Trading Places | Steve Henderly, CFA

Printer Friendly PDF: December 2025 Commentary

Happy Thanksgiving! Ready or not, another holiday season is upon us. ‘Tis the season for gathering with family and friends, eating too much food, and if your schedule permits, the consumption of a few classic Christmas movies. Trading Places (1983), a comedy starring Eddie Murphy and Dan Aykroyd, may not be the first movie that comes to mind, but it is set during the Christmas season (and really funny, but not kid friendly!). Trading Places is a comedy built around a cruel social experiment conducted by the wealthy Duke brothers, who wagered they can swap the lives of two men to prove whether success is a product of nature or nurture. Louis Winthorpe III, a privileged, elitist commodities broker, is framed for crimes to destroy his life, while Billy Ray Valentine, a street hustler struggling to get by, is elevated into Winthorpe’s job, home, and social circle. As the two men adapt to their reversed circumstances, they eventually uncover the scheme, team up, and turn the tables on the Dukes by manipulating the commodity market; outsmarting the system that manipulated them and destroying the Duke brothers’ empire.

Happy Thanksgiving! Ready or not, another holiday season is upon us. ‘Tis the season for gathering with family and friends, eating too much food, and if your schedule permits, the consumption of a few classic Christmas movies. Trading Places (1983), a comedy starring Eddie Murphy and Dan Aykroyd, may not be the first movie that comes to mind, but it is set during the Christmas season (and really funny, but not kid friendly!). Trading Places is a comedy built around a cruel social experiment conducted by the wealthy Duke brothers, who wagered they can swap the lives of two men to prove whether success is a product of nature or nurture. Louis Winthorpe III, a privileged, elitist commodities broker, is framed for crimes to destroy his life, while Billy Ray Valentine, a street hustler struggling to get by, is elevated into Winthorpe’s job, home, and social circle. As the two men adapt to their reversed circumstances, they eventually uncover the scheme, team up, and turn the tables on the Dukes by manipulating the commodity market; outsmarting the system that manipulated them and destroying the Duke brothers’ empire.

Trading Places and the contrast between “have and have-nots” strikes us as a similar script for what played out in the markets during November. Since the “Liberation Day” lows of early April through October, our updates highlighted a stock market that was “all gas and no brakes” as new highs were regularly achieved despite cracks in the broader economy. But the persistent performance of several mega-sized companies with linkage to Artificial Intelligence enthusiasm drove the advance, while the average stock performed at a more cautious pace.

In November, it appears the divergence between the top of the market vs. the majority became too significant to ignore. Growing concerns about an “AI bubble” led those stocks to stall, pulling the S&P 500 down about 5% from its late-October peak through November 20th. Liquidity pressures further added to the uncertainty. Expectations for another interest rate cut in December sank from a 90% to as low as 30% by mid-month before rebounding. Bitcoin fell 27% from its all-time high, a move that signaled tightening financial conditions as it often serves as a barometer of risk appetite and leverage. Credit spreads widened modestly as economists grew increasingly concerned about stagnation if the massive spending on AI loses traction. These dynamics suggest the liquidity trade may be losing some oxygen, even as parts of the real economy are beginning to broaden. While AI remains a long-term growth engine, leadership must at some point shift toward companies adopting the technology to raise productivity – an evolution, not an end. Think less about who builds AI next year, and more about who benefits from it.

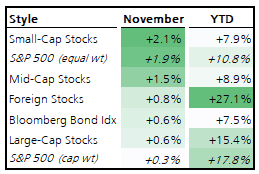

As the month progressed, odds of another Fed rate cut in December reversed higher, providing stocks with a late-month recovery that managed to bring the S&P500 back to roughly flat. However, beneath the surface, we observed notable rotation. For the first time in months, the top performing stocks were weak and leadership broadened. Equal-weight S&P outperformed cap-weight (see table in left margin), value stocks outpaced growth, and small caps beat large. Sectors more closely linked to the cyclical corners of the economy like transportation perked up and industrial-linked commodities quietly firmed. Companies with minimal exposure to AI outperformed.

It may surprise you that 65% of stocks were up in November as were client portfolios which remain less concentrated in the expensive tech names. Only the top decile of stocks – those up the most year-to-date through October – ended with negative returns and caused the market indexes to appear flat. When the market widens beyond a handful of winners, the foundation becomes healthier. That’s important; durable bull markets cannot rest eternally on the backs of just a few companies. On a side note, those with meaningful bond exposure might be pleased to hear that fixed income is on pace for its best year since 2020 (!).

So what do these market dynamics imply for the broader economy as we look to the final month of 2025 and New Year ahead? November exposed the divide between Wall Street’s version of the holiday season and Main Street’s. Corporate America, as viewed through S&P500 earnings, enjoyed +15% growth in the third quarter over last year, with every sector beating expectations. Wealth effects tied to strong equity and housing markets remain powerful. Yet consumers themselves are telling a very different story with the University of Michigan’s sentiment index falling to its second-lowest reading ever. Confidence readings are bleak, affordability frustrations remain high, and political polarization is now bleeding directly into economic responses. It’s a K-shaped pattern: the upper branch is thriving and confident while the lower branch feels stuck and pessimistic. Similar to the market, an economy is healthier when all cohorts are engaged.

