1Q In Review: Encouraging Rotation Gives Way to a Strait Jacket | Steve Henderly, CFA

Are you exhausted?! The first quarter included two major military operations (Venezuela and Iran), a flirtation with Greenland, another government shutdown, turbulence in private credit markets, and intensifying worries around how AI may decimate a number of sectors. The S&P 500 was down “only” 4.4% (client portfolios fared much better – more on that in a moment). Given the optimistic market sentiment entering the year, the abrupt mood swing from February to March felt even worse.

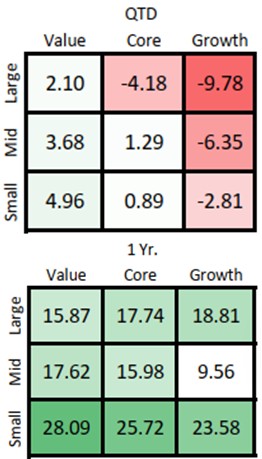

As highlighted in our January and February commentaries, diversified investors received some early vindication as the market continued to broaden beyond the handful of mega-cap technology stocks which dominated performance in 2024 and 2025. To observe the magnitude of the rotation, one needs to look no further than the equal-weighted S&P 500. It continued to reach new highs throughout much of February and gained 7%. In contrast, the traditional size-weighted version of the index – the one most often highlighted by financial media – last reached an all-time high a month earlier on January 27 and was essentially flat, up just 0.7% through February.

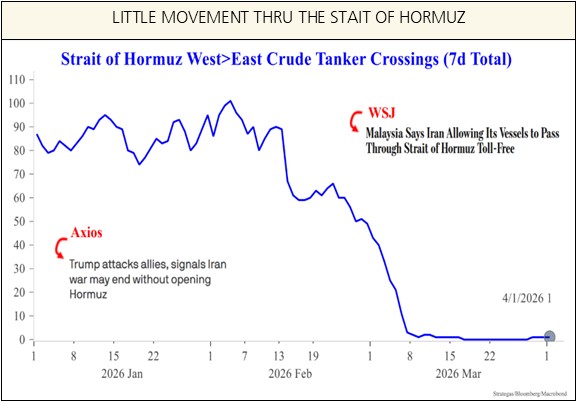

As the calendar turned to March, Operation Epic Fury changed everything and triggered uncomfortable market volatility. The strikes on Iran targeting nuclear capabilities, leadership, and Naval defenses were swift. Key question: how and when the war will “officially” conclude became far less certain as Iran’s counterattack is effectively closing the Strait of Hormuz. Oil soared more than 45% at points during the month and continues to exhibit outsized price swings in tandem with headlines/prospects for escalation or cease fire. Shipping through the Strait of Hormuz (accounting for 20% of global crude, 20% of LNG, 16% of fertilizer inputs, and 33% of semiconductor-grade helium) poses the most significant uncertainty to the economic outlook. According to some estimates, each $1 rise in crude costs the U.S. ~$8 billion annually. As of this writing, the situation remains highly fluid and subject to change at a moment’s notice, but the market appears to be trading a bit more hopeful that a ceasefire or conclusion is drawing near (time will tell if the two-week cease-fire announced on April 7 will be durable).

Client portfolios, after a strong start to the year through February, sputtered in March. Even with the set-back, they managed to conclude the quarter with modest gains, outperforming the S&P 500 by between 5 and 6%, regardless of asset mix. As noted in our special market update on March 31st, the outperformance was due to portfolio emphasis on more attractively valued areas of the stock market (lower exposure to expensively valued companies entering the year) as well as tactical thematic positions in physical commodities and electric-grid infrastructure.

Volatility is never comfortable or welcomed, and the “Fog of War” creates a different kind of uncertainty. Midterm election years historically experience larger than normal corrections (on average ~19%). The elevated uncertainty readings seen presently often precede stronger than normal forward returns. The 1-year numbers shown in client reports (from March 31, 2025 near tariff noise) are very attractive and a strong reminder. Additionally, corporate earnings grew +14% year-over-year and remain a critical fundamental anchor. When corporate profits are growing, the economy tends to avoid big trouble; but the uncertainty of war and longer-lasting supply chain disruption could begin to soften momentum.

