Too much of anything can be bad. Sometimes, it only takes a spoonful, or even less. In July 2014, the Food & Drug Administration warned about powdered pure caffeine. Usually added to drinks before workouts for an energy boost or to aid weight loss, or as a dietary supplement. It was also used as a study aid among college students. In May of 2014, a high school senior in LaGrange, Ohio died, days before graduation, after consuming one teaspoon of powdered caffeine – the equivalent of drinking 25 cups of coffee or 70 cans of Red Bull. His autopsy found more than 70 micrograms of caffeine per milliliter of blood in his system, more than 20 times that of an average coffee drinker. The difference between a safe and lethal amount of caffeine is very small.

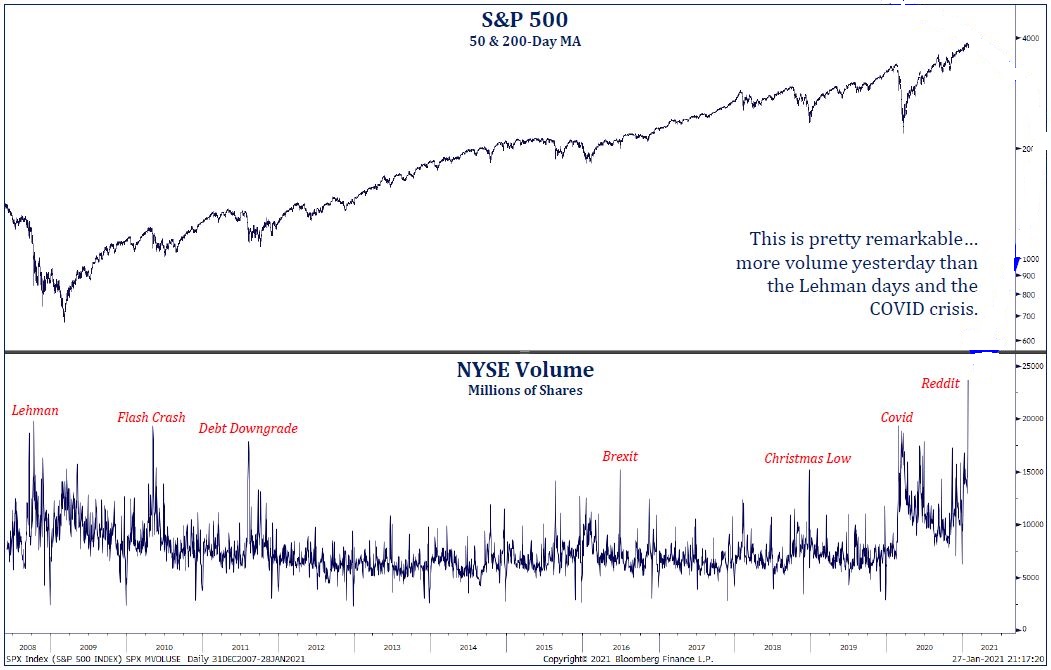

The financial press is currently caught up with Reddit and WallStreetBets message boards on social media being used by retail investors playing or “betting” on stocks. Trading volume on the NY stock exchange recently set a record – greater than huge market events surrounding Lehman (2008), and greater than the stress observed in the system during Covid (2020). The press makes the stock market appear to be on a caffeine frenzy. Observing the message-board provides a picture. “If a post on Reddit contains a rocket ship pointing upward, you best pay attention.” GameStop (sells game cartridges and controllers) never did well until the Great Lockdown with stay-at-home game playing, but recently experienced a meteoric +150% single-day rise. Blackberry stock sported more volume than when people actually used Blackberry devices. AMC (movie theaters) stock struggled last year from virus lockdown issues; recently looks like it “lifted off to the moon.” Is it really that easy – invest in hot “rocket-ship” ideas touted on social media? Yet there is no attempt to understand company fundamentals or the stock trading technicals…It’s just plow ahead with the story-of-the-moment on fast moving message-board postings. There’s more to the recent fury of activity in these hot names and eye popping price changes, including call options and leverage (but this will get too deep). [Quick side question: can you lose your total portfolio value invested in the stock market during a bad market drawdown? A: Not when owning a diversified mix of different stocks or mutual funds/ETFs; but 100% loss can occur when using only options and leverage.]

