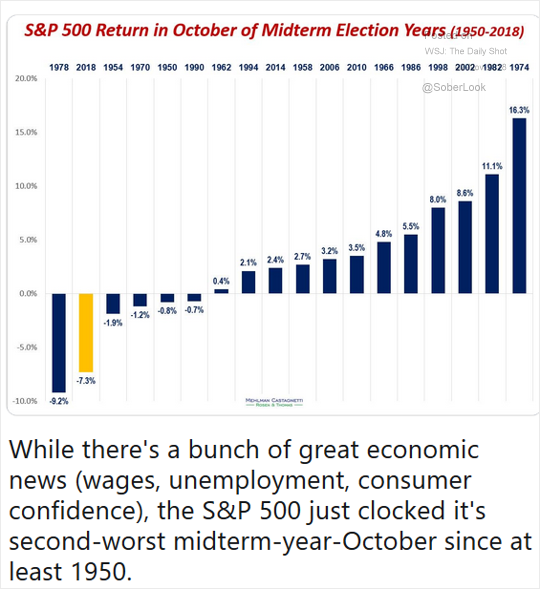

Shake or bake; not! Shake and/or Break is a fitting title for the frightful market action in October. Markets may “shake” because of tariffs. But, the Fed can cause the market “break.”

Much of the blame for October is aimed at President Trump and/or Federal Reserve Chairman Powell. Investors are concerned that the Fed remains inclined to raise interest rates further – 1 more hike in December, and presently communicates 3 additional times in 2019. There are even forecasts of one more rate increase planned in 2020. Investors are also concerned about tariffs because they are like a tax to American citizens. Both issues are viewed as punitive to economic growth over the next 12 months. Some wonder if the recent economic strength is “as good as it gets.” That suggests that economic and business growth will be shifting into slow expansion again (even though this expansion will become the longest running in US history next year). The economy is probably able to handle slow rising interest rates, to a point. But the stock market will show stress earlier, as witnessed by action in October. In essence, the market tone was altered due to these two concerns. Again, markets may “shake” because of tariffs; but markets could “break” because of the Fed.

As relentless as it was, we believe the October stock market action was a temporary selloff and not the start of a bear market. Sudden stock market selloffs caught investors twice in October. The S&P500 dropped -6.9% during the month, and was off -9.8% on October 29th from its September 20 peak. Small company stocks declined -13.2% during the month, and foreign stocks lost -8.6%. FAANG (Facebook, Amazon, Apple, Netflix, and Google) and technology stocks were especially hit hard, as their prices were bid high during the market advance of the last 2 years. In corrections, the best sectors/stocks are generally the last to get hit. In general, action during the month erased almost all the market gain for 2018. Price volatility added to investor worry, as volatile price action was not present for most of the year since January. Diversification in client portfolios did not help much as even bond investments posted negative returns due to rising interest rates.

As relentless as it was, we believe the October stock market action was a temporary selloff and not the start of a bear market. Sudden stock market selloffs caught investors twice in October. The S&P500 dropped -6.9% during the month, and was off -9.8% on October 29th from its September 20 peak. Small company stocks declined -13.2% during the month, and foreign stocks lost -8.6%. FAANG (Facebook, Amazon, Apple, Netflix, and Google) and technology stocks were especially hit hard, as their prices were bid high during the market advance of the last 2 years. In corrections, the best sectors/stocks are generally the last to get hit. In general, action during the month erased almost all the market gain for 2018. Price volatility added to investor worry, as volatile price action was not present for most of the year since January. Diversification in client portfolios did not help much as even bond investments posted negative returns due to rising interest rates.

