Why does investing in the stock market feel like taking an escalator up, and riding an elevator down? Rising markets seem to be slow upward climbs, like an escalator; the rise occurs over extended time (months and years). But, a correction or market pullback occurs quickly (days and weeks, or months), like riding an elevator down. It’s quick. It seems to take a year to earn 10% in a rising market, but a few days to lose 10%. The elevator experience is always uncomfortable and creates anxiety. Yes, anxiety for us too as we manage client accounts with great care and effort.

Stocks in the S&P and NASDAQ exchanges are near their YTD lows. The S&P500 is off -12.5% since its last market high on January 3rd. It’s off almost -8% in April and retesting the level on March 14. But the average S&P stocks is now -20% off its 52-week high and many stock sectors are down over -30%. Complicating things…bonds often provide safety or a “hedge” to stock market action. Not thus far in 2022; bonds are experiencing one of their worst performances in 40 years. Both bonds and stocks are seeing a “rainy day” at the same time; albeit, that bonds are providing better relative performance. Any pullback creates investor anxiety because no one knows how much or how long a pullback will run. All pullbacks appear like they could run awhile.

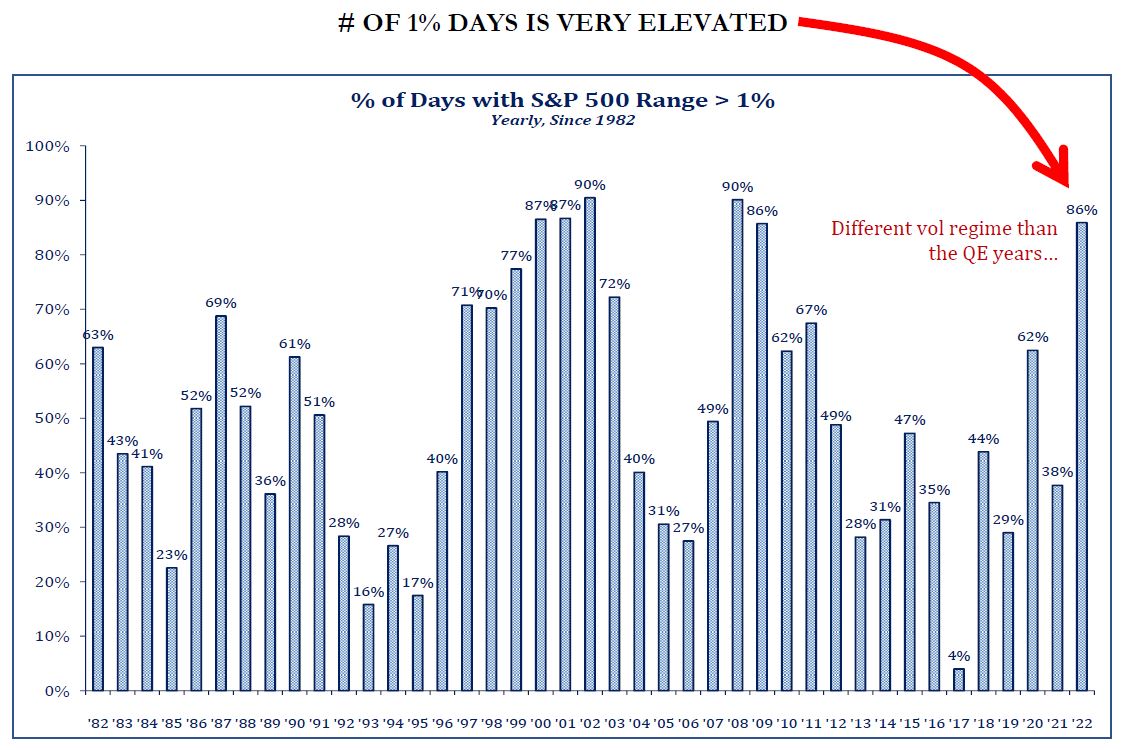

Anxiety is prevalent. So far, 86% of the trading days in 2022 experienced a move up or down of more than 1% (see chart below); very elevated. That’s analogous to riding up/down on an elevator; but this relates to a financial market anxiety elevator = not fun!

- Recall 2022 is deemed “the year of rates” – rising inflation and interest. Inflation rates are high, running at 8.5% annualized; and sticky. Sticky, high inflation should curb consumers spending (slowing the economy and assist the Fed in fighting inflation); this would allow supply and demand to normalize.

- Interest rates are just now being increased by the Fed. Tightening action is aiming for a period of below-trend growth to better balance supply and demand. Often, Fed tightening occurs until something breaks. Inflation needs to break before economic growth and employment to achieve a “soft” landing (not recession).

- Russia/Ukraine war (appears world leadership is pursuing an ineffective “do-nothing” response to expanding Russian aggression), is challenging the inflation fight because the supply-chain is compromised; this is likely to slow global economic growth, particularly in Europe.

- China’s COVID response includes rolling lockdowns; adding to supply-chain bottlenecks that exasperate the supply-demand equation and boosts inflation while also slowing economic growth.

Anxiety is prevalent. A tug-of-war is occurring within the markets – for both bonds and stocks. The characteristic trait during a tug-of-war is volatility; near term action being a back and forth battle.

- Bonds – dislike rising inflation, and bonds dislike Fed tightening interest rate actions. Bonds currently appear “oversold.” There is a back and forth action observable in bond rates – up, then down; challenging the recent peak for rates and then dropping off when news settles. The Fed’s response to inflation is “late”, it’s lagging the market action. Bonds “feel” oversold.

- Stocks – growth style and technology stocks, which led the market advance over the last 10 years (during zero interest rate + quantitative easing) are struggling; they are off -30% or more from their highs. At the same time, value style stocks paying dividends appear to be seeking to take the leadership role, because the Fed policy change (raising interest rates + quantitative tightening).

Investing now involves competing challenges. First, stocks are the best offense for battling inflation; bonds do poorly during inflationary events. Yet, bonds usually provide a good diversification for riskier stocks. Second, if the Fed raises interest rates too much too quick (battling inflation), they could create a recession. During a recession, stocks would be more adversely affected than bonds. That’s the dilemma – invest to beat inflation (own stocks), or invest as if a recession is coming. Third (last), major portfolio changes are not advocated because….The Fed does not want to break the economy; they want to break inflation. With bonds being “oversold” (because they are moving in front of Fed action) and stocks already cheaper, it is appropriate to avoid emotional changes that would involve multiple timing decisions and thereby create greater risk. It is critical to remain invested. Avoid emotional reaction. The markets will continue to experience volatility while the Fed addresses inflation. Economic growth and company earnings should moderate. That means returns will likely be muted during 2022. At the same time, investors’ moods are increasingly pessimistic – but that’s actually a helpful attribute because lots of bad news is already priced-in, making it easier to be positively surprised than it was just a few months ago.

We advocate investors continue to ride the escalator even as repair work is underway.

PS: Watch for our regularly monthly investment commentary coming next week.

Bill Henderly, CFA | April 27, 2022