Drinking from a Firehose: 2025 in Review | Steve Henderly, CFA

The first half of 2025 felt like drinking from a firehose. President Trump’s return to the White House brought a rapid sequence of policy headlines – including DOGE initiatives, tariffs, renewed focus on immigration, and sweeping tax and spending proposals. It felt chaotic and markets struggled to keep pace with the speed of change. Those following the news were drinking from the proverbial firehose. By comparison, the final few months of the year were less frantic but arguably more conflicted for investors with bulls and bears locked in a tug of war rather than one side clearly in control.

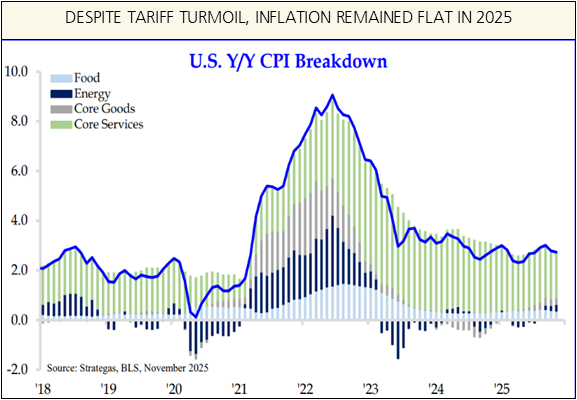

In December we wrote of a “K-shaped” recovery in a holiday-themed commentary we titled “Trading Places”; a dynamic where wealthier and higher income households generally continue to do well due to rising investment and property values, but everyday consumers feel strain. The K-shaped recovery remains a useful lens for understanding both the economy and the markets. Trump’s tariff campaign did not reignite inflation in 2025 as some feared. On the flip side, inflation did not meaningfully ease toward pre-pandemic norms. With wage growth not fully offsetting higher prices, affordability became the buzzword for lingering pressure on consumers – helping explain why consumer confidence remained weak even as markets pushed higher.

and higher income households generally continue to do well due to rising investment and property values, but everyday consumers feel strain. The K-shaped recovery remains a useful lens for understanding both the economy and the markets. Trump’s tariff campaign did not reignite inflation in 2025 as some feared. On the flip side, inflation did not meaningfully ease toward pre-pandemic norms. With wage growth not fully offsetting higher prices, affordability became the buzzword for lingering pressure on consumers – helping explain why consumer confidence remained weak even as markets pushed higher.

On monetary policy, the Federal Reserve delivered three rate cuts in 2025, largely in line with consensus expectations. The timing of these cuts was somewhat delayed however, arriving later than many investors anticipated given the easing cycle began in September 2024. Entering 2026, the prevailing view is that the Fed is likely on hold unless economic data, including employment statistics, deteriorates meaningfully.

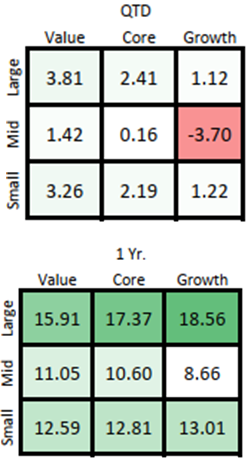

Despite all the noise, 2025 turned out to be a solid year for investors. The U.S. equity market finished the year up roughly 15 – 18% depending on your preferred index of the Dow or S&P, extending a strong two-year run following the 10 month bear market low established in October 2022. That said, gains were again top-heavy. The same small group of mega-cap technology stocks accounted for a disproportionate share of returns, particularly from May through October begging the question, is the S&P an index or just 10 stocks? Mid- and small-size US stocks advanced, but performance was a muted 10% and 7%, respectively.

depending on your preferred index of the Dow or S&P, extending a strong two-year run following the 10 month bear market low established in October 2022. That said, gains were again top-heavy. The same small group of mega-cap technology stocks accounted for a disproportionate share of returns, particularly from May through October begging the question, is the S&P an index or just 10 stocks? Mid- and small-size US stocks advanced, but performance was a muted 10% and 7%, respectively.