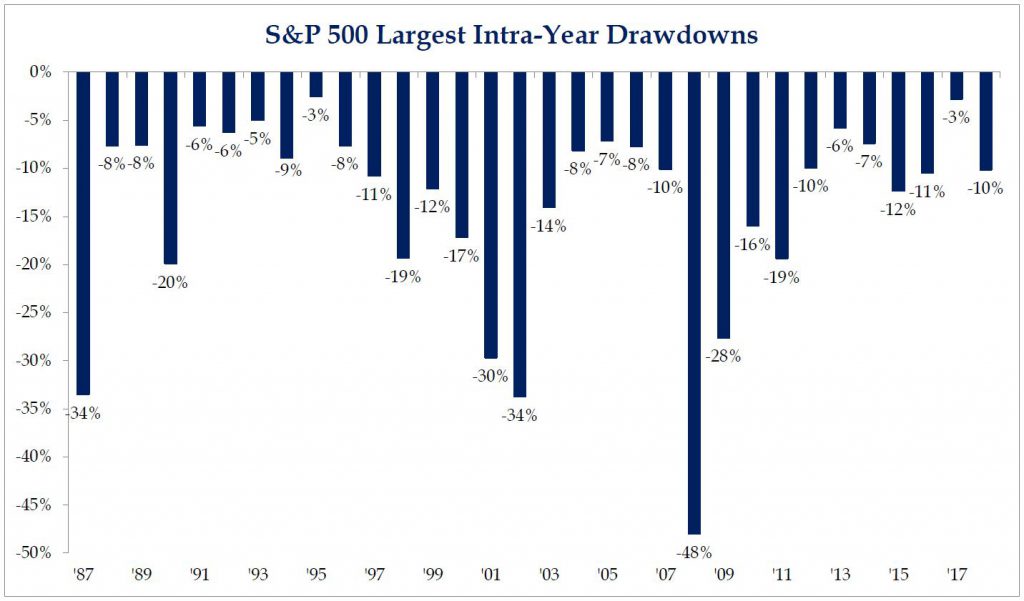

Sharp initial drops are often hallmarks of ordinary corrections, defined as a price decline between -10% and -20%. A -10% pull-back is not out of the ordinary (see chart to left). Corrections do not always, or often, develop into bear markets. Looking at 22 corrections since 1974, there were only 4 that evolved into a bear market (1980, 1987, 2000, and 2007). In the current Bull Market since 2009, there were 6 corrections that did not become a bear. Bear markets typically start with deceptively gentle drops, and are often triggered by a recession. When a bear market does come, it will most likely commence with a whimper, not a roar. Since 1966, the average bear market lasted just shy of 17 months, far shorter than the average bull market (60 months). Bear markets often end abruptly, the opposite of how they begin, with the rebound being extremely robust and difficult to predict. An almost opposite market experience occurs with a correction – the drop starting abruptly, and a recovery thereafter occurs slowly. Since timing is so difficult, it is wise to invest for the long-haul; stay the course.

Sharp initial drops are often hallmarks of ordinary corrections, defined as a price decline between -10% and -20%. A -10% pull-back is not out of the ordinary (see chart to left). Corrections do not always, or often, develop into bear markets. Looking at 22 corrections since 1974, there were only 4 that evolved into a bear market (1980, 1987, 2000, and 2007). In the current Bull Market since 2009, there were 6 corrections that did not become a bear. Bear markets typically start with deceptively gentle drops, and are often triggered by a recession. When a bear market does come, it will most likely commence with a whimper, not a roar. Since 1966, the average bear market lasted just shy of 17 months, far shorter than the average bull market (60 months). Bear markets often end abruptly, the opposite of how they begin, with the rebound being extremely robust and difficult to predict. An almost opposite market experience occurs with a correction – the drop starting abruptly, and a recovery thereafter occurs slowly. Since timing is so difficult, it is wise to invest for the long-haul; stay the course.

The October 2018 violence may counter-intuitively be good news for the markets in the future. On average, stock market recovery follows within 6 months, and a rally resumes within a year. Time, price and sentiment are all important factors that must work through prior to the resumption of a rally and a Bull market. Recent negative price action is probably close to being completed. Investor attitude (sentiment) takes time. Following the October price drop, stock market valuations today are lower than those at the time of the November 2016 presidential election.

Other good news from history indicates that a recession – usually a catalyst for a bear market – never started when real (after inflation) Fed Funds was near zero, as is currently. In other words, short interest rates need to be a lot higher above the inflation rate to cause the economy to slide into a recession. This trait merits watching, because the Fed is moving along a path that will take short interest rates higher. If they move too much, too fast above inflation, then problems can occur. The economy still has time because it can manage somewhat higher interest rates. But Fed action could make the markets break.

