Our last monthly commentary “Weird Words About a New Abnormal” attempted to update about the markets and a frequent question on investor’s minds – “After the significant financial market rebound, should I consider becoming more conservative (for various reasons)?” The weird words were entertaining and appropriate for a heavy topical discussion. Let’s take a cute (humorous) route this month. Let’s lighten the load with some humor while discussing the current market action and outlook. The biggest difference in people who demonstrate resilience and those who don’t is their perception – how they conceptualize traumatic or stressful life situations. It’s all the little things that happen in your day-to-day life; how do you perceive them? One way to change bad feelings is via good doses of humor.

Years ago, two young boys were on a sunny beach; one with sunglasses on, the other without. The one with sunglasses called out, “I’m hot.” The other youngster without responded, “Does that mean I’m cool?” On a different occasion, after glancing at the menu prices at a high-end restaurant, a parent urged the family to be careful when ordering. When the waiter returned to take food orders, one youngster said “another round of water for everyone.” Kids will say the darnedest things at just the right moment. You probably recall other funny comments and events in your own family. Hey, what about Chickadees or Chickadoos? (Later)

August was a spectacular performance month for stocks. The S&P500 advanced +7.2% and logged its 5th straight month of rebound from the March 23 lows. All client portfolio objectives advanced YTD returns. That is really amazing because of the significant challenges of 2020 thus far. Stocks generated positive returns as did many bond types, just not the major bond index. Foreign investments also participated nicely. The stock market rise is unfortunately revealing performance differences – significant performance with/from a small group of “technology-like” and growth stocks, while value related names are generally advancing at a slower pace. In other words, the breadth of the market advance is narrower than desired, particularly during the early innings of a new advance. It’s better to see many troops following the generals (leaders) higher. The performance difference between Growth and Value can be expected to narrow – laggards should rise and/or leaders pause/correct.

Between the March 23 lows and August 31, the S&P500 gained +58.1%. On August 12th, stocks made a new high, above the February 19 peak. That feat was the quickest recovery to a new high, taking just 102 trading days (for market declines in excess of -30%, the next fastest recovery is 414 days post-’87; if the data is widened to include declines in excess of -20%, the 1982 recovery of 58 days and the 1990 recovery of 86 days were faster).

There were a total of 7 new highs during August. Interesting, that occurred while the US and global economies are technically still in a recession. This is the 5th time in US history that the index reached new highs while still in a defined/declared economic recession (others were 1961, 1980, 1982, and 1991). With the other 4, the recession was declared end-dated within the next month.

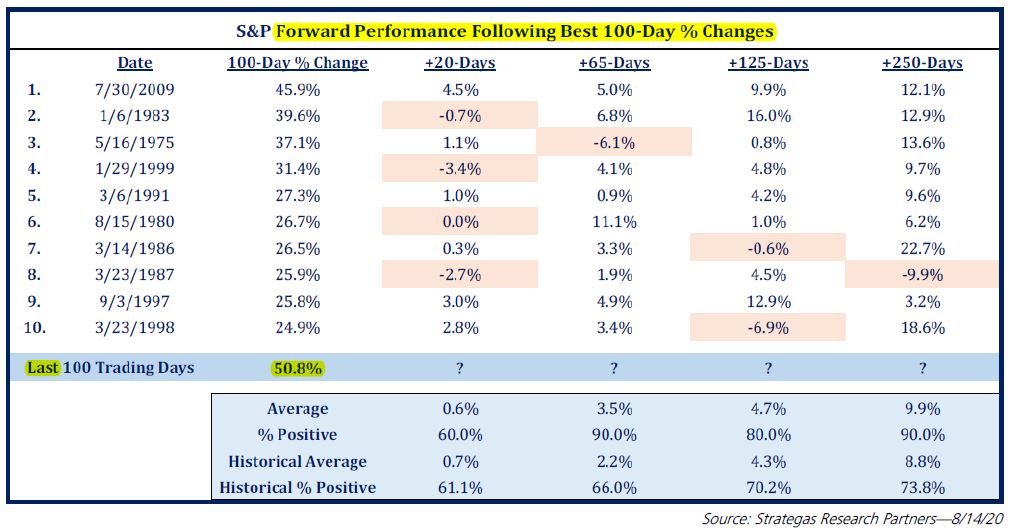

What does this strong rebound suggest for the future? Glad you asked. Looking at historical data… Forward performance following the best 100-day percentage changes advocates staying invested. While the next 3-month interval provided an average +2 to +3.5% increase (a pause and even pullback from the rapid pace), the next 12-months generated an average +9% to +10% advance 90% of the time. Or, looking at market data when new highs occurred during a recession, the average 12-month forward return was +11.4%. That suggests you need to be there (invested).

Historical numbers can be encouraging to recall. How about looking below the surface at the underlying backdrop? These facts can offer an important guide for the future.

- Economy – domestic and global – is firing unevenly, but a durable bottom in activity is most likely intact. In the US, consumer spending is on course to rise by almost +37%, in large part due to the $600/week benefit enhancement; it will likely slow with that stimulus’ expiration/reduction in August. Manufacturing is now in expansion territory; it is +6% above its February peak. These easy jumps are because the rebound started from Lock-down lows in April. The services component, including some small business service areas of the economy are not advancing nearly as strong, remaining -9% below the February peak. In total, the US economy is growing +25% in the current 3Q, and is anticipated to grow an additional +5% in the 4Q. Future economic growth is contingent on progress in containing the virus, as well as actions of Congress to provide additional financial support to unemployed workers. Recent academic research indicates the March/April lock-down tool was too blunt.*

- Medical/health – the globe appears to be learning to live with COVID, and medical solutions (drug, vaccine, testing) to the problem (virus) are progressing. US cases were in a downtrend, and are now stalled. Hospitalizations lag, but are also in an improving downward trend.

- Monetary policy changes were announced last week. The basics of the Federal Reserve changes mean very accommodative monetary policy pursued for an extended period of time. The new policy emphasizes maximum employment to recent cycle lows IF/as inflation remains low. Monetary policy should not change the “trend” growth rate of the economy. Monetary policy should be set to become a “supporting actor,” with Quantitative Easing (QE = buying/selling bonds) used from time to time. Low/ zero interest rates will remain at least until unemployment (exceeding 10%) is cut in half (probably a couple/few years out with 3% GDP growth).

- Deficit spending is expected globally and thus becoming more socially acceptable. The Great Lock-down is making deficit spending an appropriate fiscal tool. Fed Chairman Powell indicated government fiscal policy (spending, taxes, regulations, and tariff tools) should be used to direct the economic growth path; more appropriate tool. At this time, deficit spending is important to further aid recovery from the economic lock-down wherein unemployment is currently high. The deficits this year amount to 98% of the size of the GDP, and next fiscal year will be at least equal size as the US economy.

Together – it means huge government deficits (fiscal policy) with low interest rates and QE (monetary policy) are a likely fuel for risk assets to perform well. Excess money will flow into financial assets, elevating prices further. It is critically important to experience real economic growth. Growth would help current lofty valuations return to more normal ranges. If big tax increases were legislated to fund new social programs, then economic growth will stagnate and financial asset valuations will be challenged. Also be watchful of government regulations and tariffs that pinch GDP potential.**

What’s the market action underneath the surface saying about the future prospects?