The government shutdown only sharpened the split between Wall Street and Main Street, and we should anticipate that the record 44-day shutdown created an economic “soft patch” that will appear when data is ultimately released. More important to the short-term, the shutdown also created a “data fog” as the Federal Reserve prepares for its final meeting of the year next week (December 9-10). Will they cut rates by one more 0.25% this year? While policy technically remains restrictive (interest rates > inflation), the Fed is weighing whether conditions justify another risk management cut in pursuit of limiting weakness in the labor market. A stable labor market is important for consumer confidence and the resilience of the broader economy, but so are stable prices.

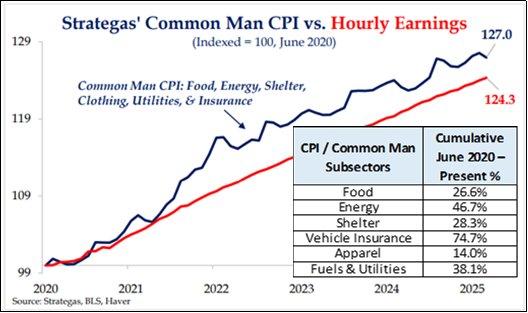

While the Fed is in focus to start December, we believe the more important factor for 2026 is corporate profits and economic growth. As noted above, earnings are still growing and the analyst community expects another +14% rise in profits for the S&P500 next year. Elevated market sentiment was a concern entering and throughout much of 2025, so it’s interesting that the narrative around consumer sentiment is so negative. The term “affordability” is the buzzword, which is essentially the cumulative impact of elevated inflation in recent years relative to wage growth which did not keep pace. As observed in the chart and data sampling to the right, “affordability” – or lack thereof – is quite real for Main Street and likely explains much of the sour attitude. It is worth noting that when consumer pessimism evidenced itself so decisively in surveys, it was a contrarian indicator. Forward performance of sectors most closely linked to consumer activity was attractive following low readings.

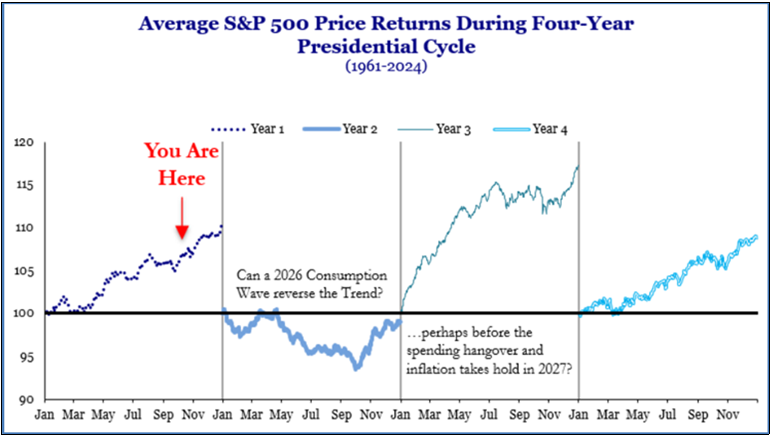

There are several positive catalysts for a resurgence of the US consumer in 2026: billions in credits and incentives for businesses, the World Cup being hosted in North America, USA’s 250th anniversary, anticipated lower interest rates, and tax-refunds from retroactive withholding changes. History shows consumers tend to spend their tax refunds, and this one could be large enough to matter. These tailwinds for the consumer are welcome relief, especially during the historically challenging 2nd year of a presidential cycle (see chart).

Taken together, November was the clearest expression yet of a market standing at a crossroads – where AI enthusiasm meets valuation reality, where liquidity tightens just as market breadth improves, and where Main Street and Wall Street experience two very different holidays. Like the split-screen opening of Trading Places, the economy is showing both resilience and strain at the same time. Further, the unease of November with pressure in AI-related stocks and cryptocurrency probably just took a little bit of air from some of the biggest concerns that were building around bubbly sentiment. Remember: sentiment follows prices – as prices cooled, sentiment came back to earth.

As we enter what is historically the strongest seasonal stretch of the year, the key question for early 2026 is whether the K-shaped recovery can converge for both consumers (have vs. have-nots) and the top of the market (mega-cap vs. average stock). If market breadth continues to improve, liquidity stabilizes, and the consumer finds support from policy and income tailwinds, the lower branch of the K-shaped recovery may finally begin to rise. Small size companies (think the “little guy”) are hovering near their largest relative discount to large cap since 2001 and seem like a coiled spring ready to bounce. For now, the divergence between have and have-nots (both consumers and markets) remains real – but so do the forces that could help Main Street “trade places” over the year ahead. We are reminded that the economy tends to avoid big trouble when profits are still expanding, and for that reason are optimistic for continued endurance of the bull market in the year ahead.

May you and your family enjoy Happy Holidays and a Merry Christmas. We thank you for the ongoing opportunity to work on your behalf and look forward to 2026.