Economic and market action of the last couple of years was so good, that it is natural for investors to think it cannot get any better. US economic growth in 2Q was +4.2% and the 3Q was +3.5% on first report. Those stats spell solid US growth, much faster than over the prior 9 years of this recovery. Yet, early 1Q2019 economic growth estimates are +2.5%, and further slowing to +2.3% by 3Q2019. The Fed’s own forecast expects growth to slow to +1.8% in 2019. A slowdown in the rate of economic growth has implications for stocks. These forecasts, including the Fed’s, leads one to wonder why the Fed needs to be in a hurry to raise interest rates? Two possible answers: the Fed wants to have a higher end-point for interest rates in its tool box so they have ample room to lower rates if/when a recession were to occur. And, the Fed is also monitoring inflation, which is starting to rise due to full employment and ushering in rising wages. It’s difficult to believe there is enough inflation (at 2%) to hurt the US economy. Nevertheless, rising interest rates pose an immediate worry for stocks and bonds.

Did you know? Rising interest rates are likely changing the “everybody gets a trophy” cost of capital environment created by low or zero-interest rate policy, and alter the investment playing field. Financial repression allowed companies with both weak and strong operating results to get cheap funding; bankruptcies dwindled, and “zombie” entities lived. In 1973, only 9% of bond credits were rated BBB. Today, that figure stands at just under 45%. With higher interest rates will come more pain, and more opportunity. How is that? Higher interest rates will negatively impact highly leveraged (debt) business. Higher interest rates paid on large amounts of debt will eat away cash flow from product sales, and cause some to businesses to fail (recently Sears). That suggests passive investment strategies (“own it all” including the highly leveraged businesses) may not perform well. Conversely, active investment strategies that utilize financial quality factors to build portfolios will own companies with strong financial characteristics, and exclude companies with eroding financial prospects. Performance rewards should accrue to many active managed strategies with strong investment processes and disciplines.

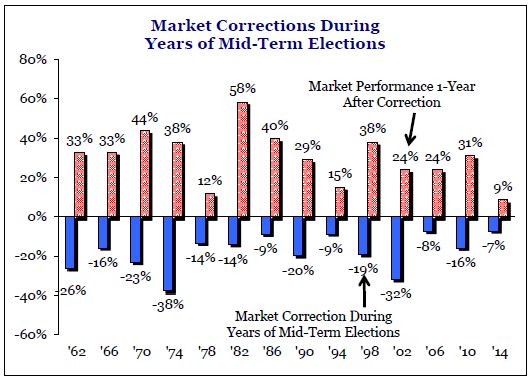

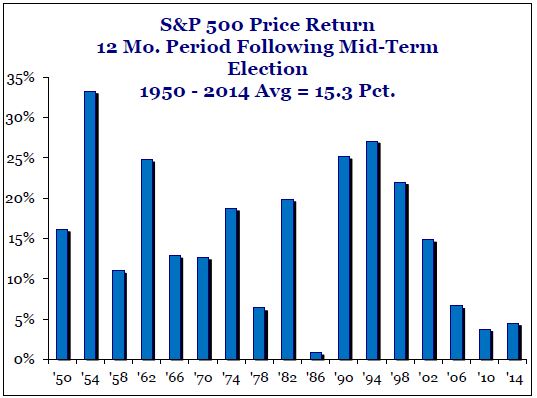

The mid-term elections are now. Most will be thrilled when the media concludes the barrage of political advertisements. Recall, a couple of our previous commentaries shared about the stock market path during mid-term election years. The message was that since 1950, the markets did not perform well in the months leading up to the mid-term election (average correction was -12%); but performance was back-end loaded with the final months making the year. Another recent study, back to WWII is very interesting to share. In ALL mid-term election years, 18 out of 18 since WWII, the stock market rose from its October low just over +10% on average during the final months of the year (and +15% after 12 months – see charts below). And, it did not matter who won. In the past, once mid-terms are over, seasonal factors took over as political uncertainty was removed. One must wonder if the recent volatility and damage surrounding “shake” and/or “break” worries will allow for a “surprise” year-end rally to occur as we wrap 2018? Long term investors will however, welcome some recovery of portfolio values before year-end. We expect the US economy can handle somewhat higher interest rates, and we are optimistic that the financial markets will continue the current Bull market advance.

Author: Bill Henderly, CFA – November 6, 2018

Printer-Friendly PDF can be downloaded here: “Shake or Break”

Charts for Reference: