We hope you are enjoying summer and sunshine. Unfortunately, the financial markets remain stuck in a “storm”. After the difficult first quarter, pain accelerated during the 2Q. There was no place to hide; bonds and stocks together experienced a 2nd consecutive negative quarter each – a somewhat rare occasion.

Against this backdrop and with so many big worries without easy or quick resolution (inflation, Russia/Ukraine, Fed that is intentionally trying to slow the economy to balance supply & demand), it can become challenging to maintain a longer-term perspective. Our newsletter this quarter provides the following context:

- “GIGO” – Do your best to control the type of information you consume, as well as how you react to it. What version of “GIGO” will you be?

- “The World Changed” – A review of market action so far in 2022 and context from history providing clues to what might be expected from here.

- “Bills to Pay” – The “cost” of fiscal and monetary stimulus pursued by governments around the globe in response to the Great Lockdown is being paid in 2022. How is the bill being paid and how long will that last?

- “iPod, iPhone, iPad… now the I Bond” – What are I Bonds, and are they for me?

A printer-friendly version of the newsletter, including benchmarking and fund performance data, can be obtained here: Q2 Nvest Nsights.

We realize how troubling is the current market environment and are here for you. We continue to monitor the backdrop, and be intentional about managing portfolios tactically. Please do not hesitate to call, email with questions, or to coordinate a time to visit together.

GIGO

In computer science and mathematics, the quality of output is determined by the quality of the input. Or, as most know “garbage in, garbage out.” Such is an appropriate idea during any troubling time and especially true for investors now. We last witnessed GIGO in February/March 2020 when COVID created the Great Lockdown. Many spent too much time watching and listening to media – news, social media, and similar which fostered great emotional worry. So too today; there is way too much negative media about everything, including the economy and financial markets. How do you stay positive? How do you stay on your plan; your path?

Be intentional about what you put into your mind – what you hear, read, and watch. GIGO, “garbage in/garbage out” is quick to modify your future. We must be intentional to restate GIGO. It can alternatively mean “good in/good out.” “Our attitudes determine our altitude” (John Maxwell). If the nose of a plane is pointed down, it will fly into the ground. If the nose is pointed up, it climbs. So too with our mental attitude.

Recall Y2K? Were you worried? That event was over 20 years ago. The fear was that computers would crash because they could not make the change from 12/31/1999 to 1/1/2000. Many “experts” suggested taking money out of the bank because the computers would crash and account balances would be incorrect due to Y2K. Looking back (perspective), Y2K was nothing more than a new millennium. Many individuals incorrectly listened to the “wolf.” Myopia is present today; it is seeing only problems; whoa me! What a mess. Problems are immediate/now, and often lead to taking wrong action. Amnesia is also present today; it is not remembering the past; the many blessings and good. We lose sight of the long path that history provides.

It is very important to review the long path, the history of the financial markets. Reviewing over 100 years of financial market history shares a couple of key thoughts – stocks beat bonds, often, and by a lot. And, it is appropriate to own more stocks than bonds, particularly to beat investors’ enemies of taxes and inflation. Yes, “rainy” days are part of the history of the financial markets. Yet, history advocates that all investors retain their focus – follow your financial plan – stay invested through it all (never try to time the markets; it’s always arriving late to the “party”). Time allows the magic of compounding returns to work to your benefit; compounding is truly magical. That’s best achieved by being a “Rip Van Winkle” investor – taking a long nap which avoids hearing “garbage in” and remain invested through the ups/downs/ups.

Investors need to stay informed; need to do their research. The key is what’s the quality of the “research” being studied? Listening to too much “bad news” media that continually yells “wolf” is certain to ruin future success. We contribute to our own mental health; we contribute to our financial success. “The greatest discovery of all time is that a person can change his future by merely changing his attitude” (Oprah Winfrey). GIGO = focus on “good in/good out!”

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc

THE WORLD CHANGED

An old adage: there are two types of economists – those who don’t know, and those who don’t know that they don’t know. Most economists are in the same boat. They make educated “guesses” based on experience. Doesn’t that sound similar to trying to predict the next move in the financial markets?

2022 is proving to be the “Year of Rates” – inflation and interest rates. Collectively the financial markets generated their worst monthly returns in June. That means 2Q was worse than 1Q; together the YTD is troubling, even disturbing. There was no place to hide. Bonds experienced their biggest selloff in 40 years during the first half with the Bloomberg bond aggregate dropping -10.4% (short maturities fared better). Stocks were spooked too (and it’s not Halloween or October) as the S&P500 dropped -16.1% during 2Q and -20% for the YTD; tech stocks were rocked. The average domestic stock fund is down over -16% (YTD and last 12 months). And cryptocurrency values imploded, down -72% since November (was it really risk adverse?); it’s a “teenager” again! In the “Year of Rates” all eyes are focused on the Fed – their monetary policy actions of raising interest rates are aimed to fight inflation, embedded in everything, and particularly noticed in energy and food prices.

It’s challenging to offer encouragement when global financial markets remain (appear stuck) in downtrends.

- The -20% decline YTD (first 6 months) for S&P500 places it in undesirable company of 1962 (-23.5%) and 1970 (-21%) for the worst starts to a calendar year.

- Since 1950, there were 23 first half (6 months) negative stock market return experiences. Performance in the second half of the year was a toss-up, a little better than a coin toss (for better or worse).

- S&P500 volatility in the first half of 2022 was high with 90% of trading days experiencing moves of greater than 1%, the highest since 2009 (99%).

- The YTD -10.4% bond index decline is atypical; declines for two consecutive quarters are very rare.

- During 186 quarters since 1976, a negative quarterly return for both stocks and bonds occurred just 20 times; there were 5 instances where both stocks and bonds were negative for two consecutive quarters.

- Bonds historically rally in the quarter following 2 negative quarters. Stocks were positive during 3 of the previous 4 instances, while bonds returned positive results in all 4.

- Consecutive negative quarterly performance for stocks and bonds was associated with a recession in 3 of 4 instances. Some economists now place the chance of a recession (2 consecutive quarters of negative GDP growth) at 50%; it all depends on inflation – when it peaks, how sticky it is, and how fast it travels lower. The Russia/Ukraine conflict and repair of supply chain challenges affect inflation fighting efforts.

