Market participants appear to believe inflation is back and will be sticking around. That’s affecting how investors perceive the outlook and direction for the bond and stock market. As such, this may be the first time since 1990 that diversification benefits achieved by mixing bonds and stocks together are changing. Since late January, both stocks and bonds are caught in the crosscurrents of increased negative activity in Washington DC, namely tariffs and possible trade wars. Add tax reform and fiscal spending which are boosting the prospects of rising federal deficits. The markets are also aware 2018 is a mid-term election year, wherein the composition of Congress could change. On the opposite side, still low but slowly normalizing interest rates, plus low inflation, plus a lot of money (liquidity) in the financial system, plus high confidence by consumers and businesses, all combine to provide a support backdrop for the economy and financial markets.

Three months have passed since the market made its last new high on January 26th. During this time, price volatility in the financial markets is compressing valuations and moving the current correction forward (corrections are composed of price + time + sentiment). The results of recent price-adjustment action are a slowing of the pace of investment returns while raising investor concerns. The correction process is never comfortable and creates struggle for investors following nearly 2 years of slow, steady rising returns with virtually no price volatility. It appears the market tone is now changed.

Stock returns were virtually flat in April, while bond returns were slightly negative as the 10-year Treasury yield rose toward 3% (up from 2.4% at year-end). With global synchronization still present, even foreign investment exposure could not provide much boost to portfolio returns. Client portfolios with greater stock market exposure performed marginally better than those with heavier bond exposures.

For as challenging as the heightened volatility seems, under the stock market surface there are signs that the intensity of the correction is abating and stocks may be trying to forge and solidify the lows for the year, occurring on February 11th. Investor sentiment is also shifting as bears are increasing in number and bulls are waning. But each punch thrown (like tariff concerns, trade war, Fed action, or a fear of growth slowing down), the blow appears to be more glancing. It may not feel like it, but April returns offer that perspective – the intensity of the correction may be abating.

This month, let’s focus the balance of this commentary on the bond market – interest rates and the tone change affecting all of financial markets. We don’t often write much on bonds or their market influence; but it is appropriate to review the shift in capital policy, because it is arguably the most acute adjustment stocks are wrestling with.

We are entering a new environment that is likely characterized by a return of inflation, an increase in volatility, and uncertainty about the US dollar. Portfolio strategy and management of bond allocations will evolve because of a secular change that is just beginning. This is important, because changes in the bond environment often influence stock and financial markets.

First, let’s understand a quick perspective about “good” and “bad” inflation. Generally, we talk to investment clients that all inflation is one of two enemies we battle; the other being taxes. Investors need to invest to “beat” the effects of inflation and taxes. Yet most economists believe some inflation is “good” when an economy is slow performing; low, but positive levels of inflation boost consumers’ desire to “buy now” at current rather than higher prices anticipated in the future. “Good” inflation boosts economic growth and allows borrowers to repay debt with slightly cheaper dollars over time. “Bad” inflation (even deflation) arises from government policy that moves prices of goods and services but not in any relation to economic supply and demand. One example of “bad” inflation occurs from import prices and input costs being altered by tariffs and/or taxes. Currently, the magnitude of inflation

is not enough to be worried about, by itself. Tariffs and trade wars could alter this environment and create stagflation, a condition of low growth accompanied by inflation.

Following 10 years of monetary stimulus characterized by low interest rates and quantitative bond buying activity instituted to address the financial crisis of 2007 and related slow economic growth environment, these policy actions promoted a “risk-on” investment strategy. For bonds, many investors reached for yield via long maturity and lower credit securities; for stocks it meant owning everything (passive indexes). Monetary policy, which was super accommodative, is now normalizing. And, there is a corresponding shift back to fiscal policy. When government and politics enter the picture, volatility rises. Now, issues of FANG (Facebook, Amazon, Netflix, Google) stocks with possible government regulation, and tariffs, etc. mean the investment environment is changing – that means a possible shift in capital flows. Bonds are at the front of this equation – after 35+ years of a secular bull market for bonds, we are moving to a secular rise in interest rates. Rising rates mean bond prices fall, termed a bear market for bonds. There is currently a passing of the baton to fiscal policy (tax reform, repatriation of foreign earnings, spending on infrastructure, and regulation relief). Increased government deficits can create “crowding out” worries as interest rates rise. Thus, fiscal policy represents the biggest, most important domestic/global economic influence for global markets. It is notoriously long and variable in its effects.

