“Sentiment” means an attitude, thought, or judgment prompted by feeling; a refined feeling.

Late last week market sentiment quickly soured, like moving from spring to summer in just a few days; sentiment is very concerned about INFLATION and its influence on the future domestic and global economic path. It’s not about economic strength – strong consumer spending, or company sales/earnings – it’s all about how the Fed and other global central bankers will be “attacking” stressful inflation. 2022 is the year of rates – inflation and interest rates (the Fed just raised rates another 0.75% – the biggest hike in a single move since 1994). Inflation is creating demand destruction. Inflation diverts where consumers would otherwise spend. That growing concern is causing investors to rethink their attitude toward stocks and bonds. After approaching these levels in late-May, the stock market officially entered a bear market down -20% on Monday (June 13) following a short-lived bull market which ran just 22 months (from 3/23/2020 and ending on 1/3/2022).

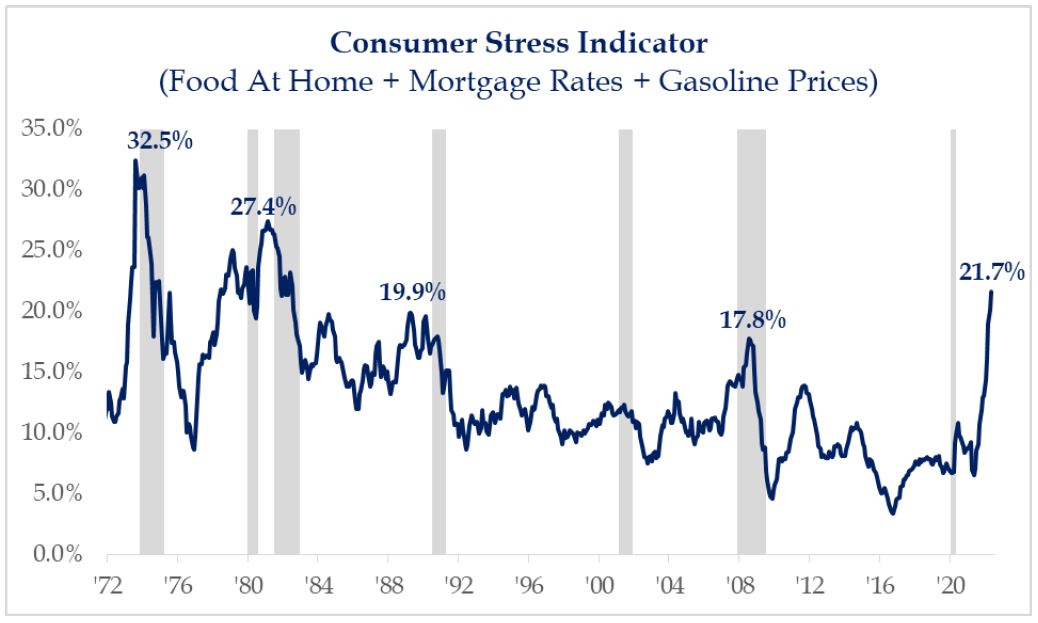

In our June 3 market commentary “Bowling Bumpers” we shared a Consumer Stress Indicator chart. It showed that adding the rate of inflation for “food at home” + “mortgage rates” + “gasoline prices” together, results in a value of 20.5. That level is the highest in 40 years. Following the CPI report this past Friday, that stress indicator now reads 21.7. Recently, the consensus (hope) of investors was that “peak inflation” occurred in March/April. Thus, many were surprised and disappointed by the reported CPI reading at +8.6%. Perhaps they shouldn’t be; CPI is running above 5% for 13 consecutive months; and above 7% for 6 months. No matter how you cut it, consumers are being pinched. In prior periods where the Consumer Stress Indicator reading was this elevated, a recession was the ultimate outcome. [Recessions don’t occur when employment is high/full; recessions usually develop with rising unemployment.] Bear markets and/or recession talk is not the news anyone wants. Yet, I suspect the market “voting” system is pricing these possibilities into current values in volatile action.

It will likely be very challenging to get CPI below 5% by year end. Two-thirds of CPI components are growing at 5% or more. That suggests inflation is broadening out and that it’s going to be stickier for longer. The more time that passes, where the Federal Reserve and other global central bankers are slow to attack inflation, the more entrenched it becomes and harder to address.

Let’s share several thoughts to consider:

- Volatility for much of this year, and lately in particular, seems to be of a “shoot first and look later” mentality. Saying it differently, it seems many fail to do their homework first, but are “story” investors following the herd and then asking what happened.

- In downtrends, rallies often fall short of targets while surprises are to the downside. It’s not uncommon to see a series of market rallies in the context of prolonged bear markets. Meaning, “dead cats” don’t jump very high in a market selloff when bear market rules apply.

- It’s difficult to get control of inflation until the Fed raises rates above the inflation rate. The Fed only just began its tightening cycle; inflation is running well ahead of rate policy.

- Time is an important element in fighting inflation. The longer it takes to defeat, the more it gets reflected in longer-term inflationary expectations – wages, contracts, and etc.

- The inverse relationship between inflation and earnings multiples (valuation) is clear and robust; as inflation rises and is high, valuations are lowered and reduced. That puts stress in the markets.

- Be cautious owning long-duration assets – either long maturity bonds, or stocks that do not pay much/any dividends; dividends are likely to make up an increasing percentage of future total return (income + price change), because interest rates are higher.

- This new bear market (decline of the stock index by -20%) could be longer (time) running – average lasts 20 months; correcting -20% to -40% moving down/up/down and even moving sideways. In terms of magnitude of decline, history shows we may be near the range of a low. Investors should think that the Fed is not in position to provide a backstop to the markets during this correction, as it is fighting inflation via raising interest rates (this is a key thought of “Bowling Bumpers” commentary).

- Monday (6/13) was not likely capitulation (huge fear and exasperation). Capitulation is a process, not a day. Selling was indiscriminate with -46 to 1 breath (46 stocks down for 1 stock up); that’s about as bad as it gets. Stocks making new lows was high; please know that the new low data is “less bad” as a market bottoms. The repair process, which lies ahead often takes time.

