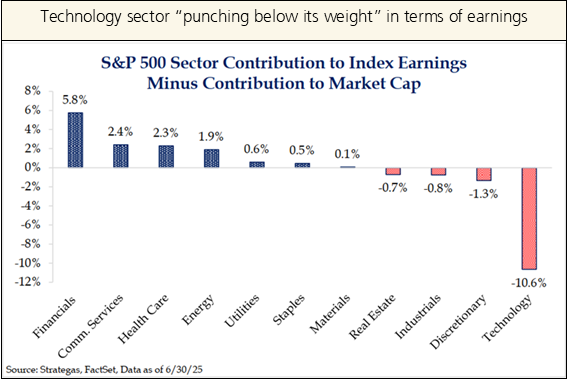

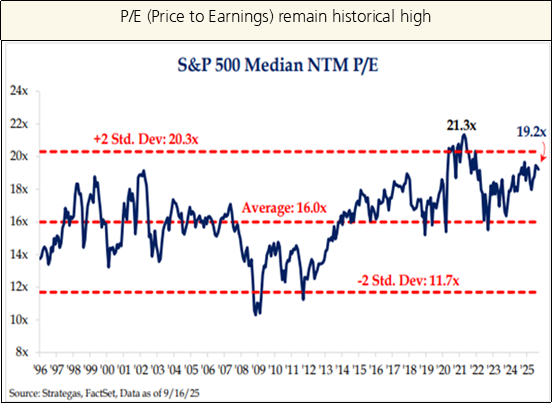

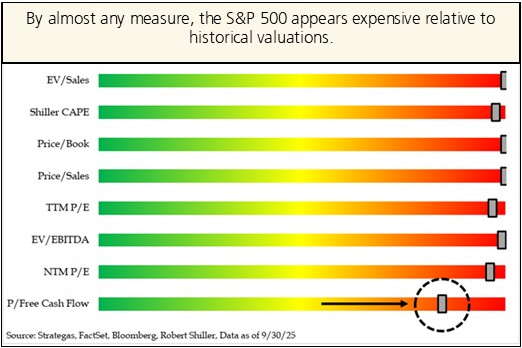

By almost any measure, the US stock market appears expensive relative to history. The five largest U.S. companies (NVDA, MSFT, AAPL, GOOGL, AMZN) trade at roughly 34x earnings versus 19x for the median stock. In general, the technology sector appears rich compared to others as it’s market value accounts for nearly 35% of the S&P500 yet delivers just 25% of the total earnings (see chart on p4). Investor sentiment surveys show bulls outnumber bears 3:1, a reading that historically appears a bit euphoric. Comparisons to the late-1990s dot-com tech bubble are resurfacing as AI spending surges and investors debate whether today’s massive capital outlays will yield corresponding transformative profits. Valuations are a poor timing tool with little historical correlation to performance in the short-run, but dynamics like these provide less cushion to absorb unexpected disappointments and imply abrupt pullbacks are possible.

One near-term source of noise is the U.S. government shutdown that began October 1 over a budget impasse with healthcare spending at the center. Shutdowns historically average about eight days, though this one could last longer (the 2019 shutdown ran 34 days). In past episodes, shutdowns generated more bark than bite, with little lasting impact on GDP or financial markets once funding resumes. Still, in 2025 the backdrop of rising debt and fiscal deficits seems to matter more than recent years. Bond market “vigilantes” are stirring intermittently this year, and persistent deficits could push the topic of fiscal discipline back into the spotlight and send U.S. yields higher, making the budget standoff more relevant than usual.

Whenever the stalemate is resolved, the more important question for the market outlook is how many rate cuts might the Fed ultimately deliver? What interest rate is “neutral” (neither simulative nor restrictive) for the economy? The Fed labeled its recent September cut a “risk-management” cut. The risks include concerns about the labor market and what it portends for the US consumer. Some of the weakness may be related to the administration’s policies on immigration.

