Highlights from our latest Nvest Nsights newsletter:

- The Bumps We Climb On – If you knew stocks would experience two bear market drawdowns over the next four years, would you be willing to own them in your portfolio?

- The Next “Financial Eclipse” – Just as the moon veils the sun’s brilliance, we will all experience various “financial eclipse” events in our life.

- Mission (Not Yet) Accomplished – Inflation data disappointed to the high side two months in a row suggesting the Fed should not rush to cut interest rates, yet markets marched higher. What lies ahead?

Click here for a Printer Friendly PDF which also includes benchmarking and data on investments widely utilized in our current tactical strategies.

The Bumps We Climb On | Steve Henderly, CFA

El Capitan is the famous rock formation that rises three thousand feet from the floor of Yosemite National Park in California. From the ground, the granite face of the formation looks smooth and nearly vertical. Yet up close, one will observe many bumps, cracks, and small ledges. These inconsistencies make conquering El Capitan possible.

El Capitan is the famous rock formation that rises three thousand feet from the floor of Yosemite National Park in California. From the ground, the granite face of the formation looks smooth and nearly vertical. Yet up close, one will observe many bumps, cracks, and small ledges. These inconsistencies make conquering El Capitan possible.

Funny how investing can be described in this same fashion; when up close and looking at day to day or even month to month movements, a chart of the market looks like a random walk, littered with significant up and down gyrations. When you zoom out, the picture appears much smoother and generally upward sloping – a very rewarding experience.

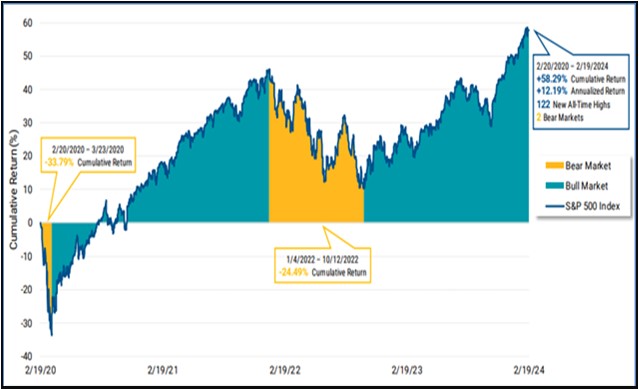

Believe it or not, it’s been four years since the World Health Organization officially declared COVID a pandemic and investor anxiety spiked. After weeks of gut-wrenching declines, the S&P500 fell nearly -12% on March 16, 2020, the worst single-day decline since Black Monday in 1987. The 11-year bull market – the longest in US history – officially died. Following this steep sell-off, a rapid recovery ensued, driven by massive government stimulus and a new market high was achieved in August of 2020. Investors continued to enjoy new all-time highs through most of 2021 until the market peaked in January of 2022. By this time, it became clear that high inflation would require forceful action by the Fed via higher interest rates. These rate hikes ushered in the bear market of 2022 with the S&P dropping 27% before a bottom was achieved on October 12, 2022.

If you knew stocks would experience two bear market drawdowns over the next four years, would you be willing to own them in your portfolio? Maybe not, but this is exactly what happened over the past four years. Remarkably, despite this difficult environment, the annualized return for the S&P500 is above the market’s long-term average. Diversified client portfolios experienced attractive progress too; this is demonstrated via 5-year returns which we include in each quarter’s report.

the past four years. Remarkably, despite this difficult environment, the annualized return for the S&P500 is above the market’s long-term average. Diversified client portfolios experienced attractive progress too; this is demonstrated via 5-year returns which we include in each quarter’s report.

It is fascinating to review long-term investing in this context, because most of us still vividly recall how we felt during COVID, as well as the 9-month bear-market that began in early 2022. Since the bear market low in October 2022, the experience moving forward was anything but smooth – with wars abroad, bank failures, and worry about economic recession. While the events of the last four years are unique, market bumps are not. On average, the stock market experiences a -10% or greater decline every three years; slightly more than half of those continued to slide -20% or more (or once every six years, with the average full drop being -28%).

Declines of this magnitude are always painful and recovery takes time. But some element of time is on most investors’ side. Establishing an investment objective one can stick with through both good times and bad is imperative. History proves that with time, we will be winners; the market climbs to new heights despite these regular bumps. Now imagine that you not only remained patiently invested over these periods, but regularly deployed new money often at more attractive values. Doing so created a supercharged rebound to new heights. Similar to climbing El Capitan, these bumps are crucial for investors’ portfolios to climb to new heights.

Warren Buffett offers to shareholders this year, “Never risk permanent loss of capital. Thanks to the American tailwind the power of compound interest, the arena in which we operate has been – and will continue to be – rewarding if you make a couple of good decisions during a lifetime and avoid serious mistakes.” It’s encouraging to hear the famed, disciplined investor remains long-term bullish on the prospects for investing.

The Next “Financial Eclipse” | Jordan Ranly, MBA

We hope your year is off to a nice start! Our Nvest team is enjoying an exciting start to 2024, and we are feeling settled in the new office space at 9757 Fairway Drive. Please schedule a time to visit!

Unexpected financial challenges can obscure from view well planned goals – a sort of “financial eclipse”. Just as the moon veils the sun’s brilliance this month, we too will experience various “financial eclipse” events in our life. An organized and holistic financial plan can illuminate the path forward even during challenging times. LIVING LIFE Financial Planning is here to help.

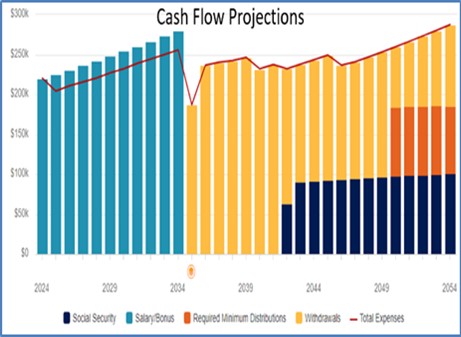

What exactly is LIVING LIFE financial planning? Quite simply, LIVING LIFE is our method to deliver financial peace of mind and empower clients with the information they need to make educated decisions throughout the stages of life. Many of our wonderful clients are now fully engaged with LIVING LIFE, including the utilization of our client portal which provides you a real-time view of your full financial life.

The portal is a powerful tool to fully organize and retain important records, map out cash flow needs, and project financial health many years into the future. Similar to our goal of building a diversified investment portfolio, LIVING LIFE is designed to cover all areas of financial life. Once a detailed balance sheet and cash flow is constructed, our team is equipped to provide personalized and pointed advice in numerous areas – from preparing for college, to retirement planning, estate planning, and more.

One common area of support is insurance planning. Nvest does not sell insurance, nor are we fond of many insurance products, but we do understand the importance of risk management. With a detailed balance sheet and cash flow needs, our team is in a position to offer pointed advice on the types and amount of insurance necessary. Is long-term disability insurance appropriate? What about long-term care or can you “self-insure”? Is current life insurance coverage adequate or still needed? If so, should you own whole life or cash out and purchase a term policy? What are the tax consequences?

Speaking of taxes, tax management is always an area of high interest. Within the law, most clients are inclined to optimize their tax liability (and minimize Uncle Sam’s piece of the pie long-term). A few strategies we explore include qualified charitable distributions (QCD’s), Roth conversions, municipal bonds, and contributions to retirement accounts (pre vs. post tax).

Steve & I enjoy this area of our business as much as the investment & portfolio management because it’s what makes purposeful investing possible. It is thoroughly satisfying to see the “light bulb” turn on once a client can visually see their current financial situation and projections many years into the future – fully prepared for the next financial eclipse.

LIVING LIFE financial planning is an included service for Nvest clients and is a key component of our promise to deliver financial peace of mind. Please reach out if you would like to learn more or there are new scenarios on your mind for us to help study.

Mission (Not Yet) Accomplished – Portfolio Review & Outlook | Steve Henderly, CFA

Investor sentiment was elevated as we entered 2024 and continues to date. Elevated sentiment can last a while; yet elevates investment risk in areas of high valuation. When expectations are too rosy, any shortcoming can create volatility. For instance: what if inflation data stops improving and prevents the Fed from cutting interest rates as soon or as much as market expectations; how about election year uncertainty, global shipping disruptions; or renewed regional bank stress jeopardizes the hoped for economic soft-landing?