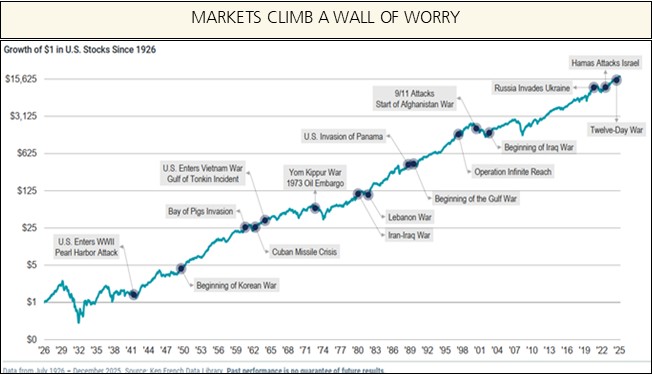

A broader takeaway from the quarter is that a constructive fundamental backdrop can, and often does coexist with periods of short-term instability. Markets historically “climb a wall of worry,” with this environment being no exception. The ability to navigate that tension, rather than react to it, is where long-term investment discipline adds the most value.

Outlook: The Fed in a Strait Jacket as Race Between Productivity and Inflation Heats Up

Investors entered 2026 with a central thesis: a tug-of-war between inflation and productivity will ultimately be won by the latter. Recent geopolitical events, which are driving energy prices significantly higher and introduce new logistic complexities to the supply chain, intensify that race considerably. Inflationary pressure – never fully eliminated since Covid – is building. Gasoline prices (like a tax) stare consumers in the face daily, and productivity gains must remain strong to absorb this supply shock. The outcome of this tug of war will shape the investment landscape for the quarters ahead.

Most are aware that oil’s impact extends well beyond gasoline. The effective closure of the Strait of Hormuz also globally impacts fertilizer costs, freight rates, helium for semiconductors, and consumer staples. The Fed now finds itself in a proverbial “strait jacket”. Inflation is rising while the labor market is showing some cracks. February payrolls fell 92,000 while March numbers exceeded expectations, adding 178,000 new jobs. The market (and Fed) will be closely monitoring this metric.

The expectation for another Fed rate cut or two by year end was quickly replaced in March with questions whether the Fed may instead need to hike rates if inflation jumps. This is not our base case given the economic uncertainties, but underscores just how quick the narrative shifted due to the uncertainty of war.

While all of this is highly uncomfortable and unsettling, we remain cautiously optimistic that the conflict with Iran can reach a durable conclusion in the coming weeks. Every week the Strait of Hormuz remains closed adds inflationary pressure and economic uncertainty. History offers some comfort: oil is typically lower 12 months following spikes due to geopolitics. The U.S. economy is also far less energy-intensive per unit of economic output (GDP) than in prior decades, which should give a bit more cushion for stimulus (like tax refund season) to persist.

The key chain to monitor: the U.S. economy depends on the stock market → which depends on the bond market → which depends on productivity winning this tug-of-war against inflation. Interest rates are important; over the last few years the 10-year Treasury rising above 4.5% marked a line in the sand (introducing a resistance or stall) for stocks. As those one-time tailwinds begin to fade, the burden shifts to sustained productivity gains and continued investment to keep this delicate balance in place.

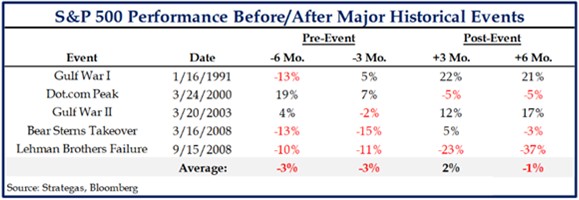

Headlines and the Trump administration signal a desire to end the conflict and frame the dialogue that mission objectives are nearly complete. Investors also note that President Trump may be more sensitive to the messages conveyed by the financial markets and stock prices than previous administrations, leading to what some are referring to as the “TACO” (Trump Always Chickens Out) trade. That said, we found the phrase “it takes two to TACO” by respected research firm Strategas particularly relevant. In War, both sides need to reach the conclusion that a cease fire is in its own best interests (the two-week cease fire announced on 4/7 is a good signal).