This rate-cutting cycle is unusual, as past Fed cuts often occurred only after banks and credit markets showed stress. Futures now imply two more interest rate cuts in 2025 and two or three more in 2026, though expectations are getting trimmed since September’s move. While lower rates are broadly seen as positive, the impact is mixed: savers benefited from higher yields the past four years, and each quarter-point cut erases an estimated $35 billion in annual interest income. The tradeoff is cheaper credit for borrowers but less income for more affluent consumers, along with the risk that easier policy rekindles inflation.

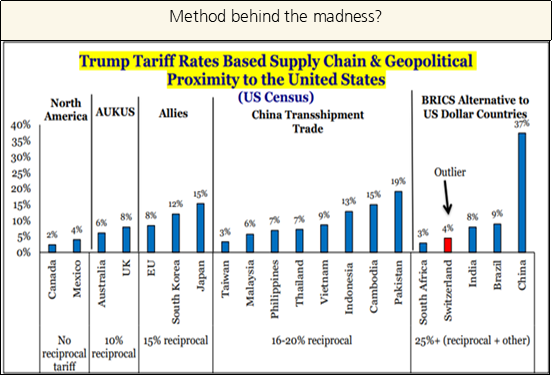

Tariffs also remain a key wild card despite investor fatigue. The Supreme Court will soon rule on the legality of levies already collected. If deemed invalid, revenues may need to be rebated. That outcome could worsen deficit concerns and push bond yields higher, offsetting refinancing benefits for businesses and consumers. The administration also possesses backup plans to reimpose tariffs, keeping trade uncertainty alive. From an inflation standpoint, it’s unclear to what degree tariffs filtered through to prices and supply chains so far. The holiday season may offer the first real test of their impact on businesses and consumers.

concerns and push bond yields higher, offsetting refinancing benefits for businesses and consumers. The administration also possesses backup plans to reimpose tariffs, keeping trade uncertainty alive. From an inflation standpoint, it’s unclear to what degree tariffs filtered through to prices and supply chains so far. The holiday season may offer the first real test of their impact on businesses and consumers.

As we know, the market climbs a “wall of worry”. Despite these highlighted concerns, our base case remains constructive over the remainder of 2025 and into 2026 based on fundamentals.

Even with recent job revisions showing nearly one million fewer payrolls through March, corporate profitability is at its highest in over 15 years and still expanding. This suggests strong productivity gains, likely aided by AI. With sales growth (~5% nominal) outpacing wages (~3.6%), profit margins remain supported. Lower interest rates should ease burdens for indebted firms and consumers, even if cash-rich companies lose some interest income. We expect earnings to keep growing, particularly among small- and mid-cap companies, and history shows the U.S. economy rarely runs into major trouble while profits are still rising.

The S&P 500 now sits nearly six months off its April 8 low and the gains of nearly +35% are robust (4th strongest advance following a –15% or greater drawdown), but history shows recoveries rarely end here. On average, the next six months following similar rallies added about +10%. Seasonality is supportive with Q4 and Q1 usually strong. Small caps, fresh off a four-year drought, recently broke to new highs. Breakouts like the one just witnessed historically preceded advances of +30–50%. Market breadth will be key to watch; we (and other diversified investors) would enjoy seeing the “typical” company outpace the well-worn Mag-7.

The S&P 500 now sits nearly six months off its April 8 low and the gains of nearly +35% are robust (4th strongest advance following a –15% or greater drawdown), but history shows recoveries rarely end here. On average, the next six months following similar rallies added about +10%. Seasonality is supportive with Q4 and Q1 usually strong. Small caps, fresh off a four-year drought, recently broke to new highs. Breakouts like the one just witnessed historically preceded advances of +30–50%. Market breadth will be key to watch; we (and other diversified investors) would enjoy seeing the “typical” company outpace the well-worn Mag-7.

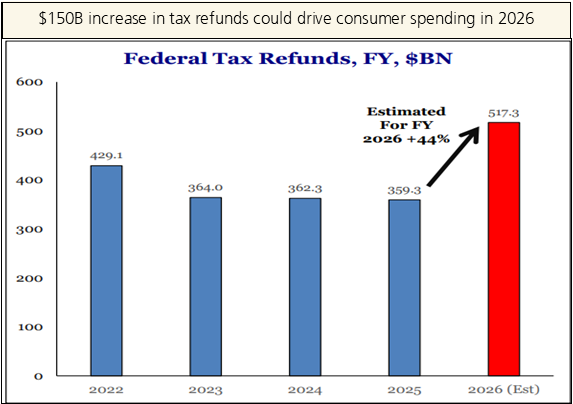

If all of this sounds too consensus, how about a less mainstream idea we came across from market strategist Strategas Research Partners. Consumers could be the next driver of gains. Despite headlines of rising unemployment and cautious consumer sentiment, tax cuts are expected to result in sizable 2025 refunds boosting disposable income moving forward. The 2026 World Cup and America’s 250th birthday are seen as potential spending tailwinds. With wages moderate and nominal activity expanding faster than costs, corporate profits should remain resilient. Productivity from AI, especially as adoption spreads beyond mega-cap tech, could further enhance margins.

The takeaway: while risks remain, fundamentals still provide a positive path forward. Markets rise more often than they fall, rallies typically outlast pullbacks, and 2025 is proving again that equities climb a wall of worry over time. Key for all investors is being “time in the market”. Time is your greatest ally.

Rates: Two Sides of the Same Coin

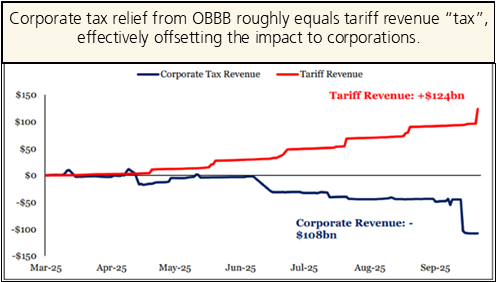

The Fed delivered on a widely anticipated rate cut of 25-basis point (0.25%) on September 17th. The timing of the Fed’s rate cut alongside the government’s massive Tax & Spend Bill amplifies the near-term impact. Lower borrowing costs paired with tax relief could spur consumer spending and business investment, lifting growth just as it appeared to be slowing. Longer term risk to inflation aside, what are some key take aways for clients? What are the pros and cons of rate cuts?

borrowing costs paired with tax relief could spur consumer spending and business investment, lifting growth just as it appeared to be slowing. Longer term risk to inflation aside, what are some key take aways for clients? What are the pros and cons of rate cuts?

For savers, rate cuts can be frustrating. We are already seeing reduced rates for money market funds, which are directly linked to short-term debt. For example, a widely held money market fund at Schwab (SWVXX) fell to 3.98% after hovering near 5% for much of 2024. Clients seeking stable returns on cash should lock-in rates via CD’s; however, we encourage a disciplined approach to cash management using our “buckets of time” concept, which aligns assets with cash flow needs. This approach is time-tested and proven to improve long-term returns on investable assets.

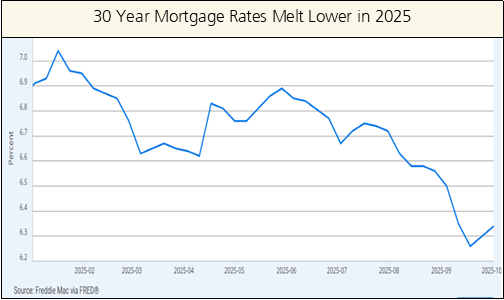

On the flip side of the coin, borrowers are seeing lower rates on credit cards, auto loans, small business loans, etc. Although mortgages are more closely linked to the 10 year treasury yield vs. short term debt, rates continue to trend lower in 2025. This is welcome news for those seeking to purchase and/or re-finance debt.

The impacts of the Tax & Spend bill are complex! Our very own Albert Van Fossen put together two great reference guides as it relates to recent tax changes (link to articles below).

- A concise list of key provisions effective in 2025 and beyond, tailored for business owners: LINK

- Understanding the New Tax Provisions for Parents. These changes offer new opportunities for financial planning. Please reach out to discuss how these provisions can benefit your family’s tax strategy moving forward or any questions. LINK

Did you Know…?

DYK? Albert is currently completing the education requirements to become an EA (Enrolled Agent) with the IRS, allowing him to support our wonderful clients with tax returns and in-depth tax analysis. Please do not hesitate to reach-out with questions!