Do green eggs really exist? Dr. Seuss’ classic children’s book, “Green Eggs and Ham” was first published in 1960. This beginner book was created to be fun and easy to read, perfect for practicing readers ages 3 to 7, and lucky parents too. Readers enjoy the terrific tongue-twisters and unmistakable characters, Seussville, and signature rhymes. Even former President Obama noted during the 60th anniversary year of the author’s books, “Pretty much all the stuff you need to know (to live your life) is in Dr. Seuss.” Do green eggs really exist? A friend who raises chickens indicated eggs are laid in a wide range of different colors and sizes – white, brown, cream-colored, even pastel blue, pink, and yes even green. We know eggs come in small, medium and large sizes, even extra-large. Did you ever eat a colored egg? If you did, you may find it appropriate to quote a favorite storyline…“I do not like green eggs and ham. I do not like them, Sam-I-am.” [March 2 is Theodor Seuss Geisel’s (1904-1991) birthday, and schools call it Read Across America Day.]

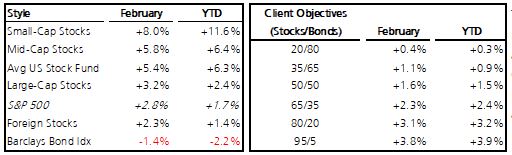

February was an overall positive month for investors of the stock market, but financial markets are getting worked up. Interest rates are rising (meaning bond prices decline) faster and more than most expected. The 10-year US Treasury Note yielded just 0.54% a year ago, 0.92% at year end, and reached 1.58% recently. It may not sound like much, but that’s the fastest rise in rates since 2016. This is creating market volatility. It’s as though the bond market is throwing a “temper tantrum”; testing or challenging the Fed’s communicated monetary policy preference to keep rates low for a long time – until employment approaches the prior expansion low level and while inflation remains controlled. Since COVID and the Great Lockdown, both the Fed and US government are pursuing aggressive stimulus to boost economic recovery. But is the bond market becoming increasingly concerned over stimulus/deficit spending? Utilizing Seuss’s writing style, the bond market might say, “I do not want COVID stimulus for the trees, I do not want stimulus sent overseas, I do not like it (Uncle) Sam-I-am”.

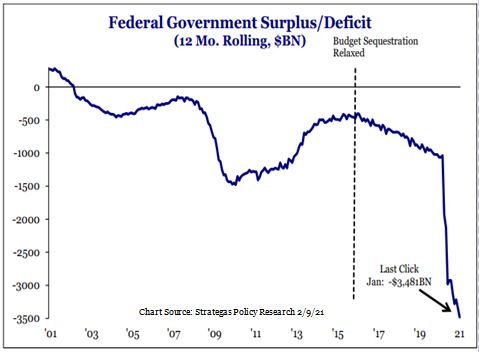

Since last March, M2 (money supply) is growing at a more than +25% annualized pace; much faster than needed to finance economic growth. This excess money is flowing into all asset types boosting prices quickly. When the Fed’s bond-buying program plus new government stimulus of $1.9 Trillion (8.8% of GDP) are combined, M2 will grow an additional +12% this year. As a result, the Atlanta Fed’s estimate for 1Q2021 economic growth is +10%. That’s higher than most economists’ estimates of about +8.5% for 1Q. That’s fast; and M2 growth is arguably too fast, too much. As stated last month, rising 10-year Treasury interest rates toward 2% would surprise most all forecasts. The quick rise of bond interest rates is also a global experience right now.

Rising rates are also creating a rotation in stock market winners/losers. Higher rates are generally favorable to the bank and finance sector because it will allow them to earn higher rates on loans; and the finance sector is undervalued compared to the tech sector (which is often heavily indebted too). While tech was hot for much of last year, it is retreating in favor of value-style stocks (finance and economic sensitive sectors). Looking more broadly, 4Q2020 earnings and revenue reports are mostly complete; all sectors showed strong improvement, with greater growth than expected. Recall too, markets are often more volatile during the first year of a new Administration as they attempt to understand new policies and direction. Also, pullbacks or even a correction (about -10%) are not uncommon following rapid market recovery-to-date. Market pullbacks plus robust earnings and economic growth will enable the valuation gap to narrow. This should allow investors to feel better about remaining invested (versus today, feeling prices are expensive and/or unrealistic). It usually takes 12 to 18 months or more for stretched valuations to appear more normal.

