Turn! Turn! Turn! | Steve Henderly, CFA

Printer Friendly PDF: March 2026 Commentary

Clients may recall our commentary a few years ago where we referenced this 1965 #1 hit song title by The Byrds. In March 2022, we were in the early innings of the most aggressive tightening of Fed monetary policy in modern history to combat inflation. The song is notable for being one of the few pop hits whose lyrics are drawn almost entirely from biblical scripture (Ecclesiastes 3:1-8). The song was also emblematic of the era’s mix of spiritual reflection and subtle anti-war sentiment, as well as symbolizing cycles of change, generational transition, and the hope that turbulent times would give way to renewal.

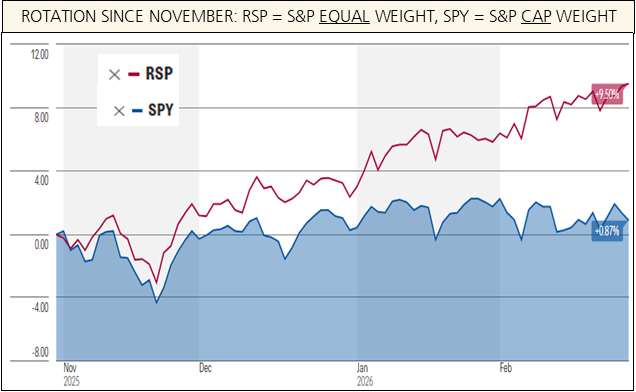

Today is not 2022 and the backdrop is very different, but if January hinted at “Rotation” (the title of our January commentary), February confirmed it. Turn! Turn! Turn! There were so many developments during the month and unfolding presently that it feels nearly impossible to address each of them in significant detail. While Venezuela’s regime was removed in January, the last several weeks remained dizzying as the US Supreme Court struck down last year’s tariff framework in a 6 – 3 ruling, an “AI-apocalypse” narrative ricocheted across markets, and now an open conflict with Iran commencing on the final day of the month. When events cluster this tightly, it can feel like instability. But markets rarely turn because of headlines; headlines tend to reinforce new trends (turns) already underway. Since October, rotation of market leadership is impossible to ignore.

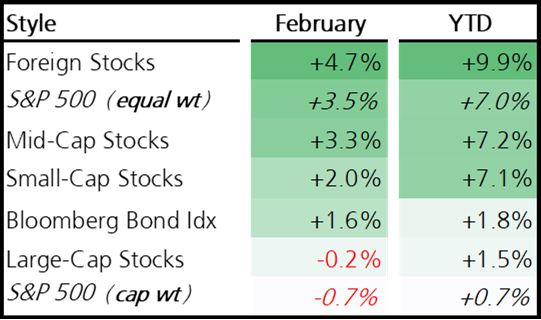

If one is only watching the traditional S&P500 (size weighted), 2026 looks indecisive with a return of just 0.7% YTD (thru 2/28). Yet the equal-weighted version of the S&P500 achieved a new all-time high in February and isup roughly 7% year-to-date. Performance in recent months expanded beyond the handful of mega-cap names that dominated most of the last two years. Rotation doesn’t get any more visible than observing the Magnificent 7 (MAGS) fall more than 7% or software stocks (IGV) down roughly 23% year-to-date. Capital is redistributing toward other sectors including industrials, materials, health care, transports. Mid, small, and international companies sport positive YTD returns ranging between 7-10%.

Perhaps most remarkable is the speed at which the rotation and narrative surrounding the market is taking place. It seems like just weeks ago that any and all AI investment was hot. Today, investors are debating whether AI will hollow out entire industries — from accounting and insurance brokerage to logistics and legal research.

Regardless of whether the sudden pessimism toward AI is overdone, lost in the noise of the last two years is that the digital economy will still depend on the physical one. Data centers require enormous amounts of electricity, materials, cooling infrastructure, and capital investment. This buildout supports industrial production and energy demand even as it enhances productivity. These areas of energy infrastructure and physical commodities are surging in portfolios in early 2026.

Productivity measures are quietly accelerating. Real GDP exceeded 4% in the back half of last year even as hours worked were flat – an unusual and constructive combination. Corporate sales growth continues to outpace cost growth. In many ways we are observing characteristics more consistent with the early stages of an expansion (including new capital investments) than with a late-cycle slowdown. The debate in 2026 may not be whether AI destroys jobs, rather if productivity gains can continue to outpace inflation pressures.

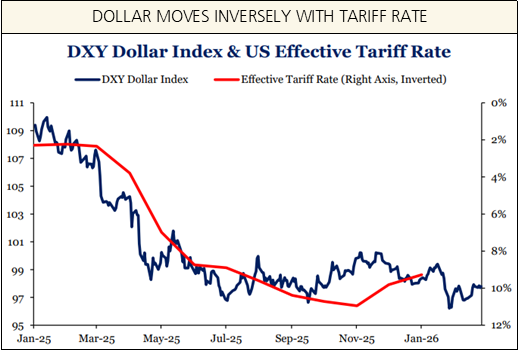

Outside of the economic and corporate investment narratives, the overall backdrop remains more complicated (as it most often does). Policy continues to shift abruptly. The Supreme Court’s ruling against the basis for which tariffs were imposed last year (“Liberation Day” in 2025) was followed immediately by a revised 15% global tariff structure. This move by the Trump administration was not a surprise, but it reintroduces trade uncertainty. Venezuela’s regime change and rising Middle East tensions added geopolitical weight and now the open and active conflict/war with Iran creates another worry item; chief among several is inflation (more below).

Against this backdrop, the U.S. dollar is again weakening. A weaker dollar is not inherently negative; it often puts upward pressure on commodity prices and is a tailwind for performance of foreign investing relative to domestic. The “de-dollarization” narrative aligns with the broader rotation away from US large companies we are observing in recent months.

Concerning Iran, energy markets are the most direct economic linkage. Oil prices matter because they directly influence inflation expectations and interest rates. In recent days oil prices are spiking; however, oil often traded lower 12 months after geopolitical spikes. Shipping costs also need to be monitored. What ultimately determines economic impact is whether supply disruptions become sustained and structural. In the early days of March, markets are adjusting but history reveals that conflicts usually do not create lasting impact on financial markets. No one knows for sure how the conflict will continue to unfold. Long-term investors should not allow the short-term uncertainty and volatility to shake them from maintaining asset mixes appropriate for their long-term objectives. Time in the market is critical to earning attractive returns.

With another month in the books, the rotation since late-October appears to be entrenching itself. New highs by equal-weight indices and leadership from cyclical sectors is encouraging in our view. Valuation models suggest large-cap growth could continue to face muted returns as elevated multiples normalize, while most other market areas and geographies offer more attractive forward return profiles. Rotation does not signal the end of a bull market. In many cases, it extends the duration by relieving valuation pressure and broadening participation. The sideways pattern of the major indexes may also be responsible for the cooling of investor sentiment seen in recent weeks, which was elevated and one of the more concerning market attributes entering the year.

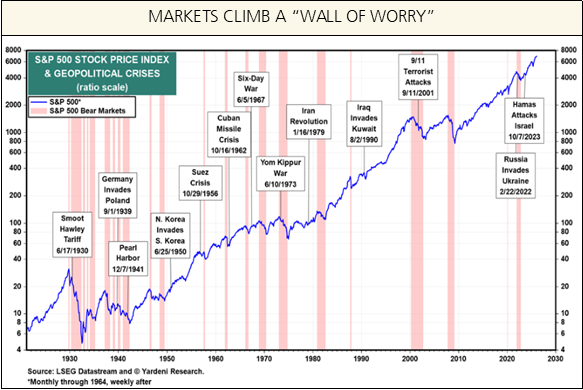

While 2026 is off to an exciting start for client portfolios, we remind clients that midterm election years are historically volatile and the wall of worries seems to be getting taller. Intra-year drawdowns in the double-digit range are common on the path to positive full-year performance. If pullbacks occur, they should probably be viewed as opportunities, supported by the broader backdrop of rising productivity, strong corporate profits, and increased investment.

We advocate clients avoid attempting to predict or trade headlines (which aside from being impossible would also be exhausting and stressful). Instead, we advocate focus on valuation, diversification, and discipline. Periods of narrow and momentum-driven leadership, as we experienced for most of 2024 and 2025, can make diversification feel unnecessary. But periods like the one unfolding now remind us why fundamentals and valuation matter. Markets experience seasons. Market leadership rotates. Narratives swing from euphoria to anxiety and back again. Turn! Turn! Turn! (SONG LINK)