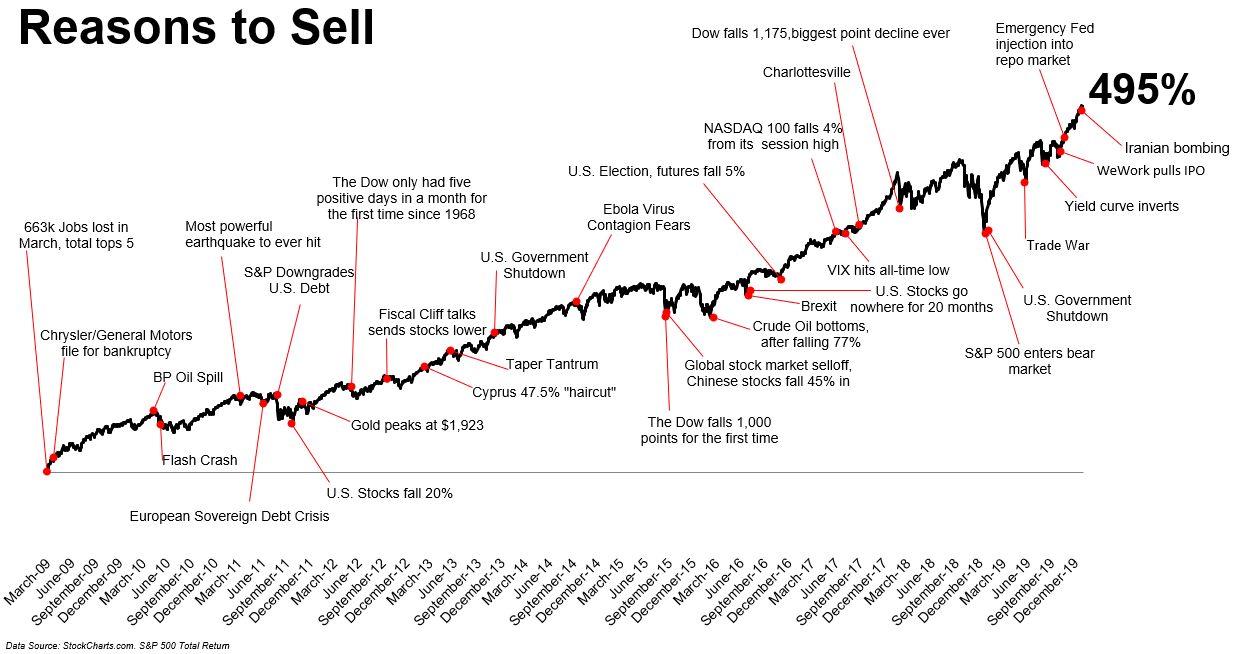

“Forced Perspective” is a technique employing optical illusions to make objects appear closer/farther, or bigger/smaller than they actually are. Filmmakers would for example place a miniature dinosaur close to the camera so that it would look gigantic in the film. Similarly, many tourists at the Leaning Tower of Pisa take a “selfie” with their smartphone camera, making it appear as though they are preventing the structure from toppling. Reflecting on years of experience it is hard to recall a time where it felt like there was more uncertainty than the present. A global pandemic, social unrest, and a polarizing US presidential contest are presently being placed very close to the “camera” by media, creating HUGE worry – a forced perspective. We cannot recall a time where there were not several big worries simultaneously distracting investors. The chart below provides just some past examples.

A key writing theme this year is “Seeing Clearly with 20-20 Vision.” We wrote about current worries while reminding investors to maintain a long-term perspective. Successful investors tactically adjust toward areas they assess as better opportunities, but they should not surrender to cash. This is true amid presidential elections wherein no investment in the stock market (S&P500) made at the beginning of an election year since 1936 was negative 10 years later – including during economic setbacks, or external shocks like COVID. A “time-in the market” strategy was always proven successful. Don’t say it…. “But, this time is different” (4 most dangerous words in investing); or that the prospect of short-term volatility cannot be tolerated. The resultant strategy of “surrendering to cash” should be avoided.

Some investors surrendered to cash earlier this year (and likely regret it today). While it may feel safer going to cash when markets are volatile and/or tumbling, cash positions do not work as was in the past. If you surrendered to cash during the 1987 stock-market crash, you were still making roughly 5% interest; in the dot-com bust, savings earned 4.5%; today money market funds yield near zero and “high”-interest savings accounts yield around 0.5%.

Fleeing to cash also carries high risk of missing the rebound or meaningful appreciation in stocks – which is exactly the experience since March 23. The market turned up even as the news continued getting worse; COVID infections didn’t peak until April, and lockdowns in most states didn’t begin to ease until early-June.

Further, surrendering to cash makes a lasting dent on net wealth. It destroys capital via locking in capital losses, often creating tax liabilities, and crimping growth – all items that can never be fully recovered. Studies show when investors liquidate positions during market downturns, they most often end up with less than if they sold at a later date when money was actually needed for spending. Investors also often fail to consider tax consequences of selling. Paying taxes early is one of every investor’s two enemies; the other is inflation. Cash returns possess a perfect losing record after subtracting the effects of both taxes and inflation. Did you know that if retirees try to “hide” in cash because of market fears, that RMD (required minimum distribution) rules will crush the growth opportunity of your portfolio to provide for the remainder of your life? Holding cash is like having a “parking brake” applied while trying to drive your car. It holds you back. Portfolio values are always reduced.

There are psychological barriers to consider as well. Behavioral studies reveal the longer one holds cash, the longer they remain and cannot change. We observe this phenomenon from time to time, as prospective clients share stories about exiting during the great financial crisis (‘07-’09); or other similar events. While they desire to get reinvested, they simply cannot get comfortable re-entering given current worries of this day. After missing “so much,” they now perceive the market as due for a pullback, which never seems to arrive in a “big” way. If a “big enough” correction did occur, the environment again feels scary. They think they’ll be able to get back in when the conditions are right, but that usually does not occur.

The stability of cash can be alluring in the face of volatility and huge uncertainty. Please remember that the effects of owning cash are not wise. That’s why we advocate using a “buckets of time” focus directly linked to your time horizon and purpose for these savings. This enables you to maintain a “time in the market” focus. We define risk as a permanent loss of capital; yet history reveals that with sufficient time in the market you will be a “winner”.