By contrast, international equities were a bright spot and a bit of a surprise considering persistently sour headlines. International did even better than US large-cap leaping more than 25%. Often overlooked but important risk diversifiers, bonds delivered their best year since 2018, providing welcome relief after the painful experience of 2022. Still, most diversified and active strategies struggled to keep pace with the concentration in tech of cap-weighted stock market indexes as few individuals or institutions can justify a 40% allocation to just 10 mega-size tech companies.

By contrast, international equities were a bright spot and a bit of a surprise considering persistently sour headlines. International did even better than US large-cap leaping more than 25%. Often overlooked but important risk diversifiers, bonds delivered their best year since 2018, providing welcome relief after the painful experience of 2022. Still, most diversified and active strategies struggled to keep pace with the concentration in tech of cap-weighted stock market indexes as few individuals or institutions can justify a 40% allocation to just 10 mega-size tech companies.

Aside from the difficult stretch from February through April when several mega-cap names fell more sharply than the broader market, the “Magnificent Seven” roared back in the second half and finished the year near the top of the leaderboard. The resurgence is reviving bubble-type valuation debates. Mid- and small-cap stocks did show improving participation in the final 3 months of the year, once again leaving investors asking whether next year (2026) might finally be the one when the gap begins to narrow. As with Ohio’s professional football teams, the Cleveland Browns and Cincinnati Bengals, optimism for a breakout feels perennial, but the valuation gap suggests patience should eventually be rewarded.

Outlook for 2026: A Footrace Between Inflation and Productivity

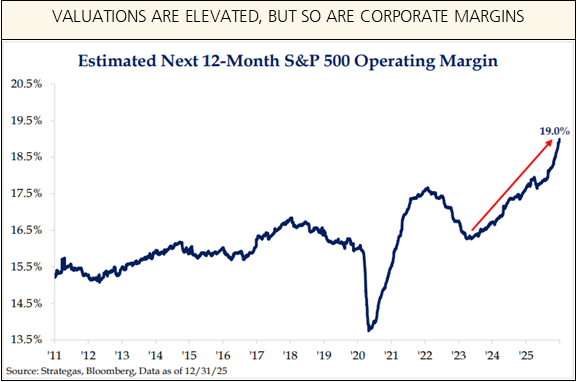

As we enter 2026, most economists and strategists are highlighting an investment backdrop that remains constructive. Central to the positive outlook is continued economic expansion and corporate profits again growing at a double-digit pace. That’s encouraging – historically the economy and markets avoid major trouble when corporations are enjoying solid profitability, even if valuations are elevated.

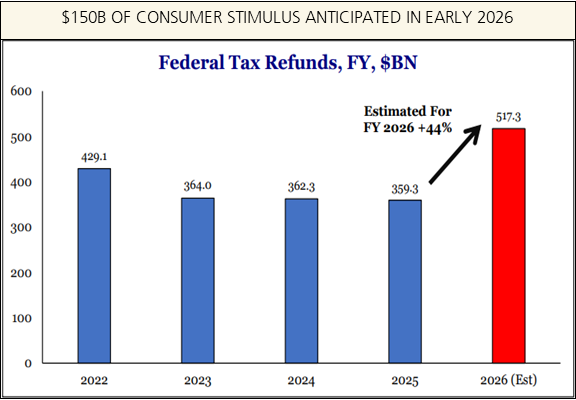

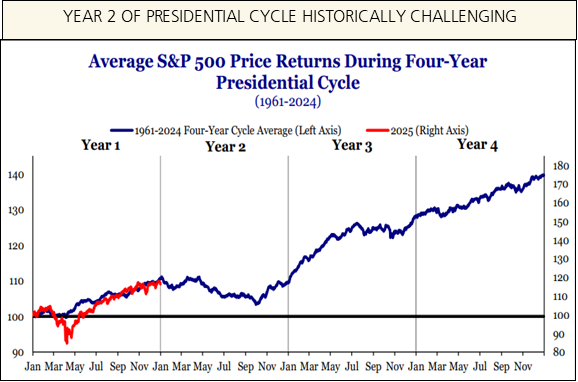

Significant stimulus for the consumer in the form of tax refunds from the 2025 tax and spending bill is anticipated in 2026, which bolsters the view of corporate profitability. But investors should not expect a year without jitters. 2026 is a midterm election year, and history reveals larger and more uncomfortable intra-year drawdowns are common – often during the 1Q. There will also be a new Chairman of the Federal Reserve. Political uncertainty, shifting policy priorities, and ongoing debates around inflation, fiscal discipline (or lack thereof), and interest rates will likely keep markets choppy. Rosy market sentiment paired with high valuations provide little room for unexpected disappointments. When volatility strikes due to sour news on employment, inflation, or corporate profits, odds are increased of a more amplified and jarring market reaction. Will fresh Venezuela news hold any implications for other areas of geopolitical stress like China/Taiwan, Russia/Ukraine, Iran, etc., around the world?

Volatility or not, areas of market leadership may change in 2026. Valuation between large-cap stocks relative to mid- and small-cap companies is historically wide; November and December provided some early signs that the market may be rotating and broadening. International equities, despite their outstanding performance in 2025, continue to trade at meaningful discounts to U.S. counterparts, raising the possibility that leadership broadens geographically in addition to size and sector. We also observed strength in transportation stocks, commodities, and select industrials during the final two months, which suggests markets may be “sniffing out” a more durable global economic upturn.

Several key themes stand out as potential drivers of performance in this environment:

Quality and Free Cash Flow: After years in which cheap capital rewarded growth at almost any cost, the market is increasingly differentiating between companies that need financing and those that can self-fund. Businesses with durable free cash flow, strong balance sheets, and the ability to reinvest internally are better positioned if interest rates cannot be trimmed further. In a world where liquidity is no longer cheap or unlimited, financial self-sufficiency matters.

Artificial Intelligence, Hype to Productivity: Hyperscalers and semiconductor producers continued to capture the early gains of the AI cycle (now in year 4). But AI should (must) at some point provide significant efficiency gains to the business consumers. “Agentic” AI – tools that automate workflows, improve decision-making, and reduce labor intensity – provide the potential to show up in productivity and margins across a wide range of industries.

The Industrial Power Renaissance: Demand for electricity is accelerating driven by data centers, AI workloads, reshoring, vehicle electrification, and infrastructure investment. There are meaningful implications for utilities, power equipment manufacturers, engineering firms, and materials suppliers. The need to build it, power it, and protect it is becoming a defining feature of the next investment cycle.

De-globalization and Geopolitical Fracture: Long-standing global operating assumptions are being challenged. Trade relationships, supply chains, defense spending, natural resource access, and technology and intellectual property sharing are all being reshaped by geopolitical tension and populist pressures. This fragmentation creates investment opportunities tied to reshoring, defense, domestic manufacturing, and strategic resource development. Also ahead is a Supreme Court ruling on Trump-era tariffs, a decision that could hold meaningful implications for their constitutionality and future tariff mechanics.

Trump will announce his pick for the next Fed chair soon. In the coming weeks, the Treasury may need to borrow more to fund larger refund checks under the One Big Beautiful Bill Act. Any or all of these developments could agitate the Bond Vigilantes, driving up borrowing costs for the US Government.

A Wave of Consumption: Despite ongoing concerns about consumer confidence, fiscal policy remains a powerful force. Billions of dollars in tax credits, particularly those tied to infrastructure, energy, and industrial policy, are flowing into the economy. This spending supports demand and employment in construction, manufacturing, transportation, and services. Additionally, 2026 brings several high-profile events – including the United States’ 250th anniversary and the World Cup coming to North America – that could boost consumer confidence and spending.

AI’s potential to spark a “Roaring 20s” style expansion, combined with a recovery in depressed consumer confidence and continued productivity gains, supports the view that growth and profit momentum should ultimately outweigh valuation and sentiment concerns, even as political uncertainty keeps the path forward uneven and noisy. A consensus for 2025 looked for earnings growth and market returns to broaden beyond the Magnificent Seven, a development that failed to materialize. Time will tell if the rotation observed in November and December is durable, but the environment appears increasingly ripe for valuation disparities to begin narrowing and is consistent with the current positioning of client portfolios for the year ahead.

2026 FAQs

Why is consumer confidence weak while markets remain strong?

Markets are forward-looking and driven primarily by earnings growth, liquidity, and expectations. Consumers, by contrast, feel inflation through rent, food, insurance, and borrowing costs. Weak confidence reflects affordability stress, not necessarily an imminent recession. Both signals can coexist, and often do. To recap a theme discussed in our outlook, tax refunds (and certainty via extension of the 2017 rates which were set to expire), our nation’s 250th birthday, and other events like the World Cup are being cited as reasons why consumers may enjoy better attitudes in 2026. Even so, market performance in periods where consumers were as bummed out as in 2025 were decidedly positive, not negative.

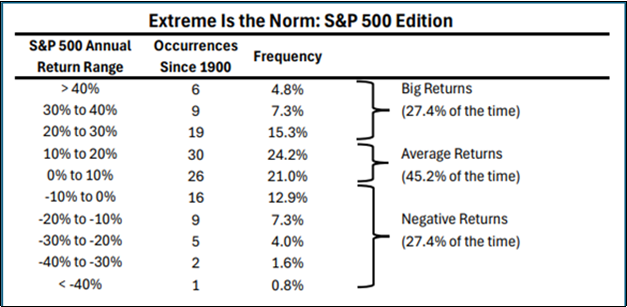

Can returns in 2026 match the last two years?

Anything is possible, and since 1926 there are four instances in which the S&P 500 enjoyed returns of +15% or more in 3 consecutive years. Generally speaking though after two consecutive strong years, forward returns tend to moderate and become choppier. In addition, midterm election year patterns suggest 2026 could be challenging. We are presently 38 months since the 2022 bear market concluded. Median forecasts for the S&P 500 call for a level of around 7500, a 9.5% rise from December 31st levels (the highest is around 8,000) – much closer to an “average” year for equities than the last two. Be aware, the long-term annual “average” is anything but typical; there are only two years in the past 30 when the S&P 500 rose between 5-10%. Returns are far more lumpy than most realize, and even average years rarely feel “average” while you’re living through them. Pullbacks and rotations are normal and often healthy.

years. Generally speaking though after two consecutive strong years, forward returns tend to moderate and become choppier. In addition, midterm election year patterns suggest 2026 could be challenging. We are presently 38 months since the 2022 bear market concluded. Median forecasts for the S&P 500 call for a level of around 7500, a 9.5% rise from December 31st levels (the highest is around 8,000) – much closer to an “average” year for equities than the last two. Be aware, the long-term annual “average” is anything but typical; there are only two years in the past 30 when the S&P 500 rose between 5-10%. Returns are far more lumpy than most realize, and even average years rarely feel “average” while you’re living through them. Pullbacks and rotations are normal and often healthy.

What should investors focus on now?

Breadth, productivity, and liquidity. A sustained broadening of market leadership would improve the durability of the bull market from our perspective. Productivity gains must continue to offset inflation pressures. And changes in Fed balance sheet policy, alongside interest rate decisions, will play a critical role in determining how supportive financial conditions remain.

Gold was the best performing asset in 2025. Thoughts?

The enthusiastic price action around precious metals throughout the last 12 months was quite amazing. Historically, precious metals were viewed as a risk-off safety trade, but when price moves are so extreme in a short period of time, adding exposure should be viewed as anything but “safe”. We view the asset class as extended in the short term and vulnerable to outsized setbacks with little notice.

Other themes to consider?

Consider the gamification of financial markets and the growing convergence of betting and investment platforms. This is certainly an area of concern as the line between fundamentals-based investing and pure speculation continues to blur.

Another theme we will be monitoring throughout 2026 is the tension between inflation, affordability, and productivity gains from AI.