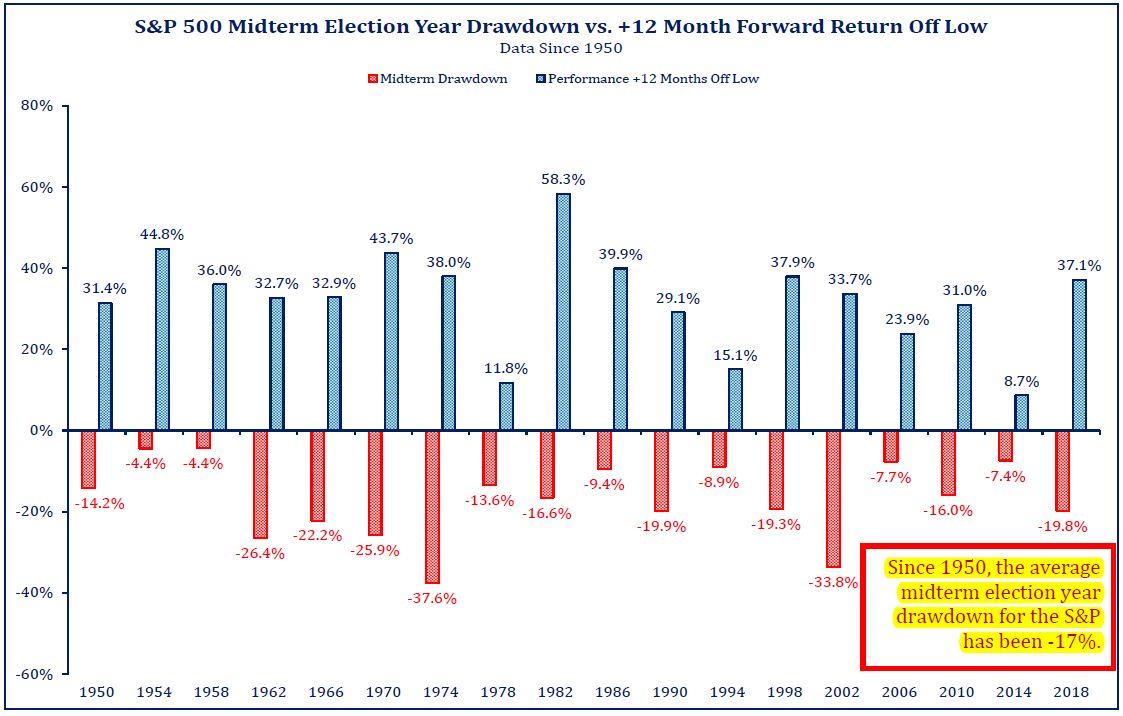

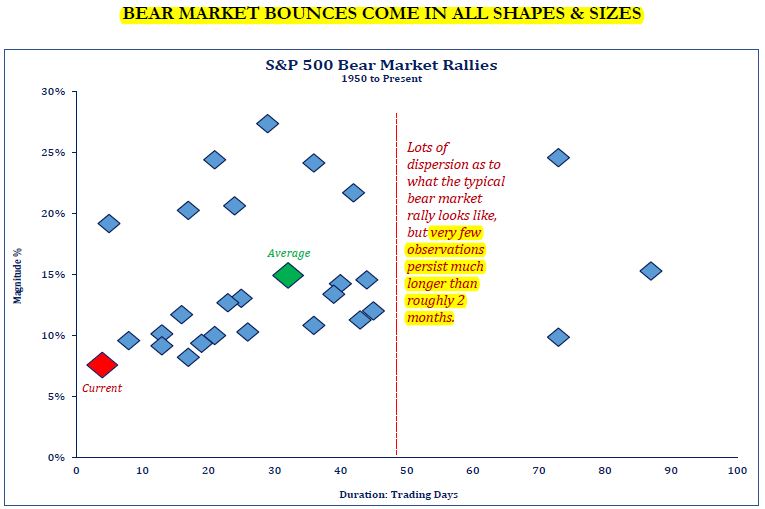

It’s difficult to predict what will happen in the coming quarter(s). It will take time to repair the damage from the current sell off. Investor sentiment is low and the markets appear oversold. A bounce, even several rally attempts are possible. Bear market rallies can occur anytime during downturns, rising an average of +15% in less than 2 months.  Separately, recall that during mid-term election years the stock market experiences a pullback that averages -17%; which could mean much of the pain of this midterm election year is past (see chart at end of this publication). Then, during the next year markets are generally encouragingly higher. One of these rallies will turn into the next bull market. It’s difficult to differentiate between a bounce in a downturn versus the start of something more durable. As there is no crystal ball forecasting the market future, no one can identify which next rally is the one that runs. Market turmoil and rainy days can be challenging for clients; they are exhausting for us as well.

Separately, recall that during mid-term election years the stock market experiences a pullback that averages -17%; which could mean much of the pain of this midterm election year is past (see chart at end of this publication). Then, during the next year markets are generally encouragingly higher. One of these rallies will turn into the next bull market. It’s difficult to differentiate between a bounce in a downturn versus the start of something more durable. As there is no crystal ball forecasting the market future, no one can identify which next rally is the one that runs. Market turmoil and rainy days can be challenging for clients; they are exhausting for us as well.

PS: A study by the University of South Florida indicates that shoppers who drink coffee before pushing the shopping cart spend 50% more money than un-caffeinated. They bought more stuff they didn’t need. Consumer activity accounts for roughly two-thirds of GDP. Caution: drinking coffee before shopping will not help the Fed curb demand, and excess spending will likely not help you achieve your financial goals (Starbucks coffee is a lot higher than a year ago). If you drink it before bed, your sleep may be delayed leading to watching the “bad news media.” I knew there was a good reason not to drink that stuff!

BILLS TO PAY?

World governments created the Great Lockdown of the world’s economy in response to COVID-19. Their response produced overwhelming fiscal and monetary stimulus to minimize a likely recession. Did they realize that the bill for supporting the global economy would come due sooner or later? As of the end of 2Q and the first half of 2022, is the debt paid in full or does a balance remain? Are there still bills to pay?

The Fed and other world central bankers just started to address paying the cost of excess money supply.  Stimulus money accelerated demand; staved off a recession (in 2020); but produced high inflation because supply chains were damaged. Higher prices occur when demand exceeds supply; the greater the demand vs supply, the faster and higher prices rise. Broken supply chains are still being repaired to meet high demand.

Stimulus money accelerated demand; staved off a recession (in 2020); but produced high inflation because supply chains were damaged. Higher prices occur when demand exceeds supply; the greater the demand vs supply, the faster and higher prices rise. Broken supply chains are still being repaired to meet high demand.