Back to productivity: the case is data-driven, not wishful. Real GDP exceeded 4% in the second half of 2025 even as hours worked were essentially flat, a rare and constructive combination. Another interesting stat reflects only one-fifth of U.S. companies commencing a meaningful investment in deploying AI at scale. If true, the full productivity dividend is barely started. Data center construction in the U.S. has now surpassed office construction – a sign of how much things have shifted. This isn’t being driven by consumers. Instead, it’s a business investment cycle, with companies spending heavily over multiple years to build out capacity.

We believe that the economy and capital spending ambitions of corporate America entering the year will be sufficient to weather the near-term uncertainty. Geopolitical events usually do not change broader market and economic trends; rather they end up solidifying trends that were already underway. It will be interesting to see if the trend of rotation away from the Mag 7 as leadership, toward the “rest of the market” will continue when the current worries fade. We believe in the importance of diversification, valuation discipline, and maintaining exposure to areas of the market where expectations are more reasonable. Periods of uncertainty do not invalidate long-term strategy – they reinforce the importance of it.

A notable silver lining from March’s volatility is the meaningful reset in investor sentiment – from elevated optimism (80th percentile) to much more cautious levels (26th percentile). While unsettling in the moment, history suggests that sharp declines in sentiment often lay the groundwork for stronger future returns. Periods like this tend to reward a gradual shift in focus toward what could go right, instead of dwelling on what could go wrong.

Frequently Asked Questions

Q: Are we at the start of a bear market?

That will only become apparent in hindsight. At present it does not appear the case. Bear markets require deterioration across employment, financial conditions, and corporate profits. Profits remain strong (+14% y/y earnings growth), while February’s -92,000 payroll print, widening credit spreads (12-month highs), and rising consumer stress create some warning signs. From a sentiment perspective, bears now outnumber bulls with the gauge near the 30th percentile – historically readings in this zone are more consistent with buying opportunities than sustained bear markets.

Q: Will the Iran conflict cause stagflation?

The U.S. is experiencing both a growth shock and an inflation shock simultaneously; monetary policy cannot resolve both at once. In fact, as long as the flow of traffic through the Strait of Hormuz remains restricted, the Fed will be confined in a “Strait Jacket”. That said, today’s economy bears little resemblance to the last stagflation environment of the 1970’s. Unemployment is low and the misery index (unemployment + inflation) is a fraction of what it was then. The key variable is duration. A near-term resolution in Iran preserves the base case; a prolonged conflict raises the odds of uncomfortable inflation and stagnating economic growth.

Q: What signals would suggest the AI capex cycle is ending?

Watch revenue trajectory of companies like OpenAI (they’ve committed $200B through 2030 requiring debt financing) and Nvidia’s stock price — which is not rewarding strong earnings over recent quarters. If hyperscaler spending slows materially or debt markets restrict AI financing, that’s a more serious flag. With only ~20% of companies reporting any meaningful investment in AI so far, the cycle appears to be in the early innings; we view it as healthy that the market is slowing its enthusiasm for stocks that surged by the most eye-popping sums.

Q: Should we worry about private credit?

The situation with illiquid private credit (ie: private issued bonds/debt) markets is concerning to us because the asset class is being pushed in recent years to investors in many forms – whether appropriate or not for the investor profile. Apollo and Blackstone devalued certain loans to zero during the 1Q that were carried at par just three months ago; some fund sponsors are installing redemption gates to limit or prevent investor withdrawals. We are monitoring this closely for potential spillover into broader financial conditions. Nvest portfolios do not own any direct investment exposure to private credits. An asset class with less than daily liquidity generally does not align with one of our core investment philosophies: No investment should control its owner. Private credit stress is one of the three macro overhangs alongside Iran and AI capex currently dampening market confidence.

Q: Any silver linings we might be overlooking?

(1) The 2026 FIFA World Cup, co-hosted by the U.S., Mexico, and Canada across 11 U.S. cities, should generate meaningful incremental tourism and consumption this summer. This year also marks the 250th birthday of the USA and expected to produce an economic boost.

(2) Earnings expectations remain robust at +14% for 2026 – a fundamental backstop.

(3) Historically, the strongest market recoveries follow exactly the kind of elevated uncertainty readings we’re seeing today. Patience, diversification, and discipline remain a time tested formula for long-term success.