Rising Oil, Rising Markets – Now What? | Steve Henderly, CFA

Printer Friendly PDF: May 2026 Commentary

It’s no secret that high oil prices are generally a drag on the economy and stock market. We witnessed the negative relationship in March as oil spiked and stocks fell with the onset and uncertainty of the Iran war and closure of the Strait of Hormuz. But… scratch that, April Fools! Beginning in April, oil prices didn’t matter. Yes, an apparent ceasefire between the U.S. and Iran was welcome news and provides hope the worst of the conflict is over. But shipping through the Strait remains blocked and oil/gasoline prices ended April near their highest levels in four years. Oil prices up, stocks…up?!? As we move into a new month, does the backdrop suggest one should “sell in May and go away”?

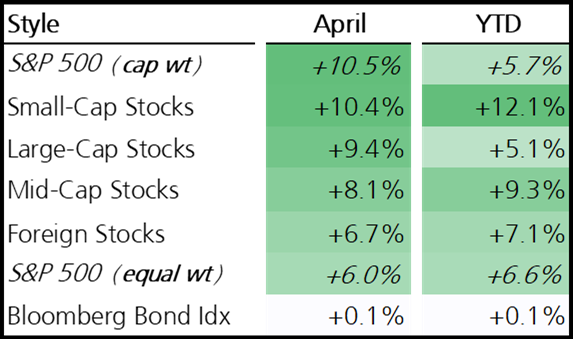

Stocks raced back to pre-war levels and beyond in April with the S&P 500 establishing 8 new record highs during the month. In fact, the S&P 500 experienced its best month since the 2020 covid pandemic rebound with a gain of +10.5%. Wow!

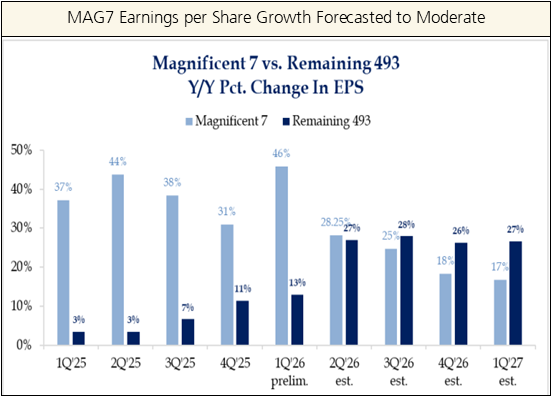

Virtually every area of the market rebounded in April, with enthusiasm being most visible from the Magnificent 7 jumping +20% after lagging meaningfully since last October. This performance, coupled with the group’s huge collective weight helped drive the S&P 500 materially higher. As observed in the chart to the right, earnings growth among the group remains huge, but is expected to slow while the broader market takes the baton. The traditional size-weighted S&P 500 significantly outperformed the equal-weight version during the month, illustrating once again how concentrated index returns can become when leadership narrows.

Client portfolios, which concluded 1Q in positive territory even as the S&P 500 was decisively negative are still ahead year-to-date, while diversification with broader exposure lagged in April. We remain of the perspective that the most attractively valued areas of the market sit outside the Mag 7 and provide better risk-adjusted return prospects long-term. Prudent portfolio construction is designed to manage risk during full market cycles. We prefer to buy assets at attractive prices with confidence that time will make us successful.

April is another reminder that investors are often rewarded when uncertainty is high. Beneath the surface, many market concerns remain unresolved. The ceasefire helped calm investor nerves, but the broader conflict is not confidently settled. Negotiations remain uncertain and there appears to be little clarity regarding who is in charge in Iran. Tensions around the Strait of Hormuz are threatening the durability of the current ceasefire. In many ways restrictions in the Strait are even more complicated than a month ago with the addition of U.S. blockade enforcement actions and continued geopolitical friction, which explains why oil prices continue to float higher. Experts suggest that even if the Strait were reopened “today”, it could take months for shipping flows, inventories, and pricing pressures to normalize. That also means broader inflation uncertainty persists as well.

Despite the geopolitical fragility, investor sentiment recovered meaningfully in April. It’s remarkable how strongly attitudes follow prices. Survey data confirms the shift; pessimism eased significantly but sentiment remains below the exuberance that characterized the market’s highs heading into 2026 and through mid-February. That’s probably healthy. A wall of worry is historically more durable than a market propped up by universal optimism; residual skepticism may support the case for continued gains.

What’s behind the swift market recovery and seemingly “flippant” perspective concerning oil prices? Resilient economic data, strong corporate earnings, and renewed enthusiasm surrounding artificial intelligence are the most cited supports.

Earnings Winning the Tug of War… For Now

We entered 2026 with the expectation for an intense tug-of-war between productivity (can AI deliver new efficiency?) and inflation (lots of money must first be spent to deploy and power new technologies). Corporate earnings season is notably strong. With more than 70% of companies in the S&P already reported through April, aggregate S&P 500 profit growth is on track to post a crazy +27% year-over-year advance. That’s well above long-term averages, and revenue trends are staying constructive. Demand, and clearly profits, are holding up better than many feared despite geopolitical noise and higher energy costs. While markets moved quickly, they were responding in part to a corporate backdrop that continues to demonstrate resilience. When profits are expanding at this pace, the broader economy tends to avoid big trouble and is more durable than headlines imply.

Results so far suggest that productivity is winning, but the strains in the Middle East intensify the tug-of-war with inflation. If productivity gains tied to technology, AI, and business investment continue accelerating (without resulting in mass employment layoffs), the economy may absorb higher costs more effectively than expected. If inflation wins, particularly due to sustained energy pressure, interest rates and financial conditions could become more restrictive, and earnings growth could begin to slip.

The Federal Reserve remains stuck in the middle of the tension. At its April meeting, the Fed again chose to hold rates steady. The decision was accompanied by a rare statement/dissent from three (a growing minority) regional Fed presidents that language implying an easing (rate-cutting) bias be dropped. This signals concern is building on the FOMC that inflation pressures tied to higher oil prices may warrant a rate increase rather than a rate cut. With high prices at the pump and a rate hike, consumers and business sentiment would really take a hit. We doubt the Fed wants to tighten (raise rates) into an energy shock. Jerome Powell, whose term as chairman is ending in May, also indicated he intends to remain on the committee, adding another layer of uncertainty with a transition in leadership.

Entering May, markets may indeed be underestimating lingering geopolitical and inflation risks. Volatility could re-emerge at a moment’s notice (particularly if ceasefire falters). Investor optimism surrounding AI, productivity, and fundamentals like earnings growth appear to be offsetting traditional macro concerns. History suggests that the often cited phrase “sell in May and go away” is unreliable at best, with April being the latest example that markets often behave differently than the most prominent headlines might suggest. Key thought: avoid worry by remaining a long-term investor.