The most watched of US indexes yielded slight ground during the week ended May 18, with the S&P500, Dow, and Nasdaq each sliding between -0.5% and -0.7%. Bonds continued to experience downward price pressure with key interest rate benchmarks resuming their inching-up. Weaker equity performance however comes on the heels of an eight day winning streak for the Dow, and an S&P500 that remains nearly +2.5% higher than it was at the end of April. Most interesting perhaps is that what are often thought of as the more economically sensitive and risk-seeking sectors including Small-size companies, industrials and the transports, actually continuing to climb, creating an interesting and arguably positive divergence when looking beneath the surface.

Author Archives: Nvest Wealth Strategies

Robust Earnings More Than Just a Tax Cut Story – Week Ended 5/11/18

US equities rebounded in the second week of May, with the broad S&P500 climbing by +2.4% and more cyclically sensitive areas of the market faring even better (Dow Transports +3.3%; Small-Caps +2.9% at the expense of defensive industries like Utilities -2.1%). The strong weekly performance was likely the combined result of unfaltering strength in 1Q earnings season (nearing a conclusion), softer than expected readings on inflation, and tough trade & tariff talk that seems to be thawing (obviously the situation is fluid and could reverse again quickly). On the geopolitical front, the US also recorded a win from N. Korea with the announced release and return of 3 prisoners back to home in the US.

Tone Change – Commentary for May

Market participants appear to believe inflation is back and will be sticking around. That’s affecting how investors perceive the outlook and direction for the bond and stock market. As such, this may be the first time since 1990 that diversification benefits achieved by mixing bonds and stocks together are changing. Since late January, both stocks and bonds are caught in the crosscurrents of increased negative activity in Washington DC, namely tariffs and possible trade wars. Add tax reform and fiscal spending which are boosting the prospects of rising federal deficits. The markets are also aware 2018 is a mid-term election year, wherein the composition of Congress could change. On the opposite side, still low but slowly normalizing interest rates, plus low inflation, plus a lot of money (liquidity) in the financial system, plus high confidence by consumers and businesses, all combine to provide a support backdrop for the economy and financial markets.

Corporate Earnings Face Off Against Shifting Rate Environment – Week Ended 4/27/18

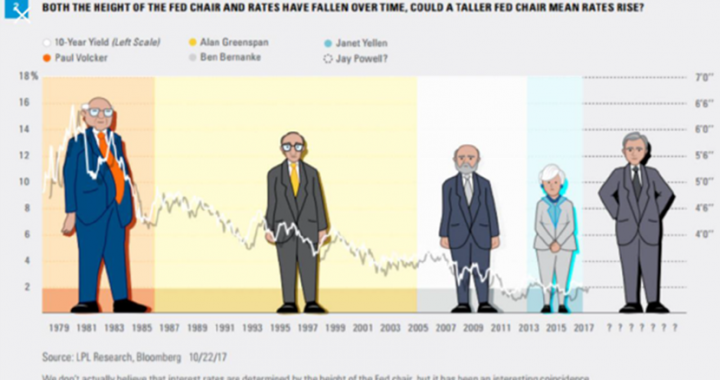

The final full week of April might best be described as a tug of war between big macro concerns and favorable micro inputs. All of which combined such that the domestic stock market was unable to find direction throughout the week and concluded virtually unchanged over the 5 trading days ending April 27 (as measured by the S&P500 and broad Wilshire 5000). By contrast, reference-rate bonds on the other hand experienced a noteworthy development wherein the 10-year US Treasury climbed above 3% for the first time in more than 4 years (it closed the week just under at 2.96%) and the Fed is signaling no intention of slowing their hikes. As recent as year-end the same bond maturity sported a stubbornly low yield of just 2.4%; so the roughly +60 basis point rise represents a +25% adjustment in just 4 brief months. With the US Federal reserve and other major monetary authorities around the globe continuing to communicate a preference toward further normalization, including through rate hikes, rates seem poised to rise further.

Political Volatility Still Driving Financial Markets; Can 1Q Earnings Ride to the Rescue – Week Ended 4/13/18

Choppy market action that persisted throughout February and March is continuing this month against an increasingly unpredictable political backdrop. 2Q began with a horrible first day and stressed week, but the slide was reversed last week despite no shortage of fresh unsettling headlines. For the week ending Friday the 13th, the S&P added +2%; some of the momentum areas hardest hit in recent weeks (Amazon, Tesla, Facebook) also managed to enjoy some of the best relative performance as the negative news flow for them eased a touch. Interesting though amid the choppier weeks is that smaller-size companies have actually fared better than their larger-cap brethren. Of additional merit, credit spreads (often a leading indicator of problems below the surface) tightened last week, suggesting that while US equities remain in closer proximity to the lows of the correction range than the upper, the underlying economic and corporate fundamentals are still perceived as OK. In that regard, the correction is appearing to maturing, and maybe nearing a tradeable conclusion.

“Pulse Check!” – Nvest Nsights Q1 Newsletter

Printer-Friendly PDF Version Here: https://nvestwealth.com/files/newsletter_04_2018.pdf

Pulse Check

The stock market ended the quarter much different than it began. Stocks roared in January with the S&P500 jumping more than 5% to set repeated records; until January 26th. Then, it’s as though the electrician changed the direction of the wall switch. As we wrote in our March commentary, “Agitation Overdone”, the current pullback is the first drawdown exceeding -5% since February 2016 (almost 2 years), or 404 trading days. The February drawdown took 10 days to erase -10%, wherein 83% of stocks declined -10% or more and the average stock gave up -14%. March vibrated back and forth, retesting the February lows. Corrections (-10% decline or more) are never comfortable, but most evolve into new rallies. The evolution process typically involves 3 components – price, time, and emotion. Price action can be quick, while emotional change takes time before playing out. It seems probable that additional time and the evaporation of bullish emotion (sentiment) are needed before the Bull run continues. An important part of any corrective process is converting optimism to pessimism. Today, we are closer than at the early-February lows, which were retested in late March/April – now almost 30% of stocks are down 20% from their highs.

Annuities: Free Lunches & Magic Bullets?

If you are at the doorsteps to retirement, you might regularly receive invitations to enjoy a free lunch/dinner as part of an “educational” seminar on various retirement, estate planning, or trust topics. Often these invitations are made extra enticing by featuring a fancy restaurant for the presentation. Yet as the saying goes, few of us believe these meals/events are without any strings attached; we know there will be some “catch” or pitch of a product or service.

One topic we regularly encounter with new clients approaching us for help is in the area of annuities. While there are advantages and disadvantages to these complex products, in our experience, they are often sold without full and adequate explanation. While we prefer and advocate the use of more customizable, and traditional investment structures (wherein you retain full control of your time horizon, investment options, and access to money), we would stop short of saying or suggesting that annuities are never appropriate. So let’s objectively review one of the most misunderstood financial products available.

Trade War Worries Bring February Lows Back in Focus – Week Ended 3/23/18

It was one of the worst weeks for equities in recent memory as the S&P500 skidded -6% and the tech-heavy Nasdaq gave back -6.5%. The pressure over the last two weeks is bringing the lows set back in early February (following a 9 day pullback that commenced after all-time highs were set on January 26) back in close proximity. Those who were feeling emboldened and relieved by a very abbreviated corrective phase and V-shaped recovery over the balance of February may be starting to feel less confident. Simply, the variety of troubling headlines in recent weeks are the most obvious catalyst for retesting lows set several weeks back and sentiment appears to be eroding based on continued developments around international trade (trade war fears) and ongoing White House drama (budget, scandal, personnel changes, etc). Troubling as those themes are, deteriorating sentiment is ordinarily a requisite condition for corrections to actually have any cleansing effect and deter risky investor behavior.

Trade Tensions Linger, But Did Goldilocks Get New Running Shoes? – Week Ended 3/9/18

Heading into March, it was beginning to feel as if the markets might revisit the correction lows plumbed in Early February amid still choppy trade. The S&P500 gave back more than -3.5% of its rebound over between February 27 and March 1 with sentiment eroding fast on the back of protectionist and trade-war rhetoric emanating from the Trump administration. That may still occur, but interestingly while the fury over trade-related tension remained elevated throughout last week and is still top of mind for many, financial markets began behaving better. In fact, the S&P500 managed to stage several mid-day reversals and close appreciably higher in 4 of the 5 days last week; the full-week experience was actually one of the best so far in 2018. The S&P500 climbed a strong +3.5% with half of that gain occurring on Friday, the 9th birthday of the current bull market (3/9) in concert with what can only be described as a blowout strong employment report for February.

Agitation Overdone – Commentary for March

Early in February the S&P500 and other indexes fell into correction territory. Recall, a correction in the financial markets is a 10% or greater decline from recent highs, which occurred on January 26th. Pullbacks, even in strong uptrends, are historically considered normal. But this was the first drawdown of -5% or more in 404 trading days running since February 11, 2016. Is the correction overdone? Perhaps, but it was probably overdue. Market agitation was brought on by 3 occurrences – feelings that valuation was stretched; a big jump in volatility; and uncertainty about inflation (more below). Also, many investors remain concerned that valuations are stretched, and they became shocked by increased volatility following 23 months of calm and steadily rising stock prices.