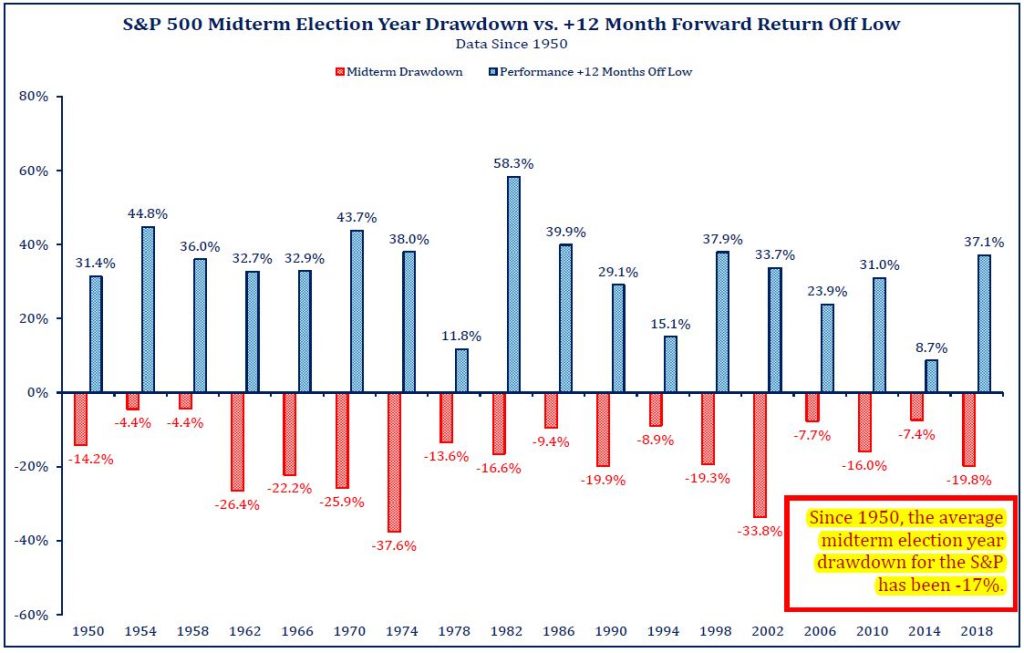

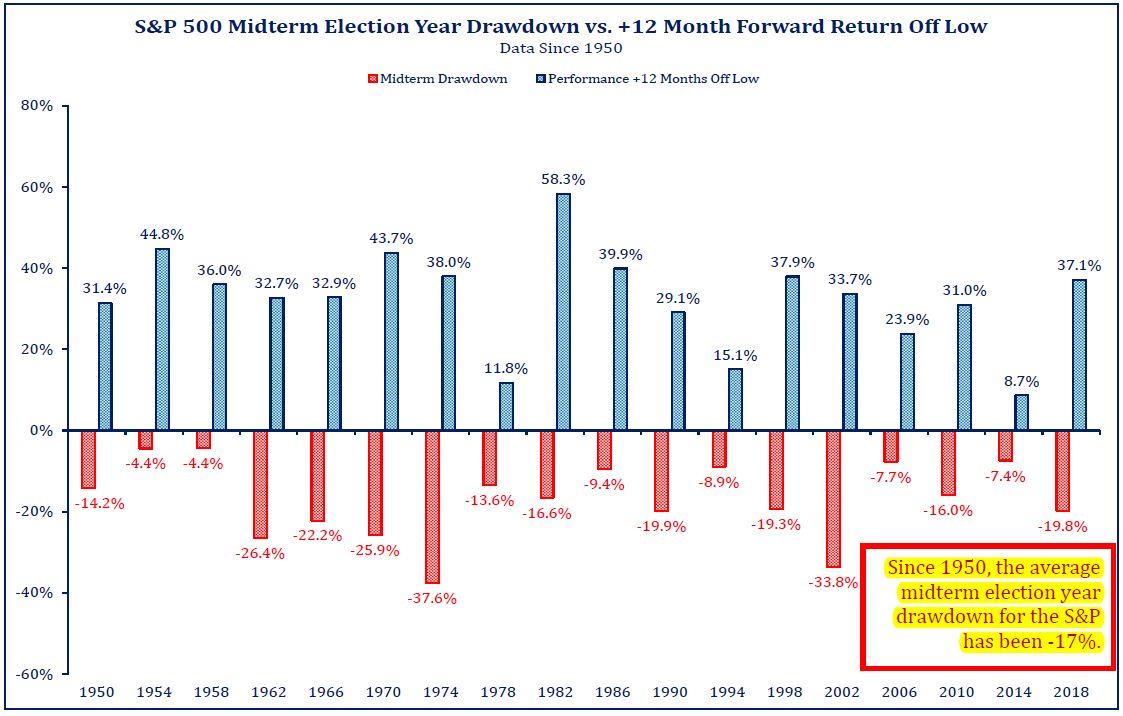

- The most underestimated risk by investors today is Congress moving forward on legislation to raise taxes in a reconciliation package, AND also approve new spending for those hurting from inflation – these would be additional policy mistakes. History shares “Tax and spend” policy ideas to reduce inflation is absolutely incorrect; pursuing such is a sure recipe for higher inflation that only ends with recession. This is one reason why midterm election years generally experience a -17% drawdown on average; in the past, changing the composition of Congress creates policy gridlock which leads to optimism in the market thereafter.

We encourage maintaining your investment time horizon.

- Attempt to be a “Rip Van Winkle investor” (one who takes a nap); it’s never good to be caught-up with daily market wiggles (volatility) and “bad news bears.” Fear-based investing will almost always result in poor return experience.

- Several tactical shifts in client portfolios were implemented months ago – emphasizing value and dividends over growth (big valuation difference); those adjustments remain correct. Tactical strategy is always under review – like, reusing a position-traded MMF in the bond space (yields are rising, and credit or interest rate risk are not present); maybe additional tilt toward value via tweaks away from small-cap growth and/or lower quality companies; not any big changes.

- For those with longer-time horizons, be on the watch for a good time to make further, new investments; a time to buy is approaching. Some areas of the market are really on “sale” falling much more than the indexes. Being opportunistic is very often rewarded (ask Warren Buffett).

It “feels” a bit early to get really bullish on the markets since the Fed only increased rates 75 basis points before today, the Fed’s balance sheet from QE is just beginning to decline, the unemployment rate is yet to rise, and company earnings estimates are yet to be lowered. More interest rate increases are needed and expected; the +75 basis points this week takes the Fed Funds rate to 1.5% (rates were near/at 0% early this year). Yet, it is nearly impossible to identify the market low. Making that guess is too difficult for an imprecise business. Wise investors understand from experience that you must remain invested and be there when the market turns; the markets will turn in a hurry with the advance becoming the next new bull market run.

Lest anyone think otherwise, we too dislike market turmoil. We agonize over it on your behalf. We understand it is a part of long term investing – that “rainy days” refresh, and the “bumps” in the charts are what we climb on (to higher values). We welcome the opportunity to visit with you – in person, phone or via computer. We encourage meeting in person as it affords the best ability to hear/listen to thoughts, ideas and concerns.