The biggest surprise about this economy is that it just keeps chugging along despite Fed efforts to slow it down. Everything from stocks, to bitcoin, to gold marched to new records during the 1Q, exceeding even the most optimistic predictions. The US economy (and stock market) is proving resilient despite some small cracks in the labor market suggesting growth should eventually slow down. To date, hints of market weakness seem to evaporate within a few trading sessions, as investors quickly buy any dip; the largest drawdown for the SP500 during the 1Q was just -1.7%, a far cry from the average intra-year drawdown of -14%. Below we highlight a few of the key dynamics we are following most closely:

- Inflation data disappointed to the high side two months in a row suggesting the Fed should not rush to cut interest rates, yet the market still appears to desire cuts?

- With productivity strong and labor markets steady, it’s arguably more risky for the Fed to cut rates right now. Rate cuts could reignite a new wave of inflation. Some Fed members oppose cuts at this point, believing there is pent-up demand in certain businesses and sectors which will be unleased if interest rates decline.

- While the markets seem eager for rate cuts, history interestingly shows that the market does best when the Fed is on hold/pause. The longer the pause, the better the equity returns. This suggests investors should favor a patient Fed and resilient economy, rather than hoping for cuts.

- Currently, the world’s monetary authorities seem to be pulling in different directions, with a number of key central banks favoring cuts. If manufacturing is bottoming and possibly starting to recover, we should watch for upward price pressure in commodities including energy (which seems to be occurring – both areas still owned tactically in client portfolios).

- It appears the Fed is willing to accept higher inflation. But will ‘Bond Vigilantes’ remain quiet?

- Bullish until the bill comes due was the investing mantra for most of the decade following the Great Financial Crisis. The idea was that as long as cash and fixed income yielded “zero”, there was no alternative to owning stocks for a return on one’s money.

- In this election year, it’s probably no coincidence that the Treasury is shifting the way it finances current spending to avoid draining liquidity from the stock market to keep consumers feeling constructive.

- Presently, interest rates elevated vs. the prior decade, the cost of money/financing is no longer “free”. Bond vigilantes (interest rates) swiftly increased pressure between August and October last year due to rising government debt levels. But since the Fed paused rate hikes, the bond market appears disinterested in the level of government debt or spending. A key tell if ‘the vigilantes’ are becoming agitated again is to monitor 10-year US Treasury yields; a move materially back above 4.35% suggests concern and probably causes stocks to stall.

- One current thesis keeping bond markets benign (and stocks buoyant) is that AI can fuel a boost in productivity and grow the economy faster than the pace of debt in the years ahead.

In light of these dynamics, it’s easy to “worry” if good times can continue or is the market near a top? Entering the 2Q, market participation is broadening and better than throughout most of 2023 when just a “handful” of mega cap tech stocks, the “Magnificent 7”, moved the indexes forward. All but one of the 11 sectors in the S&P500 rose during the 1Q and more than 86% of stocks are above their 200-day moving average. This is encouraging, suggesting most companies are faring better than a year ago when the overwhelming consensus continued to anticipate a mild economic recession rather than soft landing, and most stocks floundered.

