Beyond the Headlines | Steve Henderly, CFA

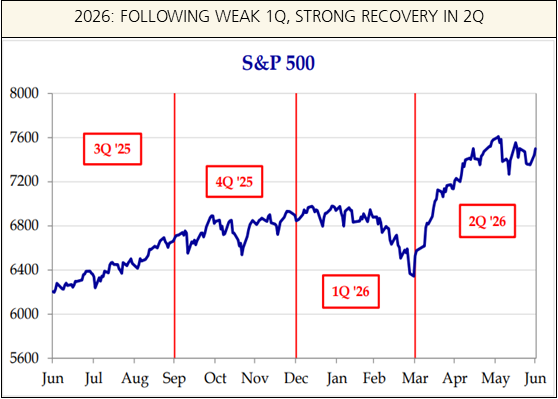

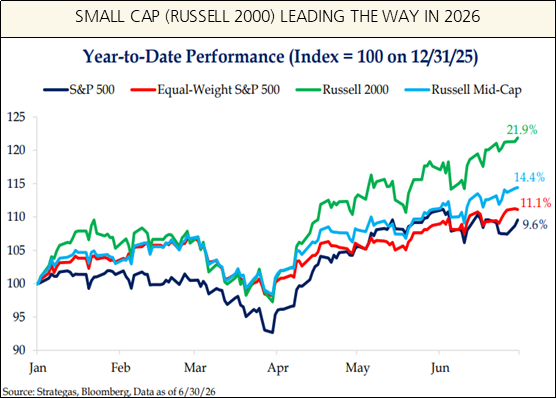

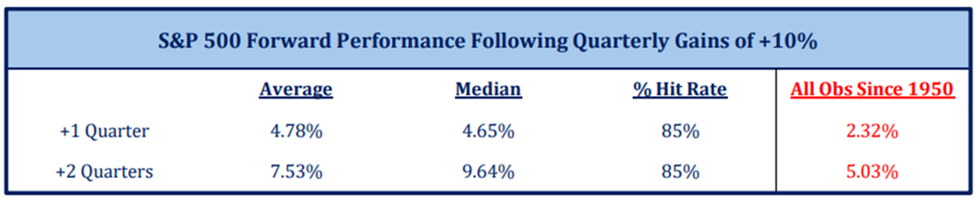

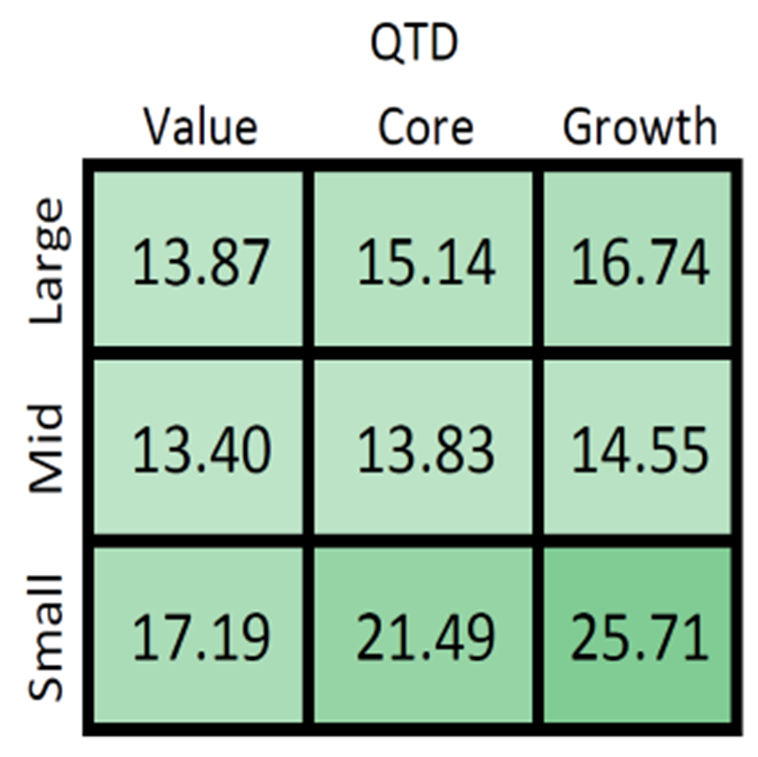

“Don’t judge a book by its cover” might be an appropriate phrase for investment results of the 2nd quarter. Headlines remained scary entering April as the Iran war was not resolved and oil prices continued to swell through mid-May. Inflation concerns, shifting expectations for Federal Reserve policy (rates), and questions surrounding artificial intelligence spending seemed like a recipe for a difficult investing experience. In spite of this scary backdrop, the S&P 500 rebounded from its March drawdown, enjoyed a nine-week winning streak, and logged 21 new all-time highs in April and May. It was the strongest quarter for the S&P 500 in six years, and sixth best since 1950. Even more surprising, the Russell 2000 (small companies) was up 22% YTD, the best performance since 1991!

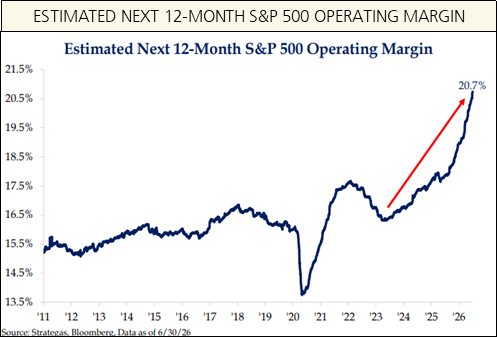

The rally was not without fundamental support. Earnings for the 500 largest U.S. companies surged nearly 30% from the same period a year earlier, giving rise to the term FEMO (“Fabulous Earnings MOmentum”). From a macroeconomic perspective, economic data also remained resilient. Together, these factors provided a solid fundamental foundation for the market’s advance, rather than an emotional-driven case of FOMO (Fear Of Missing Out).

Then arrived what some are calling a “June Swoon.” Technology stocks, particularly many of the market’s biggest winners over the past two years, struggled. Headlines surrounding artificial intelligence spending, bond yields, a new Federal Reserve Chair with a decidedly hawkish tone, and uncertainty surrounding the conflict with Iran were cited. The technology sector, which comprises nearly 40% of the S&P 500 market cap, struggled. Conversely, the average stock quietly held its ground. Market breadth actually improved in June as money rotated into financials, healthcare, industrials, and other sectors lagging since March. In fact, the equal weight S&P 500 was up 2.4% in June vs the traditional market weight index which was down 1.0%. Rather than abandoning equities altogether, investors appear to be reallocating/rotating toward areas with more attractive valuations and improving fundamentals.

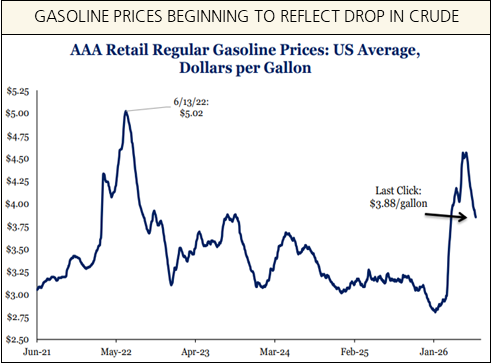

The type of rotation and broadening observed in June is often a hallmark of healthier bull markets. Sustainable advances are typically driven by more than just a handful of companies doing well as confidence spreads throughout the economy. As tensions with Iran eased and shipping through the Strait of Hormuz reopened, oil prices retreated sharply from their highs. While not back to pre-war levels, lower energy prices provide both relief at the gas pump and ease inflationary pressures that were quickly building throughout the economy. That should reduce some of the pressure for the Federal Reserve to tighten (raise rates).

Meanwhile, businesses continued investing aggressively in technology, infrastructure, and productivity-enhancing capital projects. This economic expansion continues to appear driven by corporate investment rather than consumer borrowing – a dynamic that is proving to make the economy resilient despite higher interest rates.

