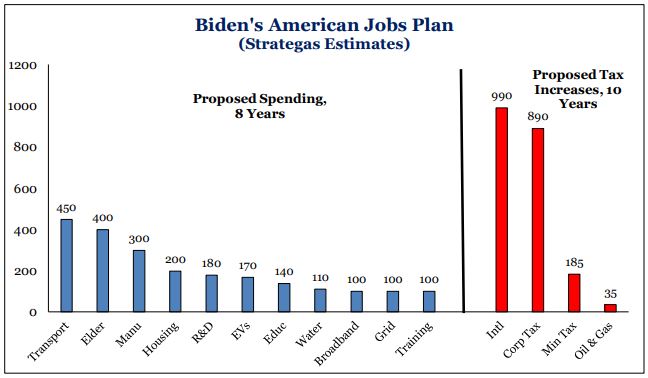

The first quarter offered lots of “candy” (government spending) and no “spinach” (tax increases). But that idea started changing in April with government policy shifts: the unveiling of big infrastructure spending (spread over 8 to 10 years), plus new large-dollar child spending programs; both to be funded with higher taxes – corporate and individual. Taxes are oriented as an aggressive path to pay for massive spending. At present, the combination of extraordinary fiscal spending and monetary stimulus is pulling forward demand, output, revenue, profitability and investment (perhaps stealing it from 2022 and maybe beyond; called a growth hole). After such a strong start to the year, and remarkable 12 month recovery, the biggest hurdle the market faces is high expectations and crowded positioning. At present, there appears to be a peak in positive data and eager market participation (number of stocks rising at the same time), usually found in the first third of a new bull market run. With so much good news already priced into stocks, any bad news or “miss” could spark near-term volatility. So let’s ask… Is this as good as it gets?

April was the best month of 2021 for client portfolios; and best rolling 3-month interval during the last 8 months. Portfolio values continued to appreciate nicely. It is tough to get too cautious on stocks even as they established 10 new highs in April making a total of 25 new highs during the past 4 months. The new bull market which started March 23, 2020 is now 13 months old – rising +90.6%, the fastest rise ever. Investors are excited with the attractive growth and returns in their portfolios. Some are wondering if it’s appropriate to undertake broad de-risking of equity exposure. De-risking is not recommended because the full global market is not re-opened yet; and there are not excesses appearing in economic data. Saying it differently, it is unwise to be under-exposed to stocks with money supply (M2) still expanding at an annualized pace of more than 25% – the monetary policy continues to be the strongest pillar upon which the current bull market resides.

While these early bull market returns are exciting, we should recall that the second year of a new bull market is usually upward, but less robust. Also, it coincides with the first year of a new administration. History reveals both factors tend to produce an upward full year result, but with increased volatility. Market valuations are extended while underlying economic and company fundamentals need to “catch-up” or narrow the valuation gap. Also, every change in administration since 1950 creates market concern as the market does not know how new policy ideas/proposals will affect future economic and market conditions. Thus, there is likely a pause or even a market correction (10% or more) during 2021. But it is important too, for the moment, that there are no sinister signs of stress showing in the bond market (which would arise from rising inflation/interest rates) to signal that markets are becoming concerned a policy mistake is in the making. Thus, while volatility and market churning are probable and create a natural feeling of frustration; volatility/pullbacks are unlikely “fatal” to the new bull market and its continuation.

Returning to our question, “Is this as good as it gets?”… Well, it’s tough to get better than the best. Let’s review several underlying market/economic data and expectations:

- 2021 economic real GDP (before inflation) is expected to reach +7% with nominal GDP reaching 10% (includes 2.5% inflation) – levels not experienced since 1983.

- Profit growth is advancing +25-30% this year (it’s already factored into stock prices during the last year).

- The Fed is currently focused on only one part of its mandate – until full employment is restored it will be tolerant of higher inflation.

- An inflation scare is inevitable given the level of savings, stimulus payments, re-opening albeit with supply-chain challenges, and wage competition from unemployment benefits (equate to about $23/hour).

- Each recent economic stimulus package, on its own, would be the biggest fiscal initiative in the past 50 years. It’s “a trillion here, a trillion there.”

- More than 56% of the US debt owed to the public ($21 trillion) matures within 3 years; the weighted average interest rate is 1.38% (low; if rates rise, the cost of debt/interest will quickly increase); the size of the Fed balance sheet increased in size by nearly 90% since last year (represents roughly 35% of GDP).

Life is getting easier for most – economic conditions are better, re-employment is continuing – as we move further into the post-COVID world. Globally, most of the industrial world is benefiting from economic growth. Yet, there are many supply-chain exceptions creating product shortages and slow deliveries. This is observed looking at input prices which rose for the 11th straight month; highest reading since June 2008. Most industries are still operating below their pre-pandemic capacity utilization level, which contributes to the output (product) limitations. This is where inflation originates and grows, and it bears watching. The huge size of fiscal and monetary stimulus pulls future economic growth forward into 2021 creating product shortage with higher prices. It could create a potential growth hole in 2022 and beyond unless there is more deficit spending in the future. But, if we add tax increases (proposed), the economic hole will grow bigger; taxes are a fiscal drag on growth. Is this as good as it gets, because it will be a great challenge to continue stimulating aggressively?

Economic volatility is continuing to translate into political volatility. The markets will try to gauge expectations – government policy interference is huge (stimulus with taxes seems contradictory); more than needed for the economy to heal and grow on its own. Unfortunately, history reveals that dramatic shifts in social policy using economic levers, generally wreaks havoc on market-driven systems in the intermediate-term. These statements are not meant to create or cause alarm, though that is possible and understandable. With investing, remember that nothing is permanent, good or bad. It becomes a bad experience when worries cause one to make dramatic portfolio changes on the prospects (belief) that the current path is incorrect. Markets are smarter than headline news.

What’s the market saying about new policy direction since April (new spending and tax ideas)? In general, it appears the market character is changing due to policy directional announcements:

- Rising bond interest rates (from 1% at yearend to 1.6% recently on the 10-year Treasury) mean the economy is expanding; this rise is normal. Rising rates bear watching though, as they can also be a signal of rising inflation expectations – due to the current broken supply-chain bottlenecks, and huge fiscal spending.

- Stock themes are shifting or rotating. Industries/companies believed to be most directly impacted by proposed tax increases are underperforming (impacts future earnings). Tech and healthcare are showing the most negative performance impact. Companies with high domestic income appear least at risk. In 2017, high tax rate companies were the winners of the Trump tax cut and ironically are continuing to be least at risk under the proposed Biden tax plan – these include apparel retail, industrials, and financials (all areas that lagged in the last bull market and early in this new bull market). There is also an innovation paradox – companies critical to post-COVID recovery are also most at risk for higher taxes; failure to correct the computer chip shortage (various sub-industries) plaguing US manufacturers will see higher taxes; similar risk exists on the healthcare side and front-line companies addressing the COVID. Maybe the legislative process will moderate the tax impact.

So, is this as good as it gets? It is important to keep investing through time – make small changes as conditions evolve. But dramatic changes are ill-advised. They lead to poor performance and wealth alteration. Political noise is certain. It requires awareness, but not radical reaction. It is wise to retain a historical perspective – time is an investor’s greatest ally; long term pursuit of an appropriate asset allocation mix (stock/bond) is rewarding.

Printer-Friendly PDF – “Is This as Good as it Gets”