The rivalry between the Hatfields and the McCoys is one of the oldest and best-known family feuds in American history. For nearly 50 years, violence between the two families raged over who owned two razor-backed hogs that swam in the Tug River, a valley area between Kentucky and West Virginia. Even though the feud ended in 1891, they finally shook hands in 1976; a truce was signed by the families in June 2003. With a total of 60 deaths between both sides, it’s questionable that either won. The Hatfield-McCoy legend was embellished by a brief love affair between Johnse Hatfield and Rose Anna McCoy. Not sure if it was true or not – as a double-barrel shotgun is seldom able to bring sweet marital bliss!

The most significant change to the financial markets in a generation is likely underway today. The Fed is starting to change monetary policy in a way that slows growth. Meaning, following 14 years (since 4Q2008) of easy money policy – via near-zero interest rates + quantitative easing (QE is the Fed buying bonds and building a huge portfolio) – the Fed is beginning to use these two tools in reverse. It is embarking on a fight against inflation with a double-barrel shotgun – tightening monetary policy by raising interest rates + turning off its bond buying efforts of QE. This action withdraws money from the economic system. It will likely be aggressive and hard hitting; maybe even faster than desired. The objective is to battle soaring inflation; but it will also slow economic growth.

Never before did the Fed own a bond portfolio which it needed to unwind; this is new. Both actions (raising interest rates + QT quantitative tightening) will take money from the economic system (money finances growth). This is the opposite of what happened from the huge emergency stimulus employed to terminate the ill-effects relating to the Great Lockdown from COVID-19 (that huge infusion of $$ was greater than the locked economy needed to finance itself). The flood of money inflated all asset prices; higher wages established a new floor for all commodity prices including oil. With the US and global economy shut down and excess $$ everywhere, demand for products exceeded supply. Even now, a still fractured product supply-chain cannot meet demand. The consequence is inflation being fertilized. The Fed and other central bankers seem intent on hitting sticky inflation hard. This current fight will slow economic growth, including earnings growth and earnings multiples leading to slower, muted returns.

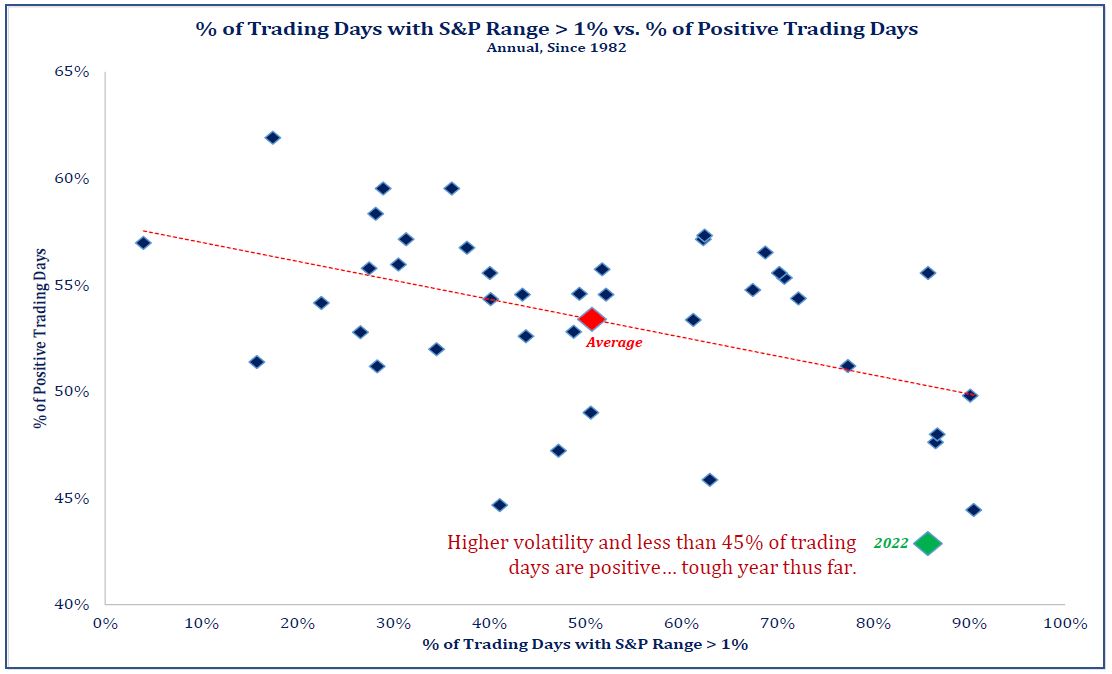

During the first 4 months of 2022, the prospects of a double-barrel shotgun (changing monetary policy) was as uncertain as it was probable. The financial markets – stocks and bonds – displayed unwelcomed volatility; 87% of the trading days (YTD) experienced daily up/down movement of 1% (high) with less than half being positive performing. That hits investor confidence and outlook. It resulted in the S&P500 retreating -12.9% YTD, and down -13.5% since the last closing high on January 3. During April, the index dropped -8.7%, while the average stock is down more than -20% and many tech and growth stocks down even more. The stock market is off to its worst 4-month start to a mid-term election year since the 1930s. The changing Fed policy is altering investors’ math on high-growth equity valuations. Bonds also suffered. They did not provide the level of buffer or hedge to stock volatility that is historically normal; their reduction in value (prices fall as interest rates rise) was the worst in 40 years, losing over -8% YTD. Client portfolios of all objectives lost value during April and YTD. Truly, 2022 is proving to be the year of rates – rising inflation and interest.

