The Energizer Bunny is the marketing icon and mascot of Energizer brand batteries in North America. It is a pink mechanical toy rabbit wearing sunglasses and blue and black striped flip-flops that beats a bass drum bearing the Energizer logo. The Energizer Bunny advertising tagline is brilliant, “Keeps going and going…” When used as a synonym to describe a person or other object, it means a person who seems to have limitless energy and endurance. Is it appropriate to characterize the stock market rally since March 23 as being like the Energizer Bunny? It appears everything is breaking out. Market strategists indicate this is the broadest rally, both domestic and geographically, since 2013. 93% of the stocks making up the S&P500 are above their 200-day moving average (trend line of the last 200 days). That’s a top decile reading historically. The high reading suggests the market is overbought (high enthusiasm; more on this below), but in fact bodes well for 12-month forward returns being positive. The current market rally “keeps going and going…”

November 2020 ranks as the best performing experience for the S&P500 since 1950, advancing almost +11%. Will December (can’t be December already?) returns prove history true, that it is one of the seasonal best of the year; or did November steal some of Santa’s Christmas excitement? December, for whatever reason, historically favors the YTD winners (currently Tech and Growth) vs YTD laggards (cyclicality and Value). We’ll see. November’s market jump was propelled by big money flows into stocks. Investors re-acquired risk (equities) with enthusiasm because several uncertainties appear to be resolving: 1) election is past and news media negativity is diminishing; 2) huge money supply growth (+23% to backstop financial markets and boost the economy) continues to boost financial asset prices; and 3) Vaccine(s) will soon be available. Together, these positives suggest the economic and financial market struggles earlier this year should be nearing an end. They boost investor confidence.

As you look at your investment portfolios, it should be energizing to see the breakout of values during November. It is even more amazing to see the recovery of values since the March 23 market low, and also for the 2020 YTD. One might almost forget how awful everything felt/was earlier this year. Tactical adjustments implemented in portfolios in April, to turn risk back-on after being dialed-down for almost 2 years, are working well. These adjustments boosted small- and mid-size company stock exposures while reducing exposure to large-size company stocks; we increased exposure to Value (much better valuation than Growth); and continue with full exposure to foreign because of its attractive valuations. In essence, re-establishing prudent degrees of risk in portfolios, and emphasizing the importance of less expensive asset valuations in expectation of economic recovery is beneficial. It can be difficult to invest during troubling times and changing market focus. Yet, maintaining a disciplined long-term investment process is rewarding, even energizing during recent strong market action.

Is there reason to be cautious at this point, given the strong market rebound/recovery? Is the market overvalued? History shares that the current 4th quarter and December in particular, is the best season of the year for stock investments. The biggest short-term concern is swelling investor optimism. It may seem counterintuitive, but the more investors expect great times to continue, the harder it is to meet or beat those expectations. Still, such enthusiasm can continue for some time beyond what most expect. Thus, don’t stand in front of seasonality + momentum this time of year. We would expect 2021 market performance to be less robust as it cannot maintain the current pace of increase without a pause.

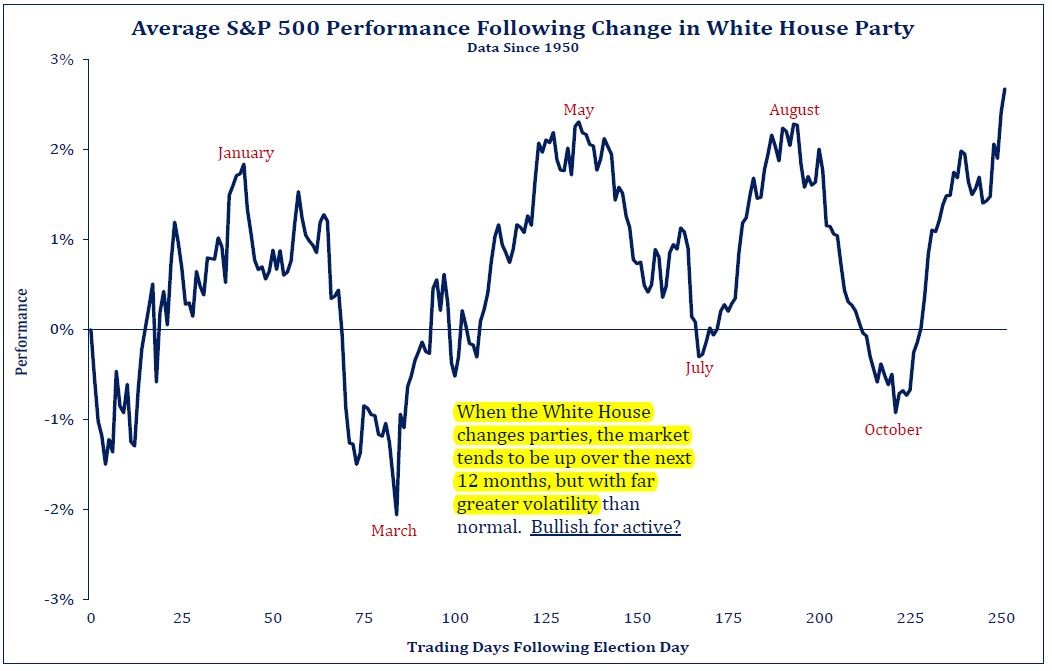

Did you know? History shares that when the White House changes parties, the market tends to rise over the next 12 months but with far greater volatility (up, down; up, down) than normal because new policy direction is often pursued (see chart below). So, 2021 should be a positive experience, if history proves true again.

Remember too, stocks lead the economy by 6 to 9 months; their strong advance supports a significant domestic and global economic recovery is underway. It is advisable to watch and monitor the underlying economic conditions. You hear us advocating that often; it helps one avoid investing with emotion. Generally, the economic building blocks appear in place to transition from recovery to expansion, and thereby assist with the emergence of a new profit cycle to support stock prices. Our domestic economy appears to have enough steam, unassisted by fiscal provision, to keep on going. Even now, the global economic picture is divergent. Europe is experiencing an economic double-dip with new COVID lockdowns (not a good strategy as it slows economic activity). By contrast with the virus “controlled”, China continues to expand (the market price of copper is signaling economic advance). The current challenge in the US is that reopen activity and mobility remain too quick for virus control (especially moving into/through the winter holidays). US policymakers may feel pressure for additional partial lockdowns, particularly if hospitals become full and the medical workforce approaches exhaustion. Still, “Smart Lockdown 2.0” should be less economically impactful than the blunt Global Lockdown 1.0.

At the same time, signs are appearing about upcoming opportunity to further re-open life because of vaccine(s), possible further fiscal stimulus, pent-up demand for services, and increased consumer confidence. Our favorite “economist”, Consumer Discretionary stocks (autos, appliances, etc.), is communicating that the cyclical part of the economy is growing again after almost 3 years of moving sideways (while Tech and Growth advanced). Thus, investors are showing new enthusiasm about 2021 and beyond because it is easier to be more optimistic on the economy’s ability to clear the current disruptive hurdles. And, if investors are looking for undervalued investment opportunities, foreign provides many of the best choices.

One area to watch, with bonds being that focal point, relates to budget deficits of the G-20 and the US in particular. The longer term risk exists that the USA is abusing its “exorbitant privilege” with debt – fiscal (spending and trade deficits) and monetary policy (QE). It is likely that interest rates in the US are higher than if there were not so much government debt. At present, US general government debt as a percent of GDP is 131%. That compares to the Euro area of 101%. Canada is 115%; the UK is 108% and Germany is 73%. When looking at the twin deficits (debt + trade), America’s deficit is approaching a level only previously seen one other time in history – 1942 – at the start of WWII. When you add the commitment by the Fed to do whatever it takes and a preference among politicians for more fiscal stimulus, these actions may push interest rates on bonds higher. How will the US address twin deficits as the economic recovery matures; will policy pursue higher taxes or economic growth? That is an important watching point that will influence longer term asset returns. With more than $21 trillion in US public debt outstanding largely funded via short maturities, small increases in interest rates can create outsized impact on debt repayment and the federal budget. Every 1% increase in interest rates could tack on another $210 billion per year in interest expense. Add that to social spending, dollar weakness could continue; even persist. Tax increases and increased regulations do not grow economies; they stall growth and thereby stall financial asset returns. It’s an item to monitor relative to future economic conditions.

Caution – don’t get caught up on longer-term deficit financing – that remains a challenge for “tomorrow”. It’s Energizer Bunny time. The pink bunny with the base drum is “going and going”. In other words, it’s good to “make hay” when the conditions are right. Stay unemotional and stay invested.

Merry Christmas, and Happy New Year!!!

Printer-Friendly PDF Version Available here: Energizer Bunny – December 2020

Author: Bill Henderly, CFA – December 3, 2020