All Gas, No Brakes | Steve Henderly, CFA

Printer Friendly PDF: September 2025 Commentary

Sports teams love slogans – some memorable, some regrettable. One of the more overused in recent years is the phrase “All Gas, No Brakes”. Catchy yes, but good advice? Probably not. “All Gas, No Brakes” seems apt for describing markets since mid-April: surging forward with little hesitation, fueled by optimism around rate cuts, artificial intelligence, and resilient corporate earnings. The trouble is, cars – and markets – need brakes. Without brakes, even the best things can become unstable. With the return of football and other fall activities, it seems forgivable to again draw analogies between sports and investing.

The economic story in August seemed to revolve almost entirely around the Federal Reserve. A very weak jobs report on August 1st showed just 75,000 jobs added in July plus revisions amounting to 225,000 fewer jobs created than previously believed in prior months (largest revision in 40 years!). The report highlighted softness in the labor market and stood in sharp contrast to cautious comments from Fed Chair Jerome Powell about inflation just a few days earlier in late-July. Immediately, chatter shifted to a Fed that was again disconnected and late to release the “brakes” of interest rates, potentially putting the economy at risk. The report opened the door to Chairman Powell’s recent speech in Jackson Hole highlighting increasing concern with the employment side of its dual-mandate and signaling a rate cut is probably appropriate in September. The market places the odds of a rate cut at over 90% when the Fed next meets on September 17.

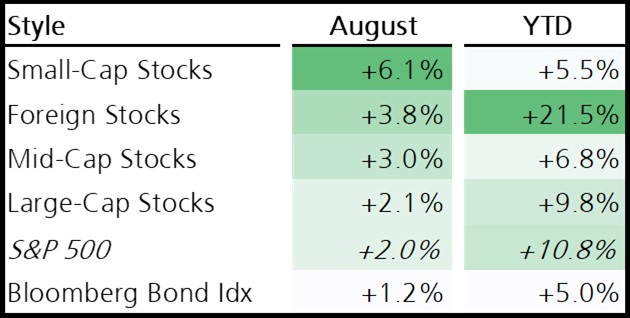

All Gas, No Brakes! Amid a more dovish tone, the S&P500 added +1.9% and notched 4 new record highs in August. While growth (Mag 7) continues to outpace value YTD, breadth improved; 70% of S&P 500 constituents ended the month above their 200-day moving average, a reading applauded by market technicians. Small-size company stocks ripped higher, and client portfolios outperformed risk-adjusted (stock/bond mix) benchmarks. In fact, the best performing stocks from January through July were the softest in August, signaling perhaps rotation behavior. We’re not rooting against any part of the market, but we welcome seeing performance broaden beyond the expensive “Magnificent 7.”

Earnings & Fundamentals

Second quarter earnings reporting dispelled some of the pessimism that tariffs might derail revenue growth. Revenues for the S&P500 expanded 6.3%, the strongest pace in over a year, and corporate America continues to demonstrate earnings growth. The market tends to avoid big trouble when company earnings are still growing.

demonstrate earnings growth. The market tends to avoid big trouble when company earnings are still growing.

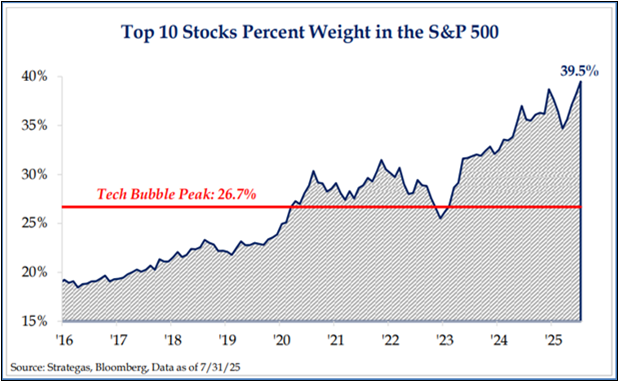

There is a growing chorus of financial news media highlighting that stock market valuations are rich, offering direct comparison to the dot-com era. This is especially true for the biggest US companies; the top 10 in the S&P500 now account for nearly 40% of the S&P 500’s value, with P/E multiples north of 30x. Nvidia alone is worth more than the entire markets of Germany and France combined! Meanwhile, the median stock sports multiples that are lower – around 20x forward earnings.