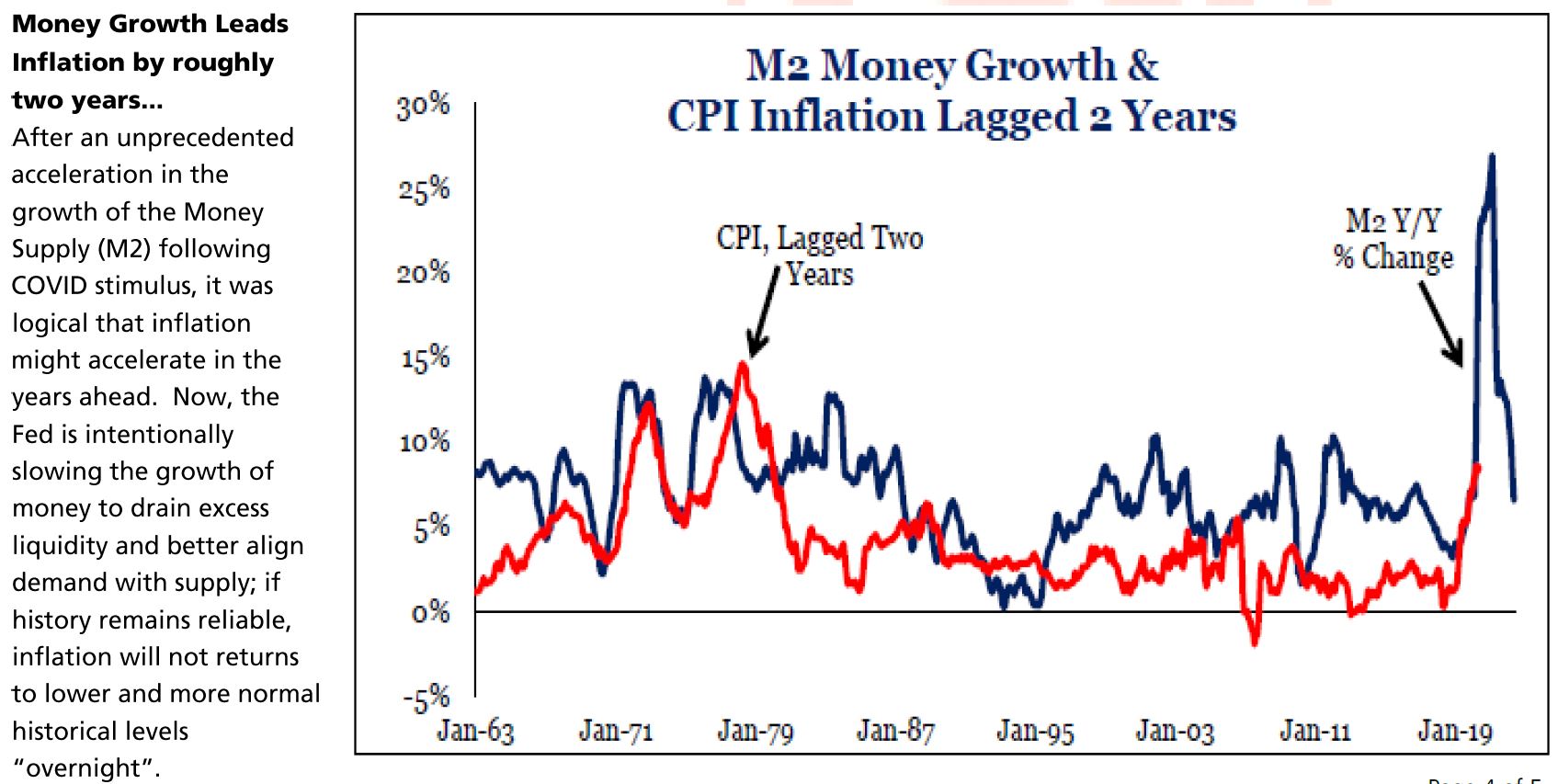

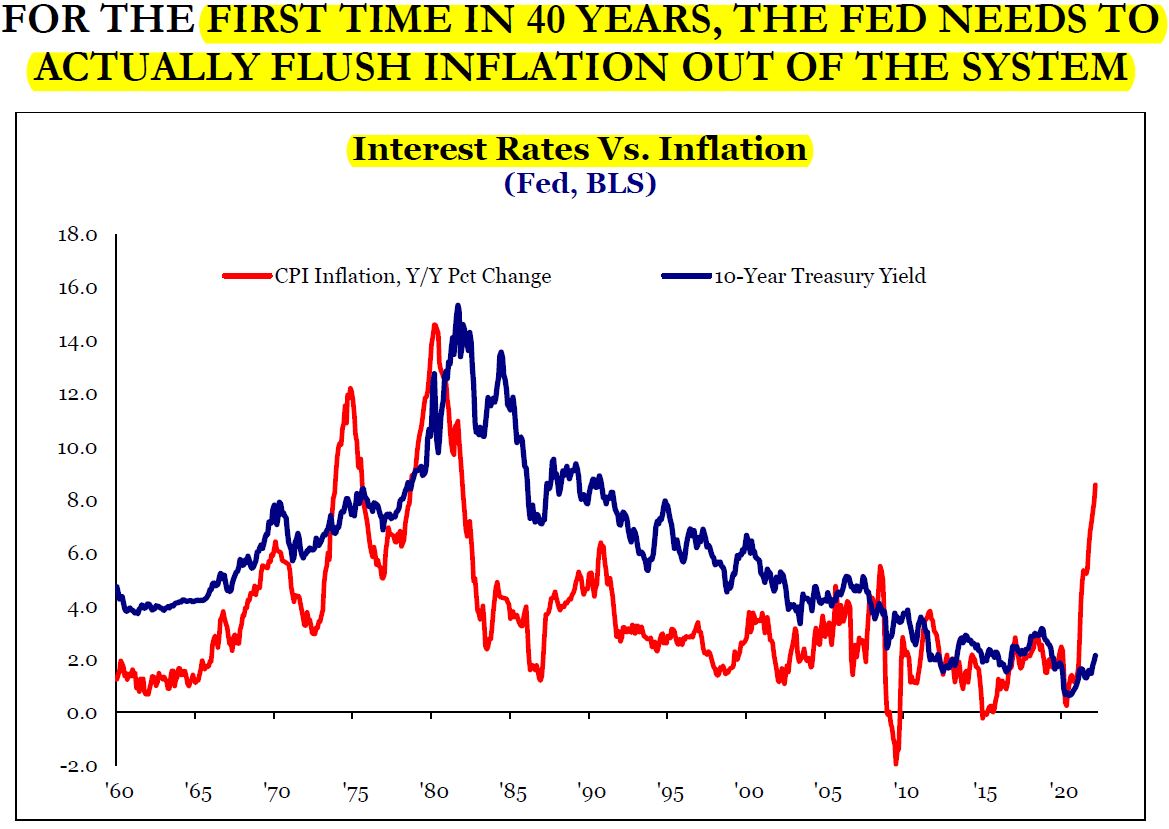

Money supply (M2) peaked at +27% in February 2021 and is approximately +7% at current. Presently, the Fed response is late or reactionary (not progressive). The Fed and others are now attempting aggressive tightening actions – raising rates quickly and by a lot, with the goal of slowing the economy and reducing demand. Over time, these actions will reduce inflation. Unfortunately, monetary policy acts with a lag by 12 to 14 months. [Fiscal policy – like tax cuts or increases, or new regulations generate more immediate impact on economic growth – changing business and consumer actions.] Inflation is influenced by excesses in money supply and other government policy; high inflation and recessions signify government policy mistakes.

The financial markets are watching and reacting. Investors’ reactions are expressed through volatility as valuations are altered. In essence, the markets are “voting” that the debt is still being paid, and will take longer; volatility will likely remain high. There is also the belief that the Fed cannot throw a life-line, or provide a backstop anytime soon to stabilize market worries about a recession; it is determined to aggressively fight inflation. Higher interest rates (not higher taxes or regulations, or new spending) can curb excess demand and sticky inflation over time.

Time is needed to repair the market damage; to establish a market bottom. During this process, investors will see the markets bounce from oversold conditions. Watch credit spreads – as lower quality bond yields widen because they expect higher risk resulting from raising interest rates and slowing economic growth. At the same time, stock market leadership is defensive. Currently, there are some early data points that appear near bear market lows – selling the YTD best performers (good stuff). Also, the financial futures market predicts 5-year inflation expectations are declining, down from 3.2% to 2.5%. That’s 5 years away, but predicting declining inflation. Overall, there is limited evidence that the market is discounting trough data, peak inflation, or a Fed pivot (from tightening) yet. The bear probably will test its low of June 16 when the S&P500 was off -23% and the 10-year Treasury was 3.5% (prices were off -10.4%).

We cannot control the financial markets or even the bear. But, we can control our actions and reactions. Investors are correct in being cautious, but also required to remain watchful. As we navigate the uncertain bear market path, client portfolios should not undergo big or radical alterations; small adjustments can be appropriate. Bond allocations should focus on short and intermediate duration with a quality bias. Bond market yields moved higher and faster than the Fed, meaning much of the Fed’s future action is priced in; savers are earning higher yields. Similarly, stock allocations should remain diversified – a quality bias includes short duration stocks (paying dividends) found in value style choices. Portfolios incorporated an energy ETF (highest dividend yield of any stock sector) and recently a commodity ETF as a diversity hedge against inflation. As the bottoming process plays out, be careful; don’t be tempted to speculate with counter-trend rallies into former leaders or high risk areas. “Dead cat” bounces are usual within bear markets. Bear market rules still apply as the Fed pursues its aggressive tightening policy. Market turmoil ultimately diminishes as the Fed begins to pivot from tightening. Remember that one of the upcoming rallies will ultimately become the start of the next, or new bull market. Investors need to be there before it starts; it’s too late after.

MONEY GROWTH LEADS INFLATION