Christmas in July | Steve Henderly, CFA

Printer Friendly PDF: August 2025 Commentary

Most think of Christmas as a December holiday, but the idea of “Christmas in July” dates back to the 1930s. Summer camps and resorts in the U.S. began celebrating the holiday in July to capture some of the magic of the season during the warmer months, and the idea spread as a lighthearted excuse for festivities and gift-giving well outside the traditional Christmas season. Today, many retailers run black Friday-like sales events, which some consumers look forward to with much anticipation. Over the last month, investors received their own version of “Christmas in July,” as several long-standing policy uncertainties finally delivered “gifts” in the form of new all-time highs for many US market indexes. Since the start of the year, tariffs, trade policy, taxes, and government spending weighed heavy on the markets. July delivered unexpected joy and excitement.

Most think of Christmas as a December holiday, but the idea of “Christmas in July” dates back to the 1930s. Summer camps and resorts in the U.S. began celebrating the holiday in July to capture some of the magic of the season during the warmer months, and the idea spread as a lighthearted excuse for festivities and gift-giving well outside the traditional Christmas season. Today, many retailers run black Friday-like sales events, which some consumers look forward to with much anticipation. Over the last month, investors received their own version of “Christmas in July,” as several long-standing policy uncertainties finally delivered “gifts” in the form of new all-time highs for many US market indexes. Since the start of the year, tariffs, trade policy, taxes, and government spending weighed heavy on the markets. July delivered unexpected joy and excitement.

Policy: Just ahead of Congress’ self-imposed deadline of July 4th, major tax and spending legislation officially titled as the “One Big Beautiful Bill (OBBB)” was signed into law. For the record, we don’t love the name, but Congress didn’t ask us for feedback! Among other things, the OBBB made permanent individual tax rates established during Trump’s first term, while providing relief to those age 65+ with an additional deduction of $6,000 per individual. The OBBB also seeks to incentivize business investment via immediate expensing of new plants, property, equipment, and more. According to Zion Research group analysis, the legislation is estimated to create one-year savings equivalent to 8.5% of S&P500 companies’ free cash flow; a boon to corporate profits. In that regard, the fiscal outlook becomes clearer and a meaningful cloud hanging over businesses and markets since spring is removed.

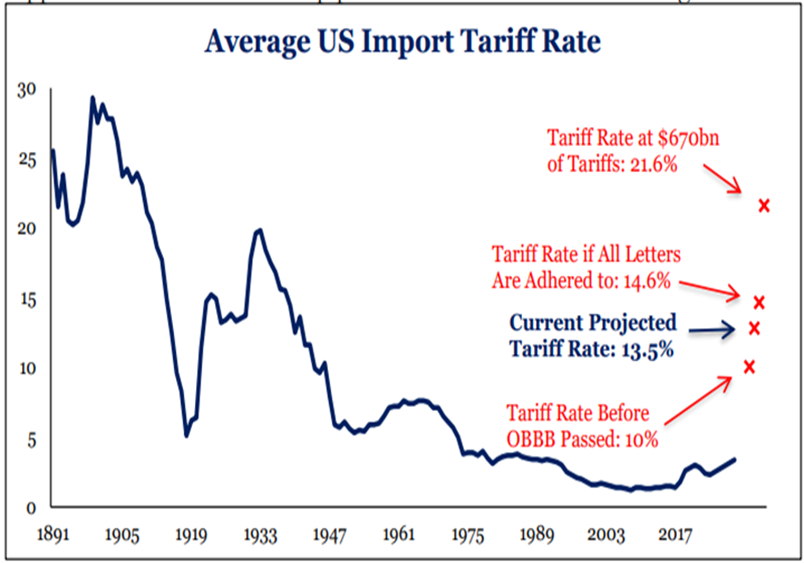

Trade: While substantive details of trade deals were largely elus ive since “Liberation Day” in April, official agreements were reached in recent weeks with Japan, the EU, the United Kingdom, South Korea, and several other nations. In fact, countries that account for more than 70% of trade with the US reached framework agreements in July and others are reportedly very close to signing deals before August 8, the most recent deadline in this ongoing saga. Research firm Strategas now estimates an average tariff rate of 13.5%; significantly less than the originally proposed average rate of 21.6%, yet still a heavy tax increase estimated at 1.6% of GDP.

ive since “Liberation Day” in April, official agreements were reached in recent weeks with Japan, the EU, the United Kingdom, South Korea, and several other nations. In fact, countries that account for more than 70% of trade with the US reached framework agreements in July and others are reportedly very close to signing deals before August 8, the most recent deadline in this ongoing saga. Research firm Strategas now estimates an average tariff rate of 13.5%; significantly less than the originally proposed average rate of 21.6%, yet still a heavy tax increase estimated at 1.6% of GDP.

Japanese equities were able to break out of a decades-long consolidation, and European markets rallied on the prospect of reduced trade friction. Tariff threats eased and markets digested the likelihood that the most punitive measures were off the table with the notable exception being China still on shaky ground. On August 1, Trump reiterated that countries not yet making deals would face escalation in the near-term but it seems peak tariff uncertainty is fading. As for our immediate neighbors (important to many domestic companies), Mexico was given a 90-day extension to continue negotiations and Canada handed a 35% tariff on non-USMCA compliant goods.

July developments on taxes and trade represent Christmas “presents” – or “candy” if recalling our spinach vs. candy analogy earlier this year where we were asked to stomach uncomfortable developments in exchange for the promise of sweet treats for dessert. The presents provided a tailwind to global equities and seemed to unlock a sense of relief in risk assets as the S&P500 set 11 new all-time highs in July and added +2.2%. US stocks broadly are now up more than +20% from their April lows. But since May gains are again strongest in the hot mega-cap technology/AI-related companies and less robust elsewhere. For example, the Dow with less concentration to names like Microsoft and Nvidia was up just 0.2% for the month. International stocks, which paused in July, are still up roughly 17% YTD – marking one of their strongest performances in the past 25 years. This means client portfolios, which are more diversified than the concentrated (cap-weighted) S&P, performed softer during the month of July. Volatility fell back to levels most often associated with calm and market confidence.

July provided gifts of clarity on taxes and trade items, but as we enter August new uncertainties confront investors. Longtime investors know that market worries are a bit like “whack a mole” – when one is beaten down, it’s usually not long before another emerges up from the ground.

Rates and Inflation: For most of the last two years, interest rates and inflation are persistent anxieties. Uncertainty was again cited by the Federal Reserve in its late-July decision to keep rates steady despite inflation not perking up in the ways many feared following the implementation of new tariffs. Fed Chair Powell struck a more hawkish tone than anticipated despite two Federal Reserve officials dissenting in favor of rate cuts. That preserved the Fed’s options until at least September when it next meets. That wait will likely keep the market hyper-focused on inflation and employment data.

In that vein, the US job market report released Friday (8/1) showed only 73k jobs added in July (weaker than expected) and prior months were revised down by a massive -258,000. This datapoint led many to question Powell’s hawkish remarks a day earlier. Was it a mistake to not cut rates last week? Will the Fed be late, holding rates in restrictive territory and causing economic harm? The economy may not be as resilient as believed. All eyes will be on Powell in Jackson Hole at the annual Economic Policy Symposium later this month.

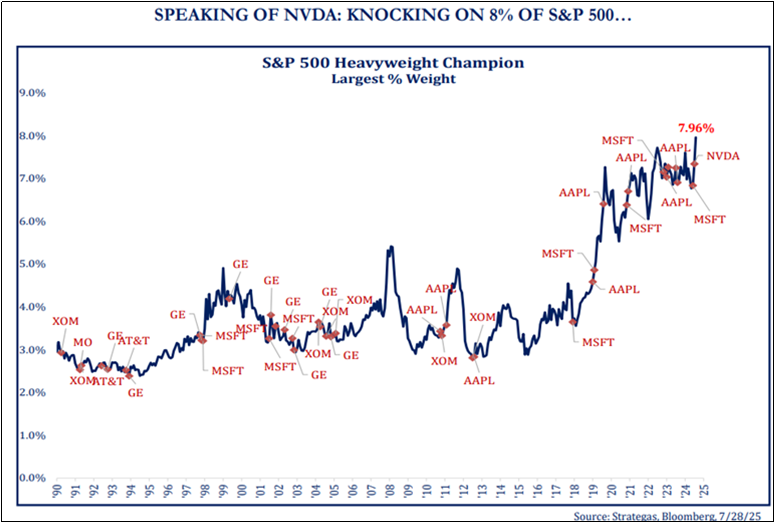

Valuations: Stocks recently achieving numerous all-time highs means Price-to-earnings multiples are again elevated. Markets are pricing a very constructive outlook. Earnings growth must materialize, especially from AI-driven productivity gains, to justify current multiples. High expectations make it harder for participants to be positively surprised; recall, the best market returns usually come when uncertainty is highest. Index concentration continues to bring risk to passive investors. Nvida’s market capitalization now exceeds $4 trillion and accounts for ~8% of the weight in the S&P500 (highest in history, reference chart).

Valuations: Stocks recently achieving numerous all-time highs means Price-to-earnings multiples are again elevated. Markets are pricing a very constructive outlook. Earnings growth must materialize, especially from AI-driven productivity gains, to justify current multiples. High expectations make it harder for participants to be positively surprised; recall, the best market returns usually come when uncertainty is highest. Index concentration continues to bring risk to passive investors. Nvida’s market capitalization now exceeds $4 trillion and accounts for ~8% of the weight in the S&P500 (highest in history, reference chart).

Disciplined investors, who endured gut-wrenching uncertainty earlier this year, are justified in being thankful for new highs achieved in July. History reminds us that August and September are often among the market’s most challenging months. That’s because trading volume is usually thin and prices often swing more than what seems rational. While recent momentum and resilient earnings trends argue against an imminent downturn, the “Santa rally in July” may now give way to seasonal chop. Corporate earnings are projected to continue growing over the balance of the year; note that an economic recession never occurred under that backdrop (monitoring earnings is important). Also important is the monetary policy action of the Fed (will they act in September, or will Powell continue to hold out?). The markets will not shy away from letting the Fed know (via volatility) if it believes rates need to be cut on soft economic data and contained inflation.

Like a holiday morning, July gave investors a burst of optimism and a welcome reduction in uncertainty. Just as toys lose their shine, markets must now contend with the realities of high valuations, interest rate debates, and seasonal weakness. Prudent investors can enjoy the gifts, but keep calm if volatility resurfaces abruptly over the coming month(s).