Two months and so far, a very Happy New Year!!! February added +3.2% to a very strong January, making this a great start to 2019 for investors with the stock market jumping a cumulative +11.5%. Wow!! We appreciate the Fed again communicating economic data dependency rather than an autopilot path of raising interest rates, plus tariff talk between the US and China is showing promise of moving toward a resolution. These items are propelling markets higher.

Needing additional investment encouragement? Strong performance in first two months of a new year is historically consistent with above average returns for the balance of the year (25 of 27 observations were positive since 1950). But please don’t annualize two months. If you do, that would equate to a “sprinting” +70% return for the year. No way. The stock market cannot keep advancing that fast, plus it would cause valuations to be extremely “irrationally exuberant”. Still, history reveals that the average 3/1 to 12/31 return following strong-start years such as this was +12%. Together, they accumulate to an attractive full year return. Also important, during the remainder of those strong years the market did experience an average -9% pull back. After the fast 2019 start, a pullback and/or pause would appear appropriate.

As we shared in our commentary last month, it is historically rare for stocks to bounce back in a “V” pattern following such a damaging earlier quarter. Most often, recoveries take the form of a “W” – down, up, then down again to retest the low-area before moving back up to prior highs and onward. And for new highs to be achieved requires underlying economic fundamentals to provide support. Recoveries usually do not occur in weeks; more often they take months and on average the better part of a year to repair significant damage.

Client portfolios advanced nicely in February and YTD – and diversification provided attractive benefits to managing risk without eroding returns.

Recent stock market action overlaid on top of Kevin Kallaugher’s famous cartoon.

It appears markets are more calm since December; that’s welcome following 2018 where the markets struggled to find more than temporary happiness in anything. If economic data was poor, the thought was “Oh my, we’re heading for a recession;” or if the results were strong, then the prevailing thought was “Oh my, the Fed will be hiking interest rates again!” In essence, last year investors’ “psychological wiring was on fire.” Now, the stock market start to 2019 suggests the “world” of investing is good with investor sentiment much improved [see graphic above]. Strong, early year returns now cause markets to appear fairly or full valued – which poses some near-term concern from our perspective.

What could cause a pause or pullback in the short-term? With the stock market appearing fair or fully valued again, three things must continue to progress well. This creates a “thread the needle” idea. Given full employment, wage rates need to increase slowly or stay low; rising too fast will boost inflation expectations and the Fed might be inclined to resume rate hikes. Second, trade tariffs already levied need to be reduced (no new tariffs). And third, the Fed needs to pause (not raise interest rates because of rising wage rates boosting inflation expectations) because economic data supports that action. The full-value market is saying, “show me” – it needs visibility of faster company growth to move higher.

There is also an old investment adage – “buy on the rumor and sell on the news.” In the short-term, the market already “bought” (priced in) the resolution of tariff issues with China. If that is as good as it gets, the market may sell off on the news event. If the tariff resolution includes rollback or reduction of current tariffs, that equals new good news (not in current market prices).

Economic fundamentals support current valuations. Investors understand the US economy was the standout against a backdrop of slowing global activity in 2018, and is likely joining the slowdown in early 2019. But the chance of entering a recession this year remains low probability; it is not a logical call. The US labor market is healthy and consumer sentiment is strong; both are the envy of the world. Also, current real (after inflation) interest rates are +0.25%, a far distance from real rates of +2.0% (above inflation) that exist at the start of most recessions; this is a positive backdrop. The “show me” attitude is understandable from another perspective. With 2018 company earnings being very strong (benefiting from tax reform at YE2017), year-over-year comparisons in 2019 will naturally be slower. “Show me” means other factors (tariffs, interest/inflation rates, and growth) need to go right and thereby provide a boost to growth.

Foreign economies, on the other hand, are softer than the US. More likely, as tariff issues resolve and foreign governments institute other fiscal stimulative policies (tax cuts to copy the US, or spending), their year-over-year comparisons could provide attractive upside opportunity. Plus, if fair value for any market is 1.0, the US stock market is more expensive at 1.3, while the foreign market offers a more attractive value between 0.8 and 0.9.

Investors appreciate the early fast start to 2019, especially with the historical understanding about how the ensuing months of the year often complete. But we are careful about investing in this environment – preferring to de-risk tactical exposures in client portfolios by emphasizing more attractive valuation market areas than stretching into expensive styles/areas. There’s a concept, called “stock crowding” that is applicable today. Stock crowding is the risk of “everyone” (or many) buying the same thing. It’s a propensity to “everyone” owning the same stocks or owning the Index 500 and it’s that concentration that poses risk of unwinding. Too much money chasing the same stocks or indexes, can create much worse drawdown experiences. Momentum feeds on itself, both up and down with down action being more quick and adverse. Currently, the crowded trade is at its highest level in 2 years. Nevertheless, we want to be invested in this market, but through ownership of a diversified portfolio focused on better valuation (lower risk) opportunities; this is investing with care and caution. We strive for long-term investing that generates compounded success.

Rule 1: no one knows with certainty what’s going to happen next.

Rule 2: pay attention to valuations on investments owned or being considered.

Rule 3: keep a long term perspective.

Q: What would portfolio values look like if one sold their portfolio to cash on 12/24/2018?

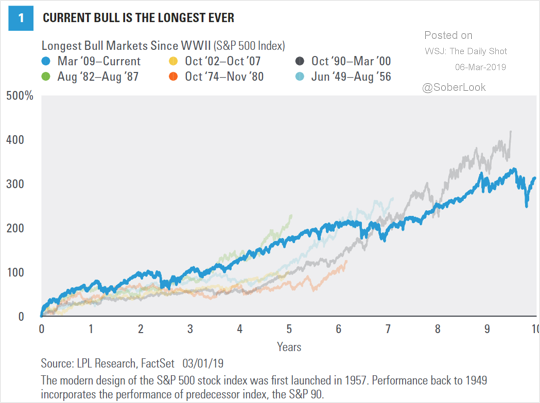

Did you know? The current Bull Market turns 10 years old on March 9th, making it the longest running in US stock market history!!! Happy Birthday (happy new year – see chart below)!