“Chloe and Miles grew up between the same bowling bumpers that encouraged risks, inflated confidence, and prevented consequences.” The quote is from “Rock the Boat” by Beck Dorey-Stein. Ever bowled where bumpers are placed in the gutters on each side of the lane? Rolling a gutter ball is not possible. This makes bowling fun for young kids and new bowlers. But, this concept is dangerous in real life – putting up “fake” guardrails to prevent bad outcomes; then when the trouble occurs, extending “forgiveness” without consequences. The same concept can occur in life when we are allowed to enjoy our “kicks.” But when the “bumpers” are removed, unwelcome “kickbacks” can occur. When my boys were growing up they were cautioned, “You can choose your kicks, but you cannot choose your kickbacks.”

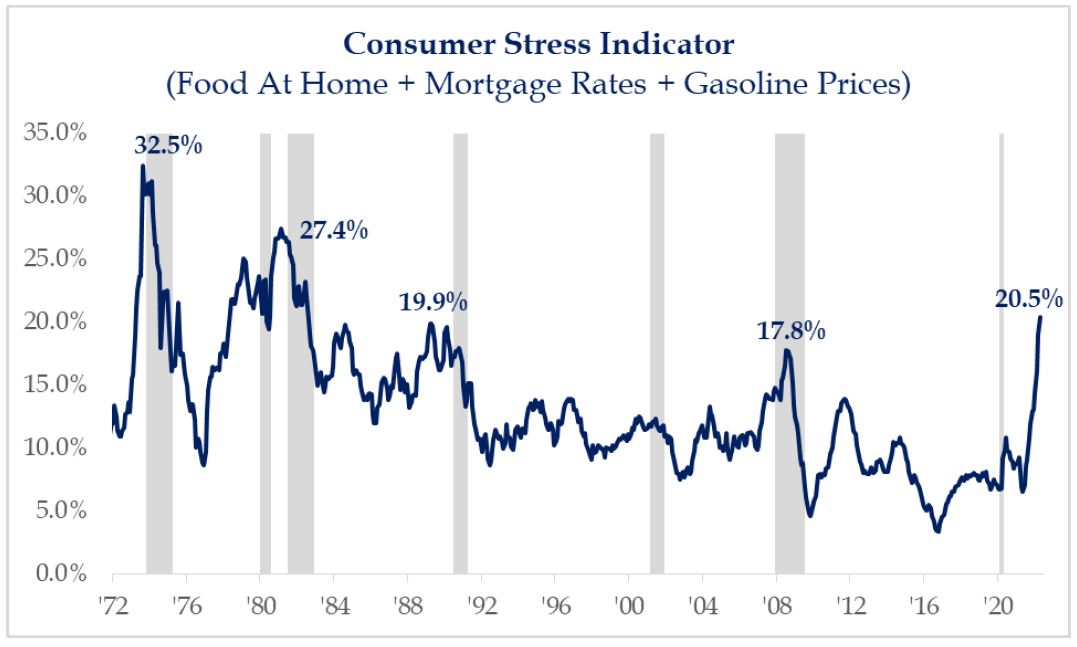

This year, a major change in Fed monetary and government fiscal policy is occurring. 2022 is the year of rates – inflation and interest – both are rising. Until 2022, low/zero interest rates and huge monetary stimulus was used to promote economic growth following COVID’s Great Lockdown. Now both are being withdrawn. Cheap money encouraged risk taking. It created inflated expectations wherein the more risk taken boosted success. All asset prices exploded higher. Success abounded; trouble was not visible. Was it the start of another “roaring 20s? Excess money also created demand far exceeding supply. When demand exceeds supply prices rise (that’s inflation). Some government policies (state and/or local) ignored economic principles: increased minimum wages, “turning off” energy supplies, and even proposing new taxes at the same time as numerous geopolitical risks and the global supply chain remains fractured. These accelerated inflationary challenges and create much consumer pain. “Inflation, like an army of termites, is burrowing its way into big items in the typical family budget. Combining the year-over-year percentage change in food at home, mortgage rates and gas prices reflects the most consumer stress since the early 1980s – Consumer Stress Indicators are at levels not seen in over 40 years (only two periods saw higher readings with both leading to recessions). Recently, we shared about another stress indicator – when the sum of gas prices + home mortgage rates total 10, consumer stress is elevated; currently near 10 (gas approaching $4.50/gal. and mortgage rates of 5.25%). Inflation is a problem, and high sticky inflation indicates a policy mistake.

To fight sticky inflationary conditions, monetary and fiscal policy are being quickly altered. That’s akin to removing the “bowling bumpers from the gutters.” Fed policy is aimed at slowing demand and the economy to reestablish a normal relationship balance with supply (and lower inflation expectations). That means risk taking is not supported, economic contraction is possible, and consumer confidence is waning. Some believe that if the stock market were to “get in trouble” the Fed will not be able to provide a “backstop” of aid as it did in 2008 and 2020; the Fed “put” (bumpers) to the markets is unlikely because they need to battle high inflation. In essence, the government provided the “kicks but/and cannot choose its kickbacks.” Removing the “bowling bumpers” is a key change in the backdrop that influences future economic and investment direction. When market backdrops change, a tug of war is created while investors attempt to grasp the significance of change within the stock and bond market; grasping change takes time, often many months.

The month of May continued to display elevated market volatility experienced YTD; the S&P struggled losing -5.5% by May 19 and approached bear market conditions (-20% decline) for the YTD. A rally during the final week erased the decline to -0.2%. Bond markets are stabilizing following uncertainty about Fed actions to raise interest rates to fight inflation. Bonds usually provide a decent hedge to stocks; but retreated about -9% YTD. The tug-of-war markets create investor confusion – rising rates are giving performance advantage to value and dividend-oriented stocks (moving away from growth and tech). Tactical strategy employed in client portfolios advocates owning more value than growth; it is providing benefit. All client investment objectives generated positive returns during May. But they are still below values from year-end.

The current correction in the stock market is probably incomplete; it recently approached a “sell all” sentiment. Yet measures often associated with selling capitulation (panic, “terror” feelings) are not convincing. We are currently playing by bear market rules, even if a bear market is not official. Bear markets can create rallies. The final week of May produced a good example – stocks rebounded from oversold conditions. History shows the average bounce is about +15% and lasts 5 to 8 weeks. Yet, beware that “dead cats don’t bounce very high.” Bear markets retreat approximately -25% to -30% for the S&P500, sometimes more. Not fun for any investor, regardless of experience.

CAUTION. When presented with historical stats like these, it can be natural to consider selling with the idea of repurchasing later. In reality, one never knows if the current or next “relief” rally is the one that turns out to be durable and powers portfolios to new heights. Many made this mistake during the 2007-09 financial crisis and then remained on the sidelines for years of what turned out to be the longest running bull market in US history. Even two years ago, many sidelined their investments because of fear – COVID Great Lockdown – and missed a new bull market that followed a 30 day drawdown of -34%.

This year, a 4-decade-long bull market in bonds is probably over. That’s why this YTD bond return experience is so troubling. Since interest rates peaked in 1981 at 16% (prime rate was near 21%) interest rates slid like the glide path of a brick; this created a 40-year secular bull market for bonds. Recall, as interest rates fall, bond prices rise; prices move opposite of interest rates. For 40 years, bond investing was generally a positive return experience as investors received not just their coupon interest but also a rising price (albeit with yields getting smaller and smaller – not good for retirees focused on earning interest). With the Fed just beginning to raise rates, investors/savers are starting to receive higher interest earnings – that’s welcomed. While bond returns are generating troubling YTD total returns, it is wrong to dump bonds; it is also incorrect to believe the 60/40 portfolio mix (stocks/bonds) is dead. Bonds do provide greater diversification benefit as interest rates rise.

Back to the idea of “bowling bumpers,” investors should understand that inflation could be higher and last longer than experiences of the last 10+ years. Remember, the Fed is just beginning to raise interest rates to battle inflation (attempting to curb excess demand). Monetary conditions exert an enormous influence on stock prices; the trend in interest rates is the dominant factor in determining the major direction of the financial markets – stocks and bonds. Once established, the trend typically lasts from one to three years. Excess money, the “bowling bumpers”, is being removed from the economic system. That can translate into softer, more muted returns until inflation is restored back toward lower historical levels. This summer is likely to remain troubling with volatility. Mid-term elections are on the fall horizon as well. Time is needed to repair the recent damage of policy mistakes that juiced demand and hindered supply.

What should investors do during the midst of a rain storm? Shelter in place. Generally, you should not do anything goofy – minor changes may be warranted, but nothing dramatic. Be ready; be opportunistic. The current correction is a re-valuation process – providing better values on stocks and bonds. Fundamental (rather than speculative) investing with emphasis on quality is back in vogue; the type of investing we favor and emphasize in portfolios. Corrections provide good entry spots for new money. History shares that stock performance beats bonds, often and by a lot. With time being our greatest ally, stocks are appropriate to own. Investors need to own a diversified mix of stocks, with bonds in their portfolio to beat their enemies – inflation and taxes. Be confident, “sunny” days will return. Just as flowers start to bloom as the spring arrives, new market leaders and portfolio growth will occur as this investment backdrop continues to change; it is a process.

Printer-friendly PDF: Bowling Bumpers – Jun2022