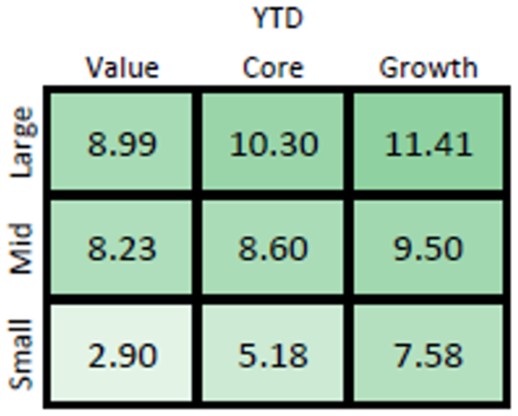

A quick glance at the domestic style map (left) and noted in client portfolios, mega-cap growth stocks still lead other categories. This also causes the performance of the S&P500 (size-weighted) to be skewed: +10% vs. equal weight S&P up +7.9% YTD. Value stocks trail the expensive high expected growth and momentum companies, but emphasis on quality (strong-balance sheets, high free cash flow, etc.) narrows this gap. We are seeing strong performance from Energy (RSPG), and commodities, after churning for much of the last 9 months, seem to be finding a spark (hint that inflation may be ticking higher). Abroad, Japan is “red hot” after nearly 40-years of no benefit. Bonds, particularly core, remain “stuck” like the Fed. If/as the Fed begins cutting rates, we will see positive price adjustment that adds to their return from yield.

History suggests that while the market may be short-term overbought and due for a breather, major market tops do not usually occur from these conditions. Momentum is not something to fear. As for the election, past experience reveals that too, is not an item we should fear; since 1944 there were 13 presidential re-election years (meaning current president is sitting for re-election), none produced negative returns. Client portfolios are tactically mixed well for the current outlook and environment. Even the solar eclipse should not dim performance opportunity.

Someone once said, “You don’t need to do anything, but you need to be aware of everything.” We like how portfolios are positioned against this backdrop.

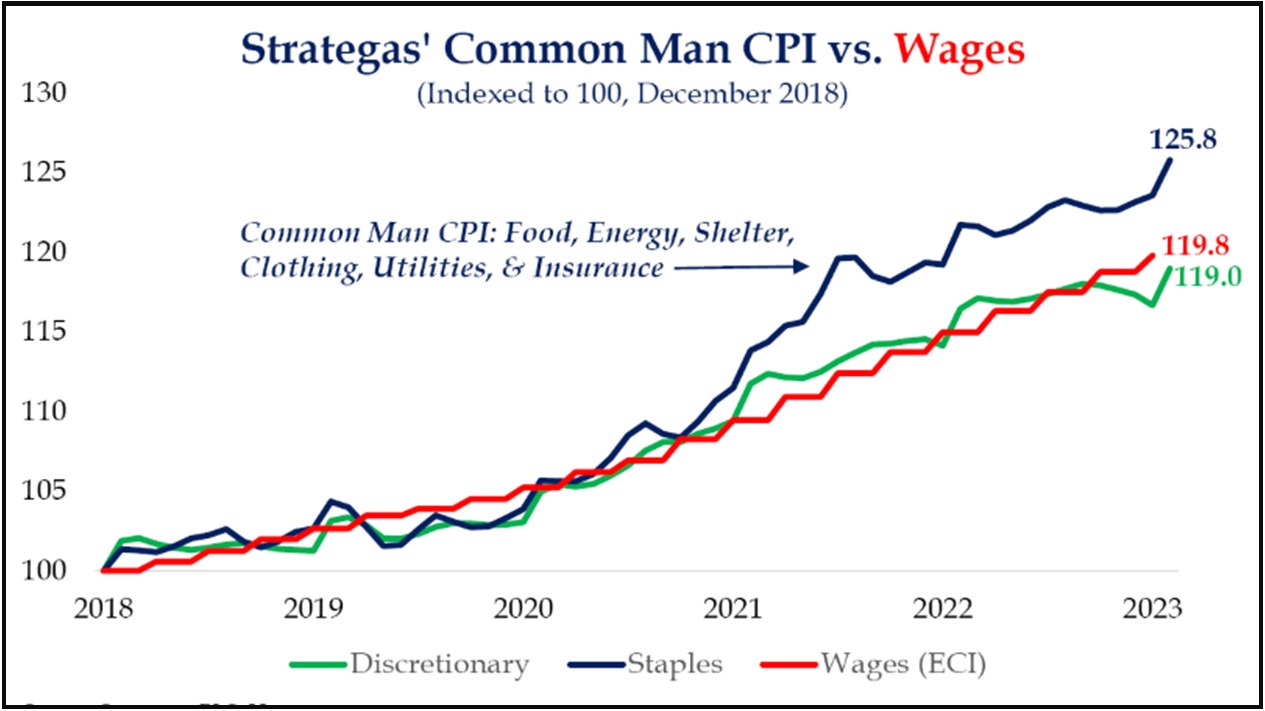

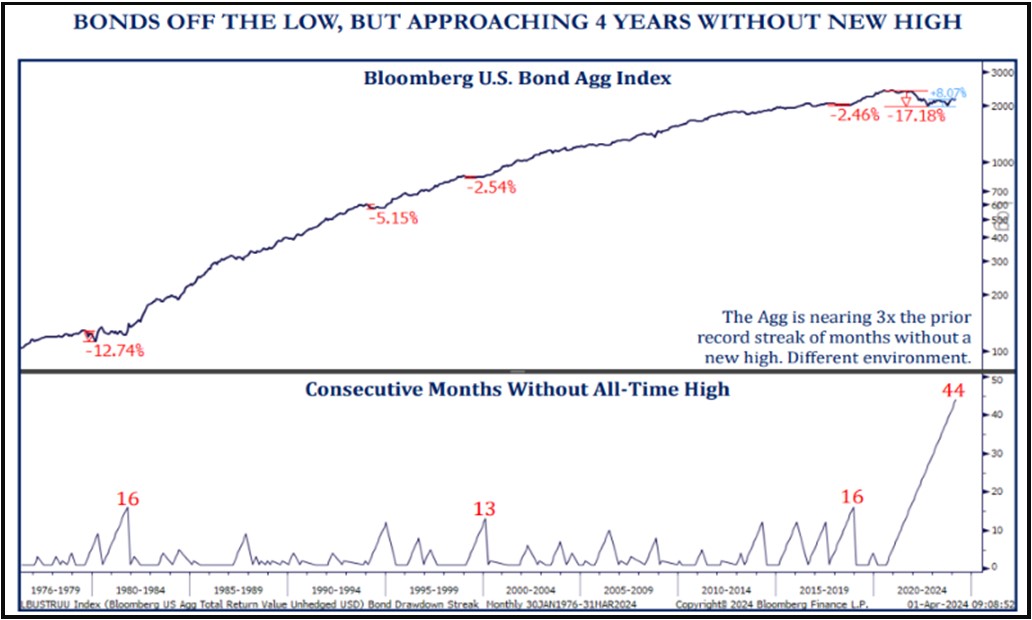

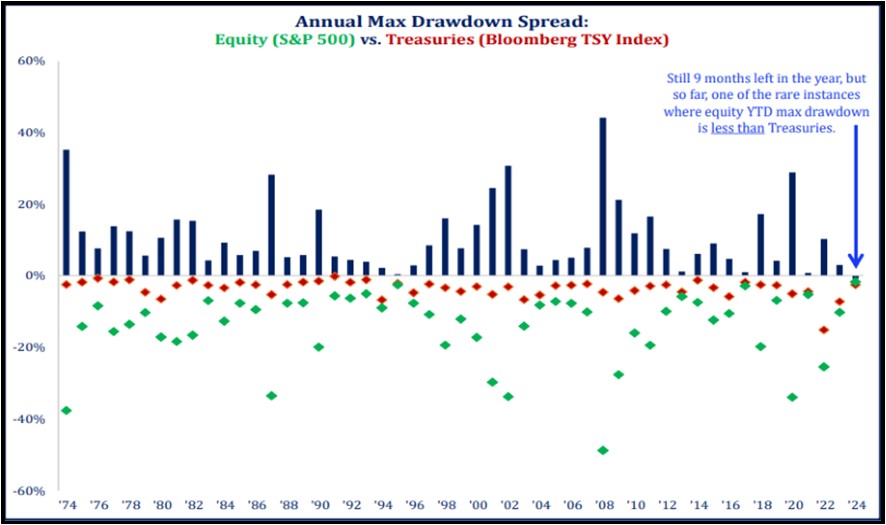

Charts of Interests (Credit Strategas):

Chart explains sour public sentiment on economy despite resiliency:

Fixed income still recovering from historic 2022 drawdown:

Only 3 months in, but unusual for stocks to be less volatile than bonds:

The Eclipse could Bring $1.5 Billion Into States on the Path of Totality: