A Complete Game | Steve Henderly, CFA

Printer Friendly PDF: November 2025 Commentary

Scottie Scheffler’s recent run of dominance on the PGA Tour offers a lesson for investors. His average driving distance is 303 yards! As impressive as that sounds to mortal golfers like ourselves, you might be surprised to learn that stat ranks him 70th among his professional peers! While long, powerful drives grab headlines, it’s the rest of his game that sets Scottie apart. It’s his approach shots, short game, and putting which keeps him near or at the top of leaderboard. Monster drives are flashy, but to win tournaments, a more balanced and complete game is usually required. The same could be said of today’s markets. The “Mag 7” continue to drive the major index averages, while the rest of clubs in the “golf bag” – small caps, cyclicals, and international stocks – are struggling to keep pace. Like a golfer relying too heavily on one club, the market’s performance is presently being carried by only the long hitters.

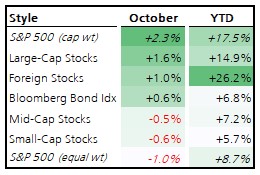

During several trading sessions in October, the S&P 500 index managed to advance even though the majority of stocks declined for the day. How is this possible? Recall the S&P is market weighted, and the 10 largest companies now account for 42% of the index value (an all-time high!). So even though the average stock suffered, the largest companies advanced, pulling the index up. In fact, the S&P 500 index advanced +2.2% for the month, while the equal-weight version declined by -1.1%. This is a historically rare setup. When breadth was previously this weak (250 or more declining stocks vs. advancers), forward performance was often uninspiring or even weak according to Bespoke Research.

During several trading sessions in October, the S&P 500 index managed to advance even though the majority of stocks declined for the day. How is this possible? Recall the S&P is market weighted, and the 10 largest companies now account for 42% of the index value (an all-time high!). So even though the average stock suffered, the largest companies advanced, pulling the index up. In fact, the S&P 500 index advanced +2.2% for the month, while the equal-weight version declined by -1.1%. This is a historically rare setup. When breadth was previously this weak (250 or more declining stocks vs. advancers), forward performance was often uninspiring or even weak according to Bespoke Research.

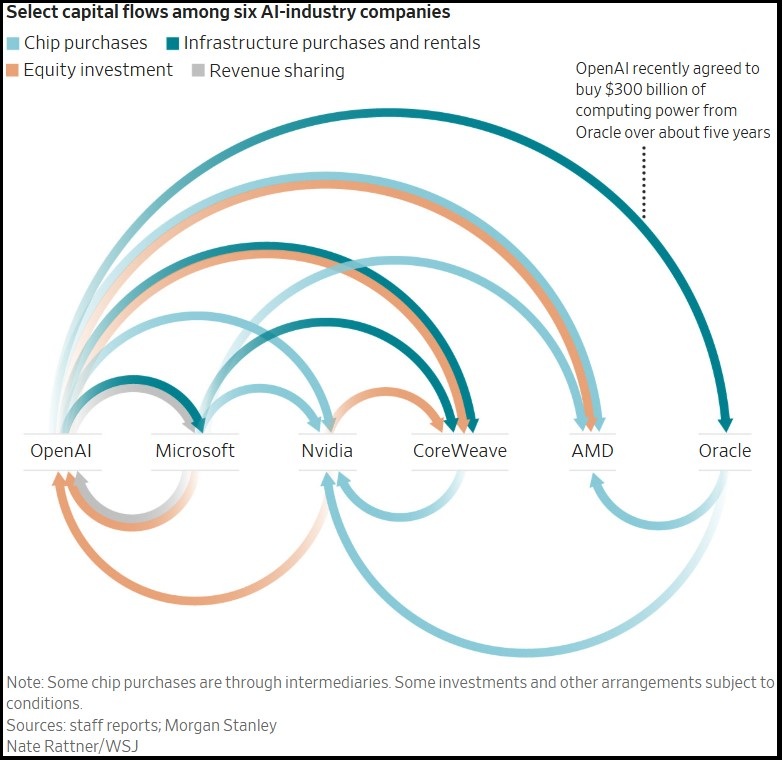

This “top-heavy” performance is once again dominated by the Mag 7 and AI exuberance. A popular chart shared this past month by the Wall Street Journal outlined how various AI companies are now “circularly investing” and fueling AI buzz and high valuations. Surprisingly, outside of this AI-related exuberance, defensive sectors led the markets higher in October. Sectors such as utilities, healthcare, and staples led the S&P 500 for the first time since mid-2022. In contrast to the “go-go” technology sector, these are sectors investors typically flock to during uncertain times. Cyclical sectors such as regional banks, homebuilders, retailers, and airlines struggled. Viewed together with the narrow market breadth, this suggests investors are playing defense even as the S&P 500 and other indexes march higher.

utilities, healthcare, and staples led the S&P 500 for the first time since mid-2022. In contrast to the “go-go” technology sector, these are sectors investors typically flock to during uncertain times. Cyclical sectors such as regional banks, homebuilders, retailers, and airlines struggled. Viewed together with the narrow market breadth, this suggests investors are playing defense even as the S&P 500 and other indexes march higher.

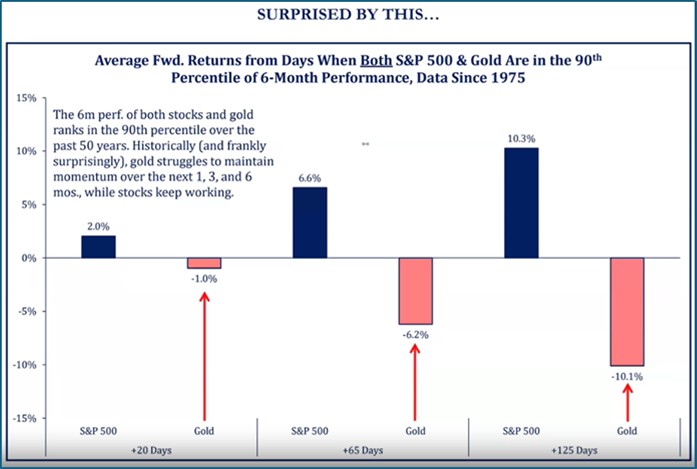

In a similar way, gold (sometimes viewed as a safe-haven relic) outperformed nearly everything, including the Mag 7 and even Nvidia through late-October. Concerns over currency debasement, swelling deficits, and renewed rate-cut momentum drove investors toward what they perceive as safety. Flows into gold and other precious metals hit record highs. We ponder: is a trade safe when the “herd” of money is flocking toward it simultaneously? While gold is a physical commodity (unlike bitcoin), it’s difficult to assess what it should be worth with fundamentals. Ask yourself – what will someone be willing to pay for gold in the future? It does not produce cash flows or pay dividends; it’s not creating revenues or earnings. As Buffett once quipped, gold is “dug out of the ground, melted down, buried again, and guarded”. A good reminder that its value depends almost entirely on perception.

Perception of safety may be shifting. After leaping more than 30% YTD through October 20, gold surrendered 10% during the final trading days of the month. The meteoric rise and flows into precious metals cause some to wonder if its appeal is part of a broader flight to safety ahead. Interesting: when both gold and equities surged together over a six-month stretch, forward returns for gold tend to be poor while stocks play catch-up. This appears to be playing out in recent days. In other words, what many see as a hedge quickly turned into a herd trade. It’s a timely reminder: in markets, crowded safety can be risk in disguise.

Beyond shiny distractions, analysts continue to point to fundamentals as justification for the bull market continuing for stocks into 2026. The Fed delivered a second “precautionary” rate cut in October. Among other things, this rate cut pressured money market rates below 4% for the first time since 2022; it also signaled an end to what is known as quantitative tightening (reducing the size of its balance sheet) to avoid constraining market liquidity. Inflation data, although not yet at the Fed’s stated 2% target, remained low enough with oil prices subdued and wage growth cooling to allow for these accommodative actions. Taken together, the latest cut and stabilization of the current Fed balance sheet are seen as accommodative to the economy. The Fed now appears slightly more concerned about labor market cracks. Chair Powell however was purposeful to push back on expectations for another cut in December and questioned why a resilient economy should justify further easing of monetary policy. Data remains key.

this rate cut pressured money market rates below 4% for the first time since 2022; it also signaled an end to what is known as quantitative tightening (reducing the size of its balance sheet) to avoid constraining market liquidity. Inflation data, although not yet at the Fed’s stated 2% target, remained low enough with oil prices subdued and wage growth cooling to allow for these accommodative actions. Taken together, the latest cut and stabilization of the current Fed balance sheet are seen as accommodative to the economy. The Fed now appears slightly more concerned about labor market cracks. Chair Powell however was purposeful to push back on expectations for another cut in December and questioned why a resilient economy should justify further easing of monetary policy. Data remains key.

Recent “noise” from the government shutdown, now a month long and running, as well as tariff uncertainty, has yet to greatly impact risk appetite. It is increasingly believed that the Supreme Court will rule the tariffs collected so far in 2025 were illegally applied, but the administration believes it can impose them under other sections of trade law. Tariffs are likely to remain part of the backdrop, but companies appear to be navigating them better than most expected entering the year. Corporate profits, continue to expand and are the best defense against recession. Roughly 60% of U.S. earnings revisions over the past three months are upward, and third-quarter earnings are tracking +9% year-over-year, about double the pace of GDP growth. 84% of companies are beating expectations – wow! The market and economy tend to avoid big trouble when companies are still growing profits.

With markets still “running hot,” investors face a familiar temptation: chase what’s working (Mag 7, shiny metals, etc.). Large-cap valuations as measured by price-to-earnings ratio (P/E) appear rich, especially in growth and the technology sector. In recent days, we are hearing reports that Michael Burry – a hedge fund manager known for profiting big for his early and correct prediction of the housing bubble and financial system impacts back in 2007-2009 – is positioning for a selloff in AI-related stocks like Nvidia and Palantir. However, the average stock in the S&P500 as well as mid, small, and international companies continue to sport better relative value. Historically, when small caps break out of extended sideways ranges, the ensuing rally ranged between +30–50%. Small caps finally broke out early this fall. The setup for catch-up performance is there, but the timing depends on follow-through in earnings and liquidity.

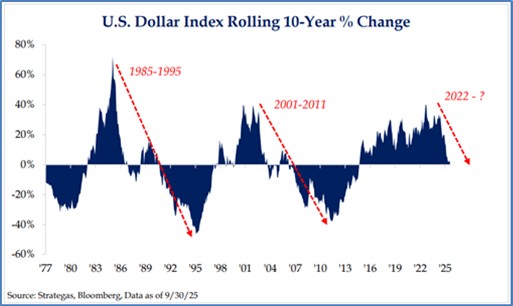

Despite a strong rally YTD, foreign equities continue to trade at significant discounts relative to domestic counterparts, supported by the weakening of the US dollar. In fact, the US dollar is now 10% weaker against a basket of foreign currencies versus the start of this year. This weakening comes on the heels of a decade of US dollar strength which boosted domestic stock performance relative to foreign. Moves in currency tend to be secular. If trade dynamics and a diminishing appetite for the USD drives further dollar depreciation, international stocks should benefit and narrow this extreme discount.

foreign currencies versus the start of this year. This weakening comes on the heels of a decade of US dollar strength which boosted domestic stock performance relative to foreign. Moves in currency tend to be secular. If trade dynamics and a diminishing appetite for the USD drives further dollar depreciation, international stocks should benefit and narrow this extreme discount.

Bottom Line: October brought new highs for the major indexes and client portfolios, but can simultaneously heighten caution and bubble concerns. The Mag 7 is keeping the scoreboard bright, but weakening breadth, defensive sector leadership, and gold’s “safe” parabolic rally (now on “pause”) may prove fleeting. Consistent investing success comes from balance. Having the longest drive, or the flashiest tech stock, doesn’t guarantee a win. In fact, trying to chase the driving power of another player off the tee can be risky. More importantly, it’s the rest of the game that matters for achieving your financial goals over the long-term: valuation discipline, diversification, sound planning, and a steady hand. While fundamentals support the continuation of the current bull market, investors should avoid leaning too heavily on a single driver. Like Scheffler’s golf game, a complete, well-rounded approach remains the proven way.