Markets will always experience periods of volatility, and June reminded us that not all selloffs are created equal. Sometimes the most important story isn’t what the indexes are doing – it’s what’s happening underneath them. Look beyond the headlines! In the 2Q, the underlying picture became healthier even as the headlines suggested otherwise.

Outlook: The Fed’s New Playbook

As highlighted in our 2Q recap above, the investing backdrop can change remarkably fast. And the year continues to be a tug of war between inflation and productivity. The two biggest questions still facing investors as we turn our eyes to the 2nd half of the year is whether the Fed will tighten by the end of this year and if capital expenditures/investment in artificial intelligence will continue at such a torrid pace.

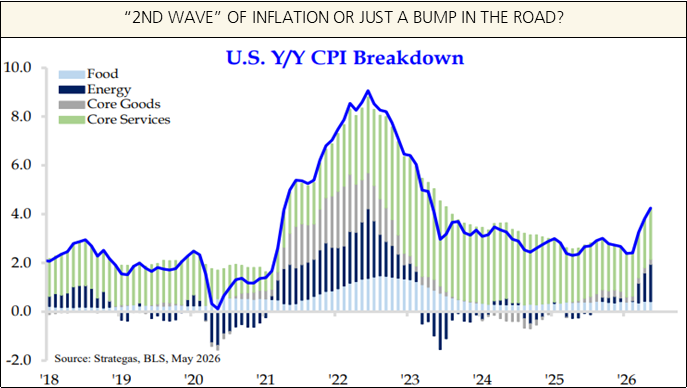

Entering the year, markets expected the Federal Reserve to continue easing monetary policy via additional interest-rate cuts. Instead, a resilient labor market, elevated energy prices, and persistent inflation pressures forced investors to seriously rethink that outlook during the 2Q. By early June, markets went from expecting meaningful rate cuts to expecting that the Fed’s next move will be a rate hike (or several). That is an extraordinary shift in expectations over such a short period of time.

The arrival of new Federal Reserve Chair Kevin Warsh only reinforced the message. While many investors hoped his leadership would usher in a faster pace of rate cuts, his early communications emphasized continuity rather than change. Restoring inflation to the Fed’s 2% objective remains the central focus, suggesting the Fed is unwilling to declare victory prematurely.

The hawkish outlook has softened in recent weeks. Easing of tensions in the Middle East and corresponding sharp decline in oil prices remove one of the largest inflation risks that emerged during the quarter. Lower energy prices should gradually work their way into gasoline prices, transportation costs, and broader inflation readings. That doesn’t justify rate cuts, but it may reduce the likelihood that the Fed needs to tighten policy further.

We believe the Fed remains more hesitant than the market consensus to raise rates. Rather than cutting rates – or potentially raising them – the Fed can remain on hold while evaluating whether productivity gains from unprecedented business investment can offset lingering inflationary pressures. That’s the tug-of-war we continue to watch most closely.

If productivity wins, corporate earnings can continue growing despite a higher interest rate environment and provide fundamental support to today’s market valuations. However, if inflation proves stubborn, higher interest rates could remain a headwind for both stocks and bonds longer than many investors anticipate. A new source of inflationary pressure appears to be emerging and must be monitored. The huge demand for semiconductors and digital storage is prompting some significant increases in the price of consumer electronics (like smartphones, computers, and more) and electricity.

The good news is that markets often adapt quickly. Corporate earnings remain healthy, credit markets are functioning well, and market participation has broadened. None of these factors guarantee smooth sailing, but they do suggest the economy remains on solid footing despite a considerably different interest-rate landscape than most investors envisioned just six months ago.

Market performance in 3Q and potentially into the November midterm election will be greatly influenced by inflation trends from here. Midterm elections historically create additional volatility, not that it’s been lacking to this point. Summer is also a time when the market often stalls and can react in outsize ways as trading volume tends to be lighter. Regardless, we will spend less time trying to predict the timing of the Fed’s next move and more time evaluating how changing monetary policy affects long-term opportunities across asset classes. From our perspective, the backdrop of huge business investment remains strongly intact and thus the economic outlook remains expansionary. Successful investors are wise to continue to look through short-term noise and focus on the big picture.

After the Launch: Don’t Let FOMO Take the Controls

Human beings are psychologically wired to follow the crowd. In everyday life, instincts are often beneficial. If everyone suddenly starts running in one direction, there is usually a good reason.

Markets operate differently. The greatest investment opportunities often begin when very few people believe in them. And, the greatest risks usually emerge after the “launch” and everyone agrees something is a “can’t miss” investment theme. Fear Of Missing Out (FOMO) takes hold. History is ripe with examples. Railroad stocks in the 1800s. The South Sea Bubble. The “Nifty Fifty” during the early 1970s. Internet stocks in the late 1990s or housing in the mid-2000s. In nearly every case, the underlying innovation or investment theme was real – but investor enthusiasm ultimately outran fundamentals. In essence, investors “jumped on board the momentum train” believing recent rapid price rises (like a Rocketship liftoff) would continue. That’s FOMO!

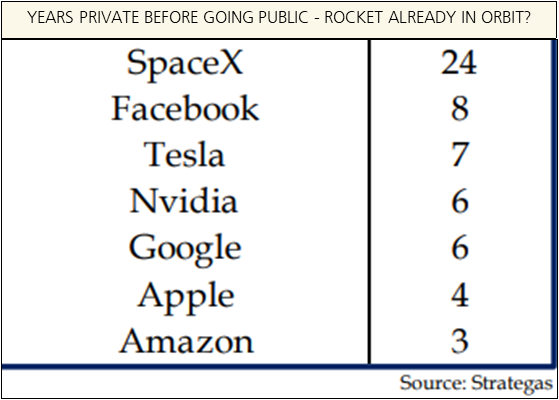

One of the more interesting market traits today is how quickly investor enthusiasm seems to migrate from one area of the market to another. Consider Bitcoin. Nine months ago, when it was soaring toward $130,000 per coin, many investors were eager to gain exposure for fear of missing out. Today, with Bitcoin trading closer to $60,000, much of that enthusiasm is gone. Gold tells a similar story. Just a few months ago, investors rushed to buy above $5,300 per ounce, seeking protection from inflation and fiscal uncertainty. After suffering its worst quarter in 13 years, however, interest has faded as prices approach $4,000 per ounce. Today’s excitement is semiconductors, artificial intelligence, and the companies building the infrastructure to support it. The enormous demand for shares of SpaceX, the largest IPO in history, is the latest example.

None of these themes are inherently bad (some arguably more speculative than others) and may still prove to be exceptional long-term opportunities. The challenge is that when everyone reaches the same conclusion at the same time, valuations get detached from even optimistic fundamentals. “Safe” investments quickly become anything but safe. History reminds us that wonderful companies don’t always make wonderful investments. Good companies can be bad investments if purchased at the wrong price.

As investors, our goal isn’t to avoid innovation. We should strive to avoid becoming overdependent or overexposed to any single idea, no matter how compelling the narrative may seem. We want exposure to the technologies and trends shaping tomorrow’s economy, but we must also recognize that market leadership changes, investor sentiment shifts, and today’s market darling can quickly become tomorrow’s disappointment. Markets, and humans, will always latch onto a favorite story. Successful long-term investors participate in those stories – but rarely allow any one theme to dominate the entire plot.

As we celebrate our nation’s 250th birthday, it’s an appropriate time to reflect on one of history’s greatest long-term investments – the American economy. Every generation of investor will inevitably live through wars, panics, bubbles, political turmoil, and countless “this time is different” moments. The lesson isn’t that markets never stumble – they certainly do – but that discipline, diversification, and patience consistently outperform fear, euphoria, and attempts to outguess the future. Successful long-term investing requires diversification, not being “in love” or “married” to one market area. Risk management and valuation are important.