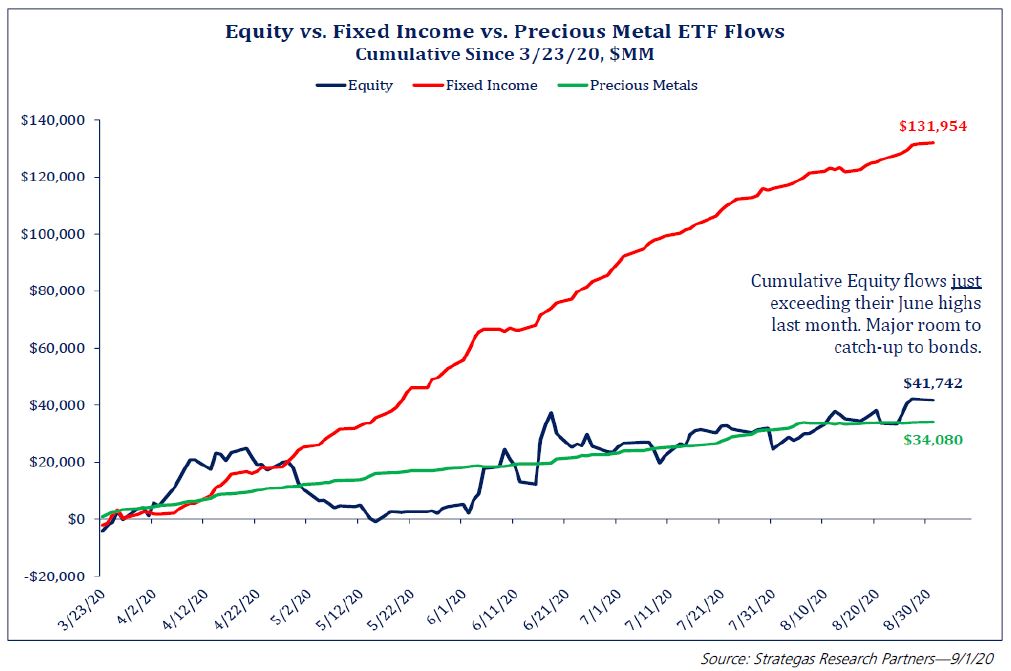

- Money flows into stocks are rising but still trail flows into bonds. A rolling 3-month sum of flows saw its first positive percent change since January; small-cap flows are barely positive for the year; international stock flows remain inconsistent but rising during a 3-month basis (valuations and economic recovery look good). Fixed income (bonds) flows still outnumber stocks by over a 3 to 1 margin since the March bottom. Meaning, many investors remain uncertain and skeptical about owning risk since the March bottom. Despite huge outperformance, some flows suggest investors are becoming skittish on Growth funds. The Russell 1000 Growth index was up +10% in August, but experienced large outflows during August and last 3-months. Since certain mega-cap names are extended, this fund flow development is notable. It is too early to say Growth is transitioning into Value, even with recent fund flows.

- Sector performance indicates the economic “reopening” is underway. Consumer Discretionary stocks are strengthening versus Consumer Staples (products bought regardless of economic conditions). Industrials and Materials (chemicals, industrial metals, and etc.) are giving a nod to cyclicality advancing both here (domestic) and globally. These actions reflect the market’s perception of the economic recovery (stronger than consensus believes) and the reopen trade (ongoing). These sectors (were in a bear market trend for the past 2 years) would not be performing better relative to defensive sectors if economic conditions were still deteriorating.

Owning risk assets at right valuations is the only way to grow portfolio values. It is important to manage risk exposure to expensive single assets, as the investment “knife cuts both ways.” It is also very important to understand underlying fundamentals when managing portfolios. A disciplined, repeatable investment process that remains “time in the market” is proven to be most rewarding. Many bits of information which we are monitoring suggest this rally, which needs a pause, should be rewarding for long-term investors. Timing (getting out and deciding when to get back in) does not work.

More humor…When wearing a face mask, do you sometimes find it difficult to understand the other person? Recently, checking in with a masked medical receptionist, she asked (what sounded like) “what’s your favorite bird?” The answer response was “Chickadee.” The receptionist asked again, through her mask, “what’s your favorite bird?” Again, thinking this was a peculiar question a second time, nevertheless answered “Chickadee.” “No” pulling down her face mask, the receptionist laughingly replied, “I was asking what is your date of birth.” A few days later, a younger person shared this funny incident with another, but called the bird a “Chickadoo.” The other person replied, “Do you mean a Chickadee?” “No! A Chickadoo.” So, how much longer with masks?

*”The Failed Experiment of COVID Lockdowns” (WSJ, 9/2/2020). Did you see this Opinion article? Its conclusions defy common sense. The key thoughts: “Locking down the economy did not contain the spread of COVID-19 and reopening it did not unleash a second wave of infections. Evidence indicates that lockdowns were an expensive treatment with serious side effects and no benefit to society.” Earlier like-studies looking across countries suggested “heavy lockdowns were no more effective than light ones, and that opening up a lot was no more harmful than opening up a little.” In theory, the spread of an infectious disease ought to be controllable by quarantine. But experts cannot explain these study results.

“Be wary of “experts” There are dangers to being caught up in the news industry’s need to say something, anything, regardless of whether or not it may actually be true. The range of opinions regarding …COVID-19 is not unlike watching a championship table tennis match. “Masks are good for you. No, they’re bad for you. Sorry, they’re good for you again.” “Ventilators are critical if one wants to survive COVID. Umm, ventilators might make things worse.” On and on it goes. The fact is that when it comes to a novel coronavirus, there really are no experts.” These quote excerpts by Jason Trennert, Chairman & Chief Investment Strategist at Strategas Research Partners.

**Did you know? The Roaring 20s (100 years ago) followed the Pandemic Influenza (Spanish Flu of 1918); an unusually deadly influenza pandemic. It lasted from February 1918 to April 1920, infecting 500 million people (a third of the world population) in four successive waves. Mortality was high, hitting hard those younger than 5, 20 to 40, and 65+ years old. Following this influenza pandemic, the roaring 20s was a period of strong economic growth and stock market returns relating to the development of the auto industry and production line. Four government policy mistakes (raising taxes, new regulations, raising interest rates, and heavy tariffs) following the stock market crash in 1929 caused the Great Recession to last for more than 10 years; the stock market did not return to its previous highs until the 1950s.

Author: Bill Henderly, CFA | September 4, 2020 – Printer-friendly PDF Version

Interesting Charts: