Mixed Signals in a Market at New Highs | Steve Henderly, CFA

Printer Friendly PDF: June 2026 Commentary

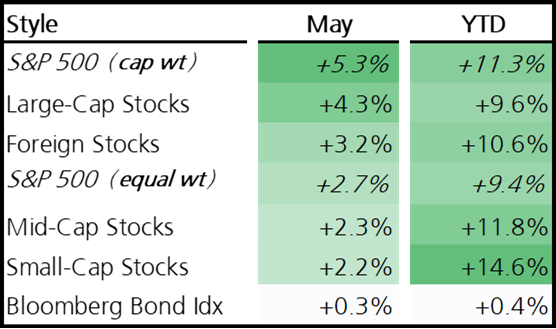

Whether red hot or ice cold, ever notice how the stock market rarely feels comfortable? Sometimes it falls sharply with little warning. Other times it climbs relentlessly despite numerous worrisome headlines. The S&P 500 added eleven new record highs in May. The market hit a low on March 30 following the Iran War and Strait of Hormuz closure. In the 42 trading days since this most recent low, the S&P 500 index advanced 18%! That places the rebound among the strongest short-term rallies since 1950. Yet consumer confidence is sitting at/near the lowest levels ever recorded due to a war that is not resolved, elevated oil prices, and rising interest rates due to building inflationary pressures. How can both be true? How can investors celebrate while consumers are deeply concerned? Two questions keep surfacing in the financial press and conversations with clients:

(1) Is this another late-1990s technology bubble destined to burst?

(2) Is the market’s strength justified based on a genuine productivity revolution made possible by adoption of AI and robotics? To borrow from Buzz Lightyear, can markets go “to infinity and beyond”?

We believe the honest answer lies somewhere in between: it’s neither as frightening as the first scenario nor as effortless as the second. Understanding that distinction matters.

Corporate America, at least for now, continues to execute remarkably well. First-quarter earnings for the S&P 500 grew more than 25% from a year ago, more than double the pace of the average earnings season over the past decade. It’s notable that earnings growth strongly justifies stock market gains. Year-to-date, price-earnings multiples actually cheapened due to the remarkable earnings strength. In the past five years, S&P 500 earnings grew 79%, which is generally in line with the index’s total return. That’s a sharp contrast to the late-1990s technology bubble when earnings grew roughly 67% between 1995-99, but stock prices surged more than 220%. This is why some market strategists are categorizing the recent rally as FEMO driven (Fabulous Earnings MOmentum) rather than irrationally exuberant FOMO behavior (Fear Of Missing Out).

This doesn’t mean there aren’t excesses today. Some corners of the AI and semiconductor trade appear stretched by almost any historical measure. Momentum remains concentrated among a relatively small group of companies, and market leadership was very narrow in April and May. The technology sector was up 36.3%, and just a dozen companies in the S&P 500 were responsible for 75% of the gains! Markets also appear to be rediscovering U.S. exceptionalism. Since early-April, US stocks are the market’s preferred destination, while foreign recovered but continued to lag.

Today’s environment rhymes with 1999 in certain respects, but it is difficult to argue that we are witnessing the same type of broad-based speculative mania. The S&P 500 was up 9 weeks in a row through May. Interestingly, this phenomenon never occurred in 1999, but is observed frequently in the heart of bull markets over the past 40 years. The average forward return for streaks lasting 8 weeks or more was +11% in the following 12 months. That history bodes well for the year ahead. Valuations among the largest companies are elevated (valuation of top 50 today is at 31x), but remain well below the extremes reached at the peak of the dot-com era (45x in March 2000). Importantly, the earnings backdrop today is dramatically stronger; however, investors must consider macroeconomic fundamentals. That’s where the signals become somewhat mixed.

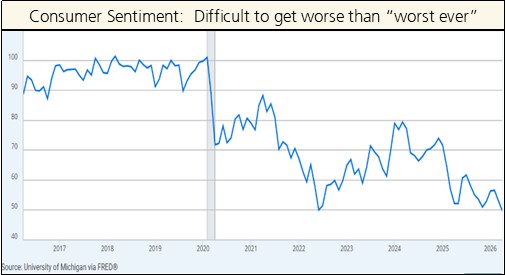

2026 is proving to be a tug-of-war between productivity and inflation, and the battle is intensifying. On one side sits an extraordinary wave of investment in artificial intelligence, data centers, infrastructure, and technology. Productivity growth remains the market’s most compelling bullish argument. On the other side are growing inflationary pressures and extremely sour consumer attitudes. Everyday American consumers are feeling pressures ranging from prices at the pump, to grocery bills, to mortgage rates. The silver lining, and we mean it sincerely: it is difficult to get much worse than “worst ever.” Sentiment is a mean-reverting variable, and historically, readings at extreme lows were more consistent with buying opportunities than sustained market deterioration.

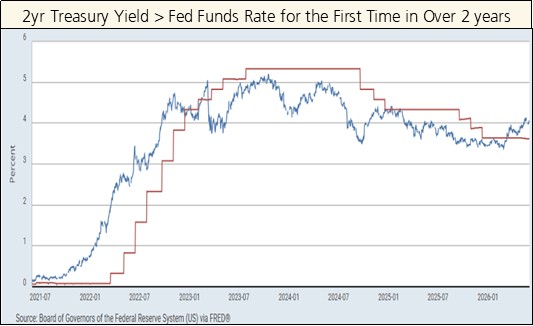

Energy prices are elevated, supply chains vulnerable, and geopolitical tensions continue to encourage deglobalization with a greater emphasis on national self-reliance rather than efficiency. Complicating the inflation picture is that money supply is expanding again, raising legitimate questions about whether inflation will ultimately prove more structural than transitory. The debate is on full display with the Federal Reserve and quickly evolving perspectives about where interest rates should go. Markets spent most of the past year assuming interest rates would gradually move lower. Instead bond yields moved meaningfully higher through mid-May (10-yr treasuries briefly drifted above 4.5% and 30-yr above 5% for the first time since 2007); the market’s expectation is that the Fed will need to hike rates. It’s all happening with the arrival of a new Federal Reserve Chair.

Kevin Warsh was widely viewed as sympathetic to lower interest rates. Markets, however, appear to be sending a different message. Yields are back at levels which, in recent history, created challenges for stock valuations. Inflation expectations are rising, and the bond market increasingly unwilling to endorse an easing bias while inflation pressures continue to build. This tracks with the historical narrative that new Fed Chairs are often tested early in their tenure. We may be witnessing that process now.

All of this is prompting questions whether it remains a good time to be invested? Recent US and Tech-led leadership is impressive, but the market is not uniformly expensive. Much of the world’s equity market remains considerably cheaper than the United States. International stocks continue to offer attractive valuations, diversification benefits, and exposure to areas of the global economy that look very different from the technology-heavy composition of major U.S. indexes. Quality mid- and small-size companies are also relatively attractive. All of this highlights the continued importance of diversification.

Peter Bernstein once wrote, “I view diversification not only as a survival strategy, but as an aggressive strategy because the next windfall may come from something unexpected.” It feels particularly relevant today. The current market continues to be driven by a relatively narrow group of companies and themes, yet history suggests leadership eventually broadens. It also suggests that the next winners are often found where investors are currently paying the least attention. Should the Iran conflict ease or conclude, we suspect international markets possess meaningful room to outperform domestic equities.

As we move into the second half of the year, the earnings foundation beneath today’s market is genuinely stronger than the late 1990s, and the AI-driven productivity case is more than hype. But the macro backdrop — a new Fed chair under pressure, inflation that may be more structural than cyclical, a consumer being squeezed at the pump, and a bond market that is not cooperating — makes the “to infinity and beyond” scenario feel premature as a base case. Eventually, market enthusiasm can lead to trouble, but as the old saying goes, “bull markets do not die of old age, they are murdered.” Central bank tightening is almost always at the scene of the crime after major market peaks, so how the Fed continues to navigate interest rate policy from here is important to monitor.

The title of this article – “Mixed Signals” – feels appropriate for the current environment. You’ll note that our comments around the Iran conflict were limited; that’s because the market already appears re-centered on the ongoing tug-of-war between productivity and inflation. That remains the most useful lens through which to interpret today’s mixed signals. The AI and infrastructure buildout underway is likely to take far longer and require far more capital and investment than most currently appreciate. In our view, that is what gives the current bull market its strongest fundamental case to continue and keeps recession odds relatively low despite a still-sour consumer backdrop. Stay in the game, but remain selective. Diversification and discipline matter as we continue to monitor and limit exposure to areas of extreme concentration and exceptionally strong recent performance.