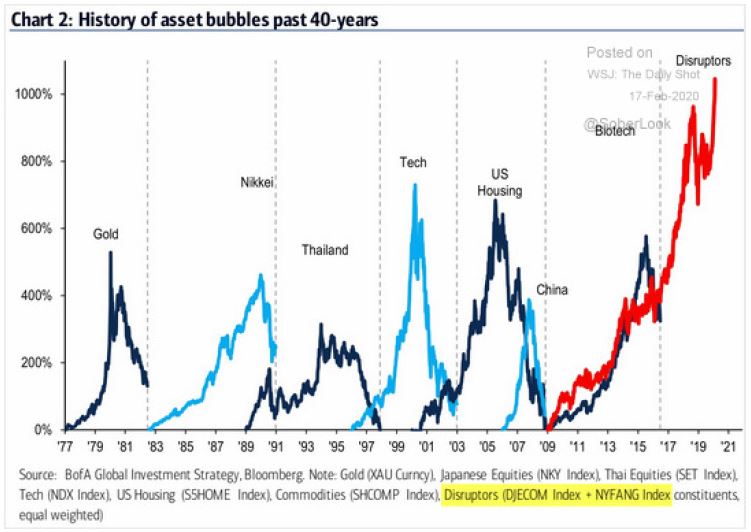

A caffeinated frenzy pulls one’s attention in so many directions it becomes difficult to focus on what’s really going on. These message-board trading experiences also make it seem or feel like 1999, the Tech Bubble. “Rocket ship liftoffs” is a chart pattern whose price action is rising quickly, like “lifting off to the moon.” Price charts of such action show this will ultimately blow up, or crash. History bears this out many times; it’s just a matter of time before the bubble bursts. While there are troubling speculative behaviors occurring, the current market environment comparison to prior bubbles or peaks is premature; it does not hold up. Even though sentiment is bullish, or even “hot” it is not as statistically extreme as Alan Greenspan stated 20+ years ago, calling the tech stocks as trading with “irrational exuberance.” We’re not saying it is different this time (one of the most dangerous comments anyone can make when investing). Let’s de-caffeinate, let’s get rid of noisy distractions and look at the basics.

Yes, the market is experiencing historically extreme valuations, and corporate profits are now showing recovery to pre-covid levels; even a number of countries are showing economic activity above pre-covid levels. Valuations do appear extended or elevated; but this often occurs after a bear market bottom when stocks advance earlier and faster than the economic recovery. Stocks lead the economy by 6 to 9 months. Important, the fabric of this market looks much different than late-1999 when the economy was growing for many years. For 2 years leading up to the market top in March 2000, the advance kept narrowing with only 35% of the stocks rising. That’s like only the generals in the army leading the charge but few solders participate; the market leaders were rising but not much else. There was no support. The same was true at the market peak in 2007 – older expanding economy but few advancing stocks. That’s not today, where 92% of the market was/is rising and economic recovery is just underway. History does not show many examples of a major top when so many stocks are so robust – trend momentum is up across 10 market sectors in early 2021, compared to 10 market sectors’ trend momentum being down in 1999.

Research partners and other sources, including the government’s Congressional Budget Office (CBO) and the Fed expect 2021 to be a “boom” year. They expect economic re-openings by 2H2021. Growth should not be scarce, despite near-term choppiness. If the stock market leads the economy by 6 to 9 months, it’s probable that the huge stock market rebound during the final 10 months of 2020 was signaling the economic “boom” of 2021. We should recall again, stocks and most all assets zoomed upward because of the huge growth of money from government fiscal stimulus and monetary support in the US and globally because of the Great Lockdown (2020); the money supply grew at +25% and remains rapid. That’s astronomical. The economy could not use all that new money to finance growth, so the excess moved into asset prices causing them to rise quickly. There still exists plenty of liquidity. With the economy recovering, time is needed for earnings to rise and close the valuation gap. Even now, as year-end earnings are announced, over 80% of reports are exceeding expectations. In the short run, financial markets should pause, consolidate, and/or even experience a correction. But this provides time that refreshes, allowing the valuation gap to normalize. Generally, the market path in the first year of a new administration (since 1950) is up, but with increased volatility (up/down/up) due to uncertainty relating to the new administration’s policies and direction. It seems likely that returns in 2021 will be less robust; we anticipate the market uptrend to continue, but slower than at the start of the new bull run (in 2020).

