Rotation | Steve Henderly, CFA

Printer Friendly PDF: Feb 2026 Commentary

Ever experience de-ja-vu? Similar to much of this past year, 2026 kicked off with the markets struggling to digest a constant barrage of headlines, causing the proverbial “drinking from a firehose” feeling. Geopolitical escalation (Venezuela, Greenland, Iran), fresh tariff threats, pressure on the Federal Reserve, talk of government intervention in housing and credit markets, renewed debates around price controls and capital allocation… even another (brief) Government shutdown. All in January… exhausting!

escalation (Venezuela, Greenland, Iran), fresh tariff threats, pressure on the Federal Reserve, talk of government intervention in housing and credit markets, renewed debates around price controls and capital allocation… even another (brief) Government shutdown. All in January… exhausting!

For investors, it is not just the speed of policy announcements, but their tone. Many of the initiatives and proposals are distinctly populist and, in several cases, counter to traditional free-market and capitalist principles. Calls to cap interest rates, restrict certain investors from purchasing assets, pressure independent institutions, or directly intervene in private markets stand in contrast to the long-held assumption that U.S. policy favors deregulation, free-market pricing, and institutional independence. While headlines dominate attention, the more important story is investor response: rotation, not retreat.

This tension matters for markets. Capital is sensitive not just to growth and profits, but to rules, predictability, and trust in institutions. When policy direction appears inconsistent – deregulation in rhetoric but interventionist in practice – global investors may reassess risk. That reassessment doesn’t necessarily show up as a violent equity selloff. More often, it can also show up in currency weakness, sector performance, and leadership rotation.

The recent pressure on the U.S. dollar is a case in point. While a weaker dollar reflects many forces – geopolitics, fiscal policy, and shifting rate expectations – it also signals a more subtle recalibration in confidence. January served as a reminder that “American Exceptionalism” does not mean immunity. Persistent geopolitical uncertainty, a more confrontational policy posture, and repeated pressure on institutional independence weighed on the dollar, prompting capital to increasingly explore alternatives.

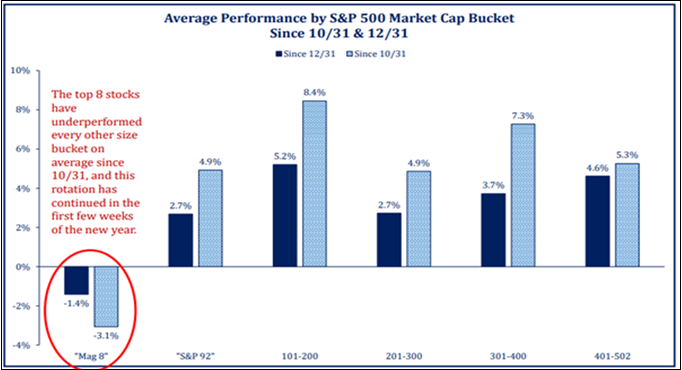

A softer dollar carries wide-ranging implications: commodity prices tend to accelerate, foreign companies benefit relative to domestic ones, and questions naturally arise around future capital flows into U.S. assets. At the same time, market leadership is rotating. The dominance of AI-linked mega-cap stocks appears to be cooling, with many of the market’s standout performers from 2024 and 2025 lagging since late October, while the other nine stock deciles (by market capitalization) moved higher. JPMorgan estimates that just 42 AI-related companies accounted for more than two-thirds of the S&P 500’s gains, earnings growth, and capital spending since ChatGPT’s launch in Nov 2022; an extraordinary level of concentration that is unlikely to persist indefinitely.

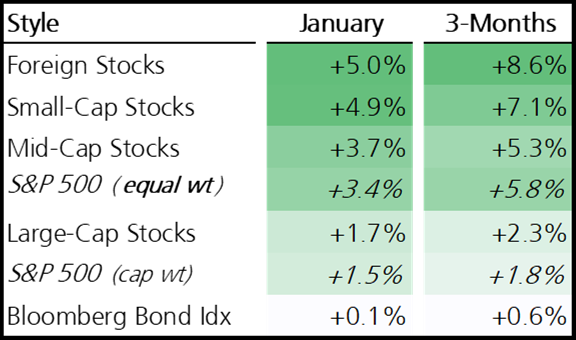

After recording four new all-time highs and briefly eclipsing a new milestone price of 7000, the S&P500 delivered a return of +1.45% in January. It’s always a little comforting when the market gets off to a good start! Historically, a positive January is viewed as a positive signal for the year ahead. While broad market indexes finished the month higher, the more revealing insight lies in the specific segments of the market driving those returns. Throughout most of 2025 (and the last several years) the strongest performance was concentrated among just a few mega-cap technology stocks. But since late-October and intensifying in January, other areas of the market outperformed. In January, equal weight large-cap (+3.4%), mid-cap (+3.7%), small-cap (+4.9%) and foreign (+5.0%) each materially outperformed. The 10 largest companies, after being responsible for more than half of the total return in the S&P500 last year, were actually negative during January. Client portfolios are benefiting from this rotation and broadening with the equity portion of client portfolios exceeding the traditional size-weighted S&P500 by more than 2% last month.

Interesting stat: small caps beat large caps for 14 consecutive trading days in January, something not seen literally in more than a decade. The Russell 2000 continues to trade at roughly a 25% valuation discount to large-caps, even as the percentage of small-cap stocks making new 200-day highs quietly rose to its highest level in a year. Transportation stocks, often viewed as a proxy for real economic activity, continued to break out, reinforcing the idea that markets may be sniffing out a broader, more cyclical expansion. And manufacturing surveys are evidencing a pickup in activity. Importantly, this rotation held up even during January’s bouts of volatility; equal-weight and smaller companies often outperformed on both declines and rebounds.

Investors should not read this as a bearish signal, but rather healthy normalization. Leadership broadening improves market durability and reduces the risk that portfolios live or die by a very small number of stocks.

One of the most encouraging signals underlying the recent rotation is improving productivity. Recent GDP growth is strong even as aggregate hours worked remain essentially flat, suggesting the economy is producing more output without commensurate increases in labor input. Corporate earnings, estimated to again expand by double-digits in 2026, support that idea. That is the pathway to non-inflationary growth, where wages, capital, and profits can all rise together rather than compete.

This matters because inflation, while cooler, remains elevated relative the Fed’s stated target. Affordability pressures continue to weigh on consumers, even as headline inflation improves. The question for 2026 is whether productivity, enhanced by AI adoption, capital investment, and reshoring, can continue to offset those pressures. If it can, the Federal Reserve can remain patient rather than restrictive. The Fed, as was expected, paused and held rates steady at its meeting during the final week of January, following multiple cuts in the 2nd half of 2025.

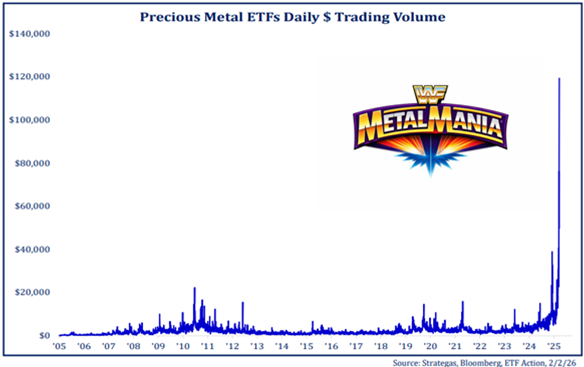

We would be remiss if not also offering a few comments on the price action observed in shiny objects during January. Precious metals surged to extraordinary levels, with gold briefly touching $5,000/oz amid geopolitical tension, dollar weakness, and renewed enthusiasm for the “debasement trade.” Many are labeling the move a flight to safety. But parabolic price surges (“Rocketship liftoff” shape) should always raise skepticism. A sharp selloff late in the month drove silver and gold ETFs down roughly 40% and 20%, respectively. Yet those declines merely reset prices to their 50-day moving averages. Even after the volatility, both remained firmly positive through January month-end. The volatility in recent days should serve as a valuable reminder that assets driven by momentum, a narrative, or fear can reverse violently. This is not to suggest there is no long-term role for real assets in portfolios, but it does argue strongly for discipline and position sizing. When something rises too far, too fast [like Tech in 2000, Oil in the ‘80s, or tulip bulbs in the 1600s], it should be viewed as anything but safe.

tension, dollar weakness, and renewed enthusiasm for the “debasement trade.” Many are labeling the move a flight to safety. But parabolic price surges (“Rocketship liftoff” shape) should always raise skepticism. A sharp selloff late in the month drove silver and gold ETFs down roughly 40% and 20%, respectively. Yet those declines merely reset prices to their 50-day moving averages. Even after the volatility, both remained firmly positive through January month-end. The volatility in recent days should serve as a valuable reminder that assets driven by momentum, a narrative, or fear can reverse violently. This is not to suggest there is no long-term role for real assets in portfolios, but it does argue strongly for discipline and position sizing. When something rises too far, too fast [like Tech in 2000, Oil in the ‘80s, or tulip bulbs in the 1600s], it should be viewed as anything but safe.

We do not believe one should interpret January’s market rotation as the end of American Exceptionalism, but a rebalancing appears in progress, which is often healthy and appropriate. Markets are rotating, leadership is broadening, and long-dominant themes are being recalibrated, not necessarily abandoned. Only additional time will tell if the rotation observed in recent months will be more durable than the brief head-fakes observed over the last several years. Regardless, volatility is likely to remain part of the landscape, particularly in a midterm election year filled with policy uncertainty. Beneath all the noise, the market continues to signal improving economic breadth. As always, staying invested, diversified, and disciplined matters far more than reacting to the latest headline or chasing the most recent parabolic price move.

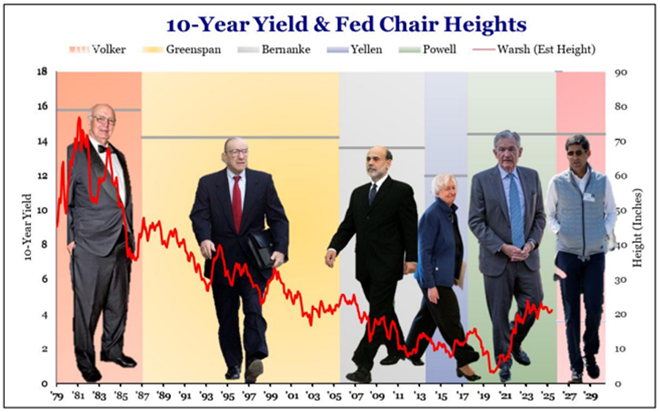

Correlation or coincidence?: Kevin Warsh was just nominated to be the next Federal Reserve Chairman. Plotting the level of interest rates against the height of Fed Chairs is an interesting picture. Does the height ofKevin Warsh (relative to Jay Powell) suggest that rates are unlikely to change much from their higher levels over the next several years? If confirmed, Warsh’s term as chair will commence in June. It is noteworthy that the market often tests new Chairmen early in their term with stressful financial conditions, but the period between nomination to confirmation is historically strong. The market is presently pricing in only two rate cuts to occur during 2026, implying most Fed meetings this year will be a hold/pause.