Last April we modified client portfolio tactical strategy – increasing exposure to small and mid-size company stocks compared to large; giving slight emphasis to value (better valuations) relative to growth; and expecting attractive returns from foreign. These tactical adjustments were pursued because market history reflects these areas often recover faster coming from a recession. The broad market and average stock is performing better than the passive indexes. That is providing active stock-picker strategies the opportunity to generate attractive returns. Client portfolios are performing well as this new Bull Market is approaching its first birthday later in March.

One area of increasing concern is the outlook for inflation. This is always a topic of interest because it greatly impacts future capital and consumer spending, profits and market valuations. The stimulus pursuits of worldwide monetary authorities imply faster inflation could occur, yet it is absent over the past 12 years. The Global Financial Crisis in 2008 legitimized the concept of “Bond-buying” (Quantitative Easing strategy) with low and negative interest rates. The Great Lockdown from COVID appears to legitimize today’s no-restraint fiscal stimulus spending; and when combined with the extraordinary accommodative monetary policies from the last decade, we’re experiencing huge government stimulus…. Literally, “a trillion here, a trillion there” is the current “playbook.” (see MMT, following article)

For now, the reopening of the economy and rollout of vaccines provide encouragement that stocks should continue to advance, albeit slower than the recent past. In essence, the stock and bond markets are confirming that the US and global economy is opening up; and last year’s big market rebound was predicting this would occur. The effects of fiscal and monetary stimulus are like “gasoline on the economic fire.” Widespread vaccinations will allow the economy to fully reopen. K-12 in-person learning hit new post-COVID highs as more students return to school, which will allow work-from-home and unemployed individuals to better resume their former work efforts. The unemployment rate will further decline as economic recovery and growth continue. At the same time, the prospects of more fiscal aid, while monetary policy remains supportive, are the issues stoking inflation concerns and market volatility. Investors should expect economic growth to keep surging near term, expect long-term interest rates to rise, which will moderate returns on risk assets from their torrid 2020 pace. Keep a watch on inflation expectations and interest rates – they will communicate approaching problems.

Isn’t it amazing how quick life continues to move? Former First Lady Michelle Obama welcomed the Cat in the Hat to the White House in 2015. Six years later Dr. Seuss’s books are increasingly deemed as unfit for current times. Will Tom Sawyer and Huck Finn be next? What about the music from the world’s greatest composers of yesteryear; and other treasures? Recall the Cat and his troublemaking friends, Thing 1 and Thing 2? As their story concludes the Cat says, “That is that.” And then he was gone with a tip of his hat.” I suspect this imagery is appropriate – there is a limit on how much is too much, whether it relates to current deficit spending or “trashing” some of the best of humanity’s history.

MMT: Modern Monetary Theory – what do you know about the concept? Are most governmental authorities pursuing it today, and thus are we all Modern Monetary Theorists? This theory advocates printing all the money needed to achieve a desired economic purpose. It means, “never has so much money that didn’t exist been spent on so many by so few.” Rapid creation or growth of money (M2) may work when all the world is doing it. Yet for the US, much care is imperative to avoid adding “the straw that breaks the camel’s back.” Extreme care is critical to not abuse the exorbitant privilege of being the world’s reserve currency. The pandemic was deflationary. But too much money creation can lead to inflation, albeit currently desired. The bond markets, maybe the new bond vigilantes are saying, “There is a point of too much. Let’s send a market message of challenge to the Fed (and government), that payday can occur via rising inflation and interest rates which lowers return on most all investment types.” It is not lost on many that America’s public debt was $8 trillion at the end of the last recession in 2009, and exceeds $21 trillion today. Bond interest rates, if/as they rise to 2% on the 10-year Treasury this year, will surprise everyone.

MMT: Modern Monetary Theory – what do you know about the concept? Are most governmental authorities pursuing it today, and thus are we all Modern Monetary Theorists? This theory advocates printing all the money needed to achieve a desired economic purpose. It means, “never has so much money that didn’t exist been spent on so many by so few.” Rapid creation or growth of money (M2) may work when all the world is doing it. Yet for the US, much care is imperative to avoid adding “the straw that breaks the camel’s back.” Extreme care is critical to not abuse the exorbitant privilege of being the world’s reserve currency. The pandemic was deflationary. But too much money creation can lead to inflation, albeit currently desired. The bond markets, maybe the new bond vigilantes are saying, “There is a point of too much. Let’s send a market message of challenge to the Fed (and government), that payday can occur via rising inflation and interest rates which lowers return on most all investment types.” It is not lost on many that America’s public debt was $8 trillion at the end of the last recession in 2009, and exceeds $21 trillion today. Bond interest rates, if/as they rise to 2% on the 10-year Treasury this year, will surprise everyone.

Printer-Friendly PDF: Green Eggs & Ham – March 2021