It resulted in the S&P500 retreating -12.9% YTD, and down -13.5% since the last closing high on January 3. During April, the index dropped -8.7%, while the average stock is down more than -20% and many tech and growth stocks down even more. The stock market is off to its worst 4-month start to a mid-term election year since the 1930s. The changing Fed policy is altering investors’ math on high-growth equity valuations. Bonds also suffered. They did not provide the level of buffer or hedge to stock volatility that is historically normal; their reduction in value (prices fall as interest rates rise) was the worst in 40 years, losing over -8% YTD. Client portfolios of all objectives lost value during April and YTD. Truly, 2022 is proving to be the year of rates – rising inflation and interest.

Market volatility is likely to continue. The message of the US yield curve seems to be that sticky inflation will continue, and a surprise or two from the economy could drive the Fed to overdo tightening (as they try to be nimble and quick). The Fed appears to be in a “tighten until something breaks” mode. Inflation needs to break before economic growth and employment do in order to achieve a “soft” landing (not recession). The Fed will act and “talk tough”, allowing the market to advance tightening for the Fed. Macro policy is aiming for a period of below-trend growth; yet the Fed does not want to “blow up” the economy. The Fed cannot control global supply (cannot get more oil to be supplied), but it can influence demand. This policy approach will alter demand by raising the “cost” of money; if supply cannot rise to meet demand, then raising the cost of money will cause demand (by consumers and business) to fall, helping re-establish a normal supply-demand relationship.

Using the “expectations” view of the bond yield curve, history shares that the Fed Funds rate could rise to the level of the 10-year Treasury, when they first raise interest rates. On March 15, the 10-year Treasury yield was 2.25% (Fed Funds was near 0%; currently at 0.25%). That suggests the Fed may be able to raise Fed Funds to near 2.25%. If the Fed boosts too fast or too high (2.50% to 2.75% by mid-2023), it’s likely that bond market vigilantes will be yelling “enough.” Of course, when Fed Funds are near 2.25%, the 10-year Treasury yield will be higher too. The 10-year influences the rates charged by bankers for home mortgages, car loans, and credit card rates. As rates rise, demand for homes, cars, and making purchases on credit will diminish. Level and pace of Fed tightening matter to the bond vigilantes.

The current message of the stock market is change – changing leadership from what worked to something new. It’s a split, tug-of-war market experience. Investors however, are worried about which will break first – inflation or the economy? And, could we experience stagflation – slow growth with stubborn inflation? The market is managing the “weight of the world on its shoulders” being displayed with volatility. “Young feller, there’s trouble, and ah know from experience that trouble all us comes in cyclones.”

What should investors be doing? What are we doing as we manage client portfolios?

First, don’t extrapolate too far negative views on what will happen. The Fed does not want to “blow-up” the economy; they want to slow the economy and slow demand to curb inflation before it becomes entrenched. Further, the Fed understands that high interest rates are problematic – to the economy but also to financing the Federal deficits. High rates boost the cost of bond issuance by the Fed; not good for anyone. Long financial market contractions are not politically acceptable.

Second, “don’t fight the Fed” as the old adage goes. We adjusted portfolios to emphasize “shorter-duration” assets earlier this year – bonds and dividend oriented stock funds. That means earning dividends and bond interest payments rather than heavily focusing on appreciation alone. Portfolios own reduced exposure to growth-style (“longer-duration” equities) that depend more on long-term price change for their return. As stated before, rising interest rates are lowering the valuation math (high P/E) of the financial markets – value-style and active management should benefit relative to growth-style.

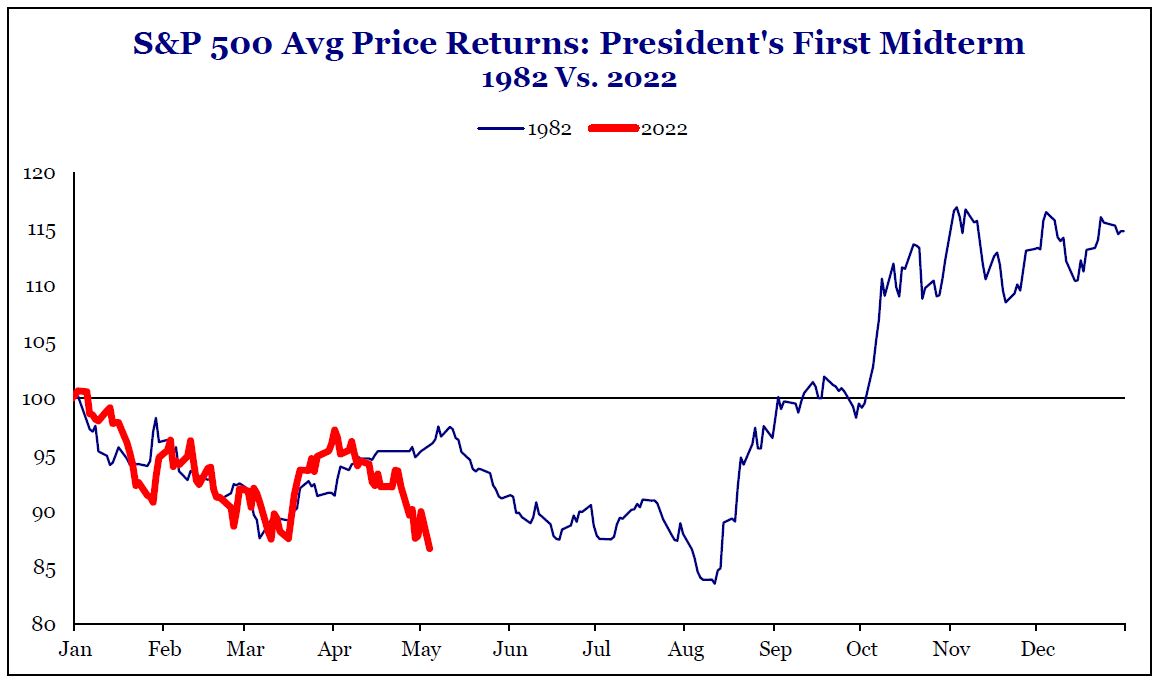

Third, timing the market is incorrect. Patience and staying invested is a challenging pursuit (at times), yet critically important. Problems occur when “bailing out”. Trading out and back-in hinder long term performance; that’s because the best and worst performing days are usually clustered near each other. No one knows when or how long troubling trading markets exist. The market’s dramatic rebound in March 2020, (the start of the current 2-year old bull market) is the most recent example. Recall, the rebound began just as the health-threat of COVID and lockdowns were being announced; the market shot higher.  Or look to 1982 – remarkably similar thematic backdrop to now – it was a midterm election year when inflation was running high and tension with Russia elevated. Weakness persisted thru the summer with anxiety expected to continue. Yet, before the mid-term election a stock market recovery started. Investors should not want to miss the next advance. The red line on the chart shows market action in early 2022, it’s a similar track to early 1982. Will history repeat? It’s impossible to say. Most likely, many investors will not feel confident to invest at the low. No one knows how long increased volatility runs. It is unnerving. The big problem is, timers destroy time and the benefits of compounding – these are THE most powerful tools for long term investment success. Time is an investor’s greatest ally. The magic of compounding only occurs by remaining invested over time.

Or look to 1982 – remarkably similar thematic backdrop to now – it was a midterm election year when inflation was running high and tension with Russia elevated. Weakness persisted thru the summer with anxiety expected to continue. Yet, before the mid-term election a stock market recovery started. Investors should not want to miss the next advance. The red line on the chart shows market action in early 2022, it’s a similar track to early 1982. Will history repeat? It’s impossible to say. Most likely, many investors will not feel confident to invest at the low. No one knows how long increased volatility runs. It is unnerving. The big problem is, timers destroy time and the benefits of compounding – these are THE most powerful tools for long term investment success. Time is an investor’s greatest ally. The magic of compounding only occurs by remaining invested over time.

Warren Buffett wrote, “People who buy for non-value reasons are likely to sell for non-value reasons.” This quote was offered in 1984 when he also shared reasons for not splitting Berkshire Hathaway shares. He explained, “it would attract an entering class of buyers inferior to the existing class of sellers.”

Buffett’s investment life, comments and actions are fully committed to being a long term, in-the-market investor. He rarely sells a stock investment. He buys and holds. When looking at wealth from investments owned by an earlier (older) generation, it’s easy to see how success developed. It was not by being smarter. Success accrued by staying invested – avoid trading; avoid paying taxes by realizing gains. Avoid emotional decisions. Allow time and the magic of compounding to assist in achieving attractive growth in asset value. Oh,… it’s also important to continue to live life under control (avoid chunky spending and withdraws). In other words, control what you can (spending) when the market is not producing fruit.

Investors may be on the verge of a changing investment environment – returns could be muted and less exciting than recent years. Disciplined investors keep on investing through changing investment backdrops.

Printer-friendly PDF: DoubleBarrel Shotgun – May2022