Higher interest rates, resulting from Fed normalization of its rate policy, plus rising inflation (“good” or “bad”), with a stronger economy and increasing debt levels leads to future pressures on bond investing. In the very short term, investors will wrestle if/when higher rates will slow or even stall the economy, and slow company revenues/earnings. Remember, earnings are the backdrop of support for the stock market advance. Some may be wondering if the current moment may be “as good as it gets?”

One sign or closely watched indicator is the interest rate “yield curve.” Investors watch the shape of the curve to provide signal for the future of bonds and the stock market. Bull markets end when yield curves invert (condition of short term interest rates moving higher than long rates); and/or when high yield (low quality) bond yields rise quickly. Neither of these traits exists today. The yield curve is flattening – the spread between the 10-year and 2-year Treasury was recently +0.5% (compared to +2.65% wide in 2013), but remains positive sloping. An inverted yield curve suggests investors believe the Fed will raise interest rates too far, to a point that the economy risks faltering.

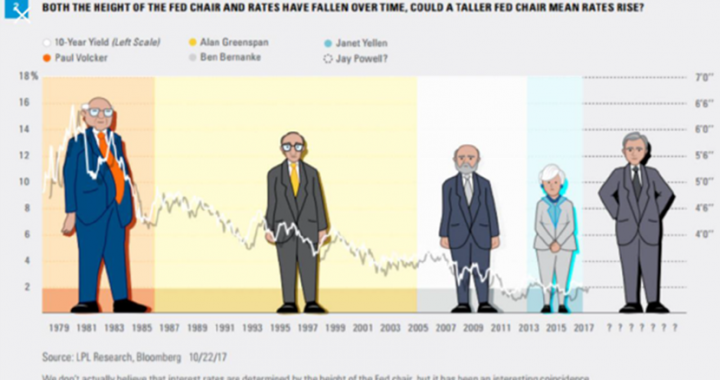

We offer two interesting charts for quick review. The first shows a long time perspective of interest rates – from 1945 to 2017; the first half of the chart, from 1945 to 1981 reflects a secular rise of interest rates, and from 1981 to recent shows a secular decline. The recent 35+ year bull market for bonds, with yields declining to lows, may be ending as the Fed is now normalizing interest rate policy. The second humorous chart displays interest rates falling since 1981 as the height of the Fed chair was getting shorter; now the new Fed Chair Powell will be the tallest Fed chair in recent history. Does that provide further signal of a change in the secular direction for interest rates (this observed correlation is only shared comically of course)?

What does the bond “tone change” mean for investors? Be wary of reaching for yield. Stay maturity short and particularly mindful of bond issuer credit quality. A steepening yield curve can wipe out interest return as the price of bonds fall, particularly more dramatically for longer maturities. Be keenly aware of how much risk is embedded in some bond mutual fund portfolios. In other words, bond product integrity will be important. As some bond fund managers (who reached for yield) unwind risk, their actions could increase bond market price volatility. This could be emotionally unsettling for investors pursuing risk-avoidance via owning bonds. Lastly, bond investors should lengthen their time horizon (not lengthen their maturity focus), by reducing the need to churn. Bond investors are many years removed from past troubling times for bonds, where bond investing was almost boring. A tone change is early in its beginning, and the temptation is to believe things will not change quickly. A rise of interest rates to normal won’t be quick (unless the market gets too worried over politics); the change won’t be a straight line upward. But, we do believe yields are reversing a 35+ year secular bull market trend of declining, and bond portfolio construction is important now, not if/after things get tough.