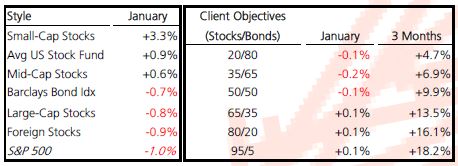

Stock price action for early January continued upward. But momentum fatigue by month end resulted in a slight stock market loss of -1% for the month. [Is that uncertainty regarding new administration policy plans? Maybe. Is it distraction from social media’s caffeine frenzy? Likely.] Client portfolios continue to perform well in the early start of 2021.

It is most interesting to observe this new bull market rise being “tick for tick” following the same path as the early days of 2009 or 1982. The current rise (since 3/23/2020) to January 25 (10 months) market high was +75% for the S&P500; similar to 13 months with an +80% rise off the March 2009 lows, and 14 months and a +70% rise off August 1982 lows. The two comparative times next experienced a correction of -17% and -14%, respectively before continuing the bull market run. Maybe the current pause refreshes – it is subtle de-risking. It could be a modest consolidation with a “real” correction coming later than most expect. That’s because there is still excess money supply with more anticipated from new fiscal stimulus plans; and the Fed will continue to provide monetary accommodation with zero interest rates. The motto, “Don’t fight the Fed” is applicable.

What if the US and other global governments continue to provide strong fiscal and monetary stimulus? There still exist supply chain bottlenecks from the “Great Lockdown”. There still exist lower-paid employees that are experiencing slow return-to-work opportunities even as unemployment rates are down a lot. The challenge is how much additional fiscal stimulus is needed while the Fed pursues its accommodative policy path longer and longer? All government policy tools provide a lag effect on the economy, employment and inflation; though fiscal support checks are quick economy boosters. With the economy growing and expected to boom in 2021, some would advocate fiscal stimulus is working and excess money is still in the system to be used (multiplier effect). Others focus on unemployed, wherein full employment (returning to previous low levels) will not occur until 2024; on that score more spending is forthcoming; there is strong possibility for raising the minimum wage (unlikely good policy for low wage earners with lower education levels). However at some point these pursuits cause inflation expectations to rise. Even now an inflation scare could be brewing – watch 10-year Treasury rates which are at 1.12% compared to 0.9% at yearend. Interest rates rise due to the strength of an economic recovery, excess money supply, and expectations of rising inflation. Most expect US 10-year rates to rise to 1.25% to 1.50% this year; it could be a scare if rates rise closer to 2.0%. Tough policy choices: improving growth but with slow progress for employment. Re-employment is always the laggard with economic recovery (vaccinations and medical cures provide encouragement on the horizon).

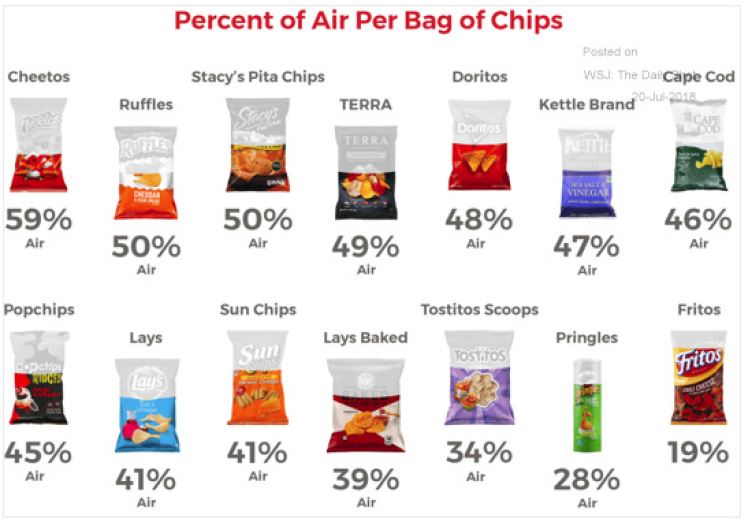

One last thought about bubbles or “rocket ship liftoffs” – they always blow up. Don’t get caught up with the latest social media investment chat rooms. Keep investing with the perspective that no garden produces instant potatoes. Time and being invested in the market are historically proven principles for successful return experiences. If you are inclined to try “story stocks” and momentum strategies, don’t use leverage or options; keep exposure limited to what you would be comfortable losing. Avoid the ‘caffeine frenzy” that distorts reality. If you need to indulge, consider buying a bag of your favorite snack chips. Beware though, the chip bag is mostly air, but better than caffeine.

Printer-Friendly PDF Version: Caffeine Frenzy – February 2021

Author: Bill Henderly, CFA | February 4, 2021