The US economy is soft and many others around the globe are contracting due to lingering tariff issues between the US and China. Since the first threat of tariffs announced in January 2018, at which time the markets “shook” lower, each additional threat seemed to escalate anxiety and provoke the stock market to lower values. Their prolonged threat lowered US and global economic growth prospects because business leaders are stymied to make long term business decisions involving investments into plant and equipment, and/or hiring new employees. Making things worse, the Fed raised interest rates during 2018, appearing unaware or unconcerned that those actions would also slow economic growth prospects. That adds to “double trouble” for investors. “Quick, call the fire department.”

Recall, our “Geopolitical Landscape on Fire” (September commentary) discussed too much “political noise” – tariffs & interest rates – affecting economic outlooks. When uncertainty reigns (is prevalent) investor focus shifts to interpreting data “at their feet” versus taking the more appropriate long-term view. All views become short-sighted. “The economic house is on fire. Hurry!”

Fast forward. Investors appreciate what they “see” developing on the tariff and monetary policy fronts. Central bankers noticed weakening economic data and are responding – the Fed just completed its third interest rate cut since July; US short rates are -0.75% lower. Politicians also appear to be taking note – Germany talks about fiscal stimulus; there is a strong push for US/China tariff truce in Phase 1; and Brexit may conclude. In essence, a pivot from trade escalation to de-escalation plus global monetary accommodation is really important. “The fire engine is on its way.”

How does the stock market see into the future? Interesting to reflect – just 12 months ago, during the 4th quarter the stock market corrected almost -20% because of rising interest rates and tariffs. “Tariffs can shake the market, while rising interest rates can kill the market.” Recent rate reductions are now showing up in the shape of the yield curve which now looks more normal, upward-sloping (this follows 5 months of being inverted with short rates higher than long rates). A normal, upward-sloping curve suggests the policy mistake (monetary policy too-tight) is being corrected. The stock market leads economic developments. It predicts direction about 9 months in advance. It seems like the “market” anticipated a tariff truce; it anticipated interest rates would be lowered; and it anticipated that other global policy actions would alter a gloomy short-view path. “The fire truck arrived and is fighting the fire.”

As a result of fluid headline worries, the stock market is almost flat over the past 20+ months (when tariffs were first announced). Yet, 2019 (YTD) is shaping up to be a fabulous year, albeit with much volatility. Thru October, the S&P500 advanced more than +23%. During the first 4 months (thru 4/30) the Index rose +18.3%. In the most recent 6 months (May thru October) it gained +4.2% more. Don’t forget, the final quarter of the year is often the strongest seasonal boost to a calendar year performance in general. October started the 4Q with a +2.2% advance – encouraged by important progress on the policy fronts.

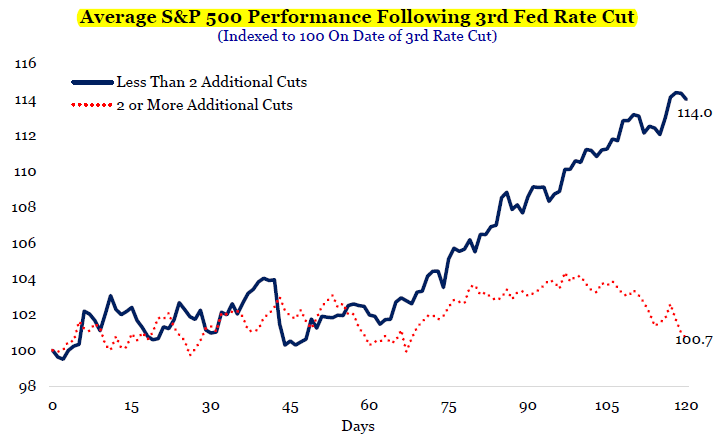

Source: Strategas Research Partners

So, where to from here? Did you know, history shows that after 3 cuts in short rates, the direction of the stock market becomes an important signal (leading indicator). IF the interest rate cuts were truly a mid-cycle adjustment (which we’ll only know in hindsight), and the cutting of rates ends quickly (a “soft landing” occurs), then the stock market rallies sharply (+14%). When/if there were more than 3 cuts in short rates, stock market returns were flat and ultimately deteriorate because rate increases were too much, too quick, and a recession developed. So, if it’s a mid-cycle rate change, stocks should rally.

Also, gaining little attention by the financial press is the observation about a growing money supply, M2. When money supply, which is the financial engine of the economy, is growing faster than the liquidity can be used, the excess money moves into financial assets. The result is a support and boost to financial asset prices; the stock market should benefit. The combination of a soft landing (muddle-thru economy) and excess liquidity provides fuel for a liquidity-driven stock market advance.

Rephrasing it, if the economic conditions remain muddle-thru, that supports the current Bull market to live longer. If interest rates stay low and accommodative; if a tariff truce occurs, then economic conditions are better supported. Only if interest rates rise again (not yet), inflation rises (not yet), and/or corporate taxes increase (not yet), then moderate growth would be uncertain to continue. [Tidbit: history suggests that following the first interest rate cut (in July, now 3 to date), it usually takes a while before the Fed’s institutes a different direction, a rate hike – average of 570 days, median is 180 days before next rate hike.] Accommodative fiscal and monetary policy establishes important pivots for continuing the current Bull market advance.

From a sentiment perspective, not too many investors expect this current Bull market to continue. After 128 months, the longest Bull market in US history is still unloved. It was never one enjoying any enthusiasm. Today, investor sentiment is bearish, not bullish; cautious, not euphoric; certainly not showing irrational exuberance like in 2000 during the tech bubble top. That is a contrarian signal – when most market participants expect something, the market usually does the opposite. Said different, too much pessimism is the breeding ground for positive surprise.

How are investment portfolios being managed given the age of the current Bull market; how are they being managed given all the political “noise” uncertainty? First, portfolios are continuing to be fully invested pursuant the client investment objectives. Second, we continue to construct allocations to stocks and bonds by “dialing down” risk. This tactical strategy for stocks means lower allocations to riskier higher priced areas of the market, and increased allocations to less-risky more attractive priced styles. Bonds remain expensive relative to stock values. In bond world, which provides a portfolio diversification benefit, the tactical focus is to invest in bond funds that look like bonds; pure or simple, higher quality bonds. At this stage our portfolio goal is to capture most of the up-market returns as the current Bull market continues, AND be positioned in front of the future end of the Bull. It will end someday, which no one knows when. By dialing risk lower, we strive to protect portfolio values in part to a market drawdown whenever that might materialize in the future.

It should be encouraging to see progress on multiple policy fronts, both in the US and global setting. The “fire engine is on scene,” and the current Bull market appears likely to continue, albeit maybe not as robust as 2019 is shaping up to be. Don’t forget, the US public is just 12 months away from the 2020 presidential election, which promises to be quite noisy (maybe market distracting). Funny though the financial markets possess a good record for being able to predict a winner. Keep in mind however that who wins ultimately matters less to the overall direction of the market; the bigger effect is on individual companies or certain winner/loser sectors from various policy shifts. Stay tuned.

Author: Bill Henderly, CFA – November 6, 2019

Printer-Friendly PDF can be downloaded here: “Fire Engine Called!” – November Commentary