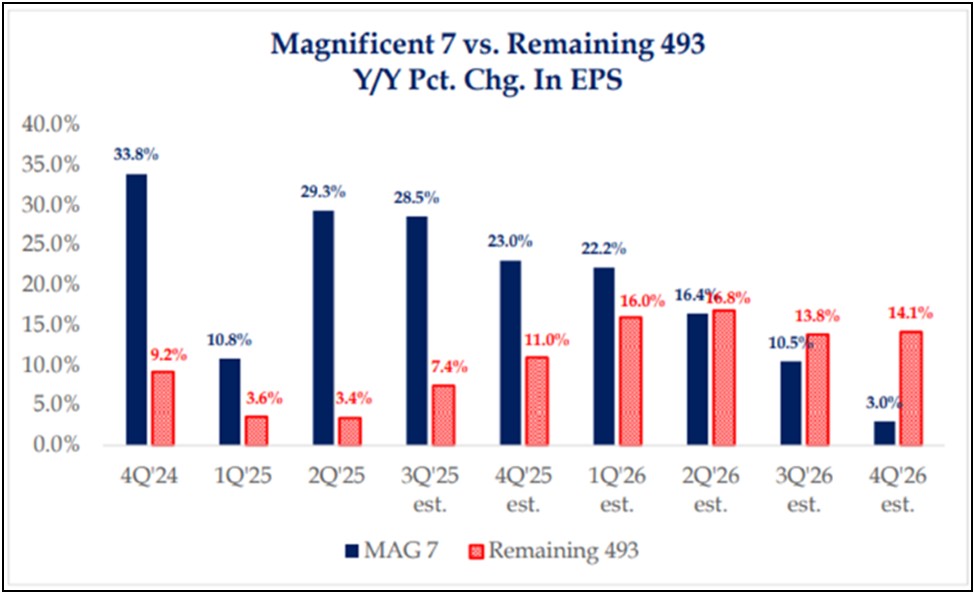

Valuation comparisons to the tech bubble 25 years ago create unease for many market participants. Bullish participants point to key fundamental differences including the largest companies robust growth and substantial free cash flow. Regardless of your persuasion, with valuations high, further multiple expansion should not be one’s base case from here – earnings growth must carry the next leg and/or aid in bringing multiples slightly lower. In that regard, it is encouraging that even if Mag 7 earnings may begin slowing, the remaining 493 names in the S&P500 are projected to be growing at a faster pace by 2Q2026 (historically, the market is forward looking by about 6-12 months). But there are other factors to consider, and potential surprises can resurrect worry for the market, especially when valuations are high.

Policy & Trade

Our commentary a month ago titled “Christmas in July” highlighted how clarity received on tax policy and trade helped extend the markets’ advance since April. Unfortunately, challenges over the legality of tariffs in the courts keep this issue uncertain. Just last week, the US Court of Appeals rejected tariffs enacted through the International Emergency Economic Powers Act (IEEPA). This was widely expected, and a backup plan for tariffs on different legal footing exists, but revenues collected via tariffs so far may need to be rebated. We will not know that until the Supreme Court hears the case and issues a ruling which likely will not arrive until early 2026.

advance since April. Unfortunately, challenges over the legality of tariffs in the courts keep this issue uncertain. Just last week, the US Court of Appeals rejected tariffs enacted through the International Emergency Economic Powers Act (IEEPA). This was widely expected, and a backup plan for tariffs on different legal footing exists, but revenues collected via tariffs so far may need to be rebated. We will not know that until the Supreme Court hears the case and issues a ruling which likely will not arrive until early 2026.

Looking Ahead – Where’s the brakes?!

Interest rates and inflation, if rising, act like brakes for the economy and stock market. Rebate of tariff revenue, if ultimately required, would pressure deficits in the short-term and could re-awaken fixed income markets causing rates to drift higher on longer-term debt. Bond vigilantes appear to be stirring; rising yields on foreign sovereign debt as well as longer-maturity US Treasury securities are making recent headlines (30-yr yield near 2008 highs). Remember the Fed only controls short-term interest rate levels. Rates of longer maturity can behave unpredictably, particularly given the interplay between tariffs, global trade, inflation, corporate pricing power, and yes – the level of government debt (both US and abroad).

August closed near record highs, with markets pricing in multiple Fed cuts in 2025 and into 2026. This, combined with the recent passed tax package is widely believed to benefit both consumers and businesses as the cost of borrowing money should decline, fueling the economy’s continued resilience. Markets, forward-looking, probably already moved on this expectation in the short-run.

Performance YTD is encouraging, yet sentiment may be getting too rosy as investors embrace optimism around rate cuts and AI-driven capex, while downplaying lingering uncertainties tied to tariffs and earnings durability. For investors, an “all gas, no brakes” mentality doesn’t typically persist for long stretches. Momentum of the Magnificent 7 carried markets higher since late-2022, but brakes – in the form of valuation discipline, earnings scrutiny, and patience – are essential. With the calendar turning to September, investors should not be surprised if we see seasonal chop. We are reminded that just 40% of September’s conclude with gains. Stay calm. We look for consumers and businesses to power the next leg of market gains from late 2025 into ’26.