Much happened in the month of April, a month that probably felt much longer – “stay-at-home” mandates and related economic shut-down continued, air/water quality improved, oil priced for May delivery traded below zero; yet stocks enjoyed a strong rebound. “Seeing clearly in 2020” seems impaired now because of too much news. “Unprecedented” is perhaps the most overused term applied to many topics during this world-wide pandemic event; but so many things truly are “unprecedented.” As a result, there is no shortage of topics that merit comment. But the simple thought is overload – too much news. So let’s pursue a bullet approach to touching on what we see as the important themes. We hope this format and information is helpful. Most important – we pray that you, your family, and friends are staying healthy and safe.

Financial markets provided a dramatic, historic rebound. Is it a rally in a bear market? Is it overdone?

- S&P500 rebounded +12.8% during April, and +30.4% since the March 23 market lows; YTD its decline measures -9.4%. Since the end of the prior Bull market peak (February 19th, wherein the market fell nearly -35% during the next 23 trading days), it remains down -13.8%. Strong one month recoveries are rare; yet history does show another of this short duration. We expect this strong rally (best in over 75 years) will still take time to evolve; bear markets associated with a recession usually last more than four weeks. More volatility is expected before its end. Caution remains warranted, but that does not mean sit on the sidelines.

- Is the stock market too optimistic? There is an impairment in economic fundamentals, suggesting that further gains may be harder. The stock market and economy seem currently disconnected. It’s tough to offer what will happen when governments voluntarily shut down substantial portions of society and the economy. We expect things will not be “normal” for quite some time.

- Equity Bull case rests on central banks easing (interest rates, flooding the markets with money), fiscal stimulus ($$ for virtually “everyone”), momentum, and contrarian sentiment wherein the “pain trade” is elevated pushing investors to take risk (with interest rates low). The old adage – “don’t fight the Fed” is most applicable; massive monetary and fiscal stimulus is “rocket fuel” for the financial markets.

- Equity Bear case centers on lingering economic damage – we avoided a depression, but the recession is just now developing; elevated valuations exist with a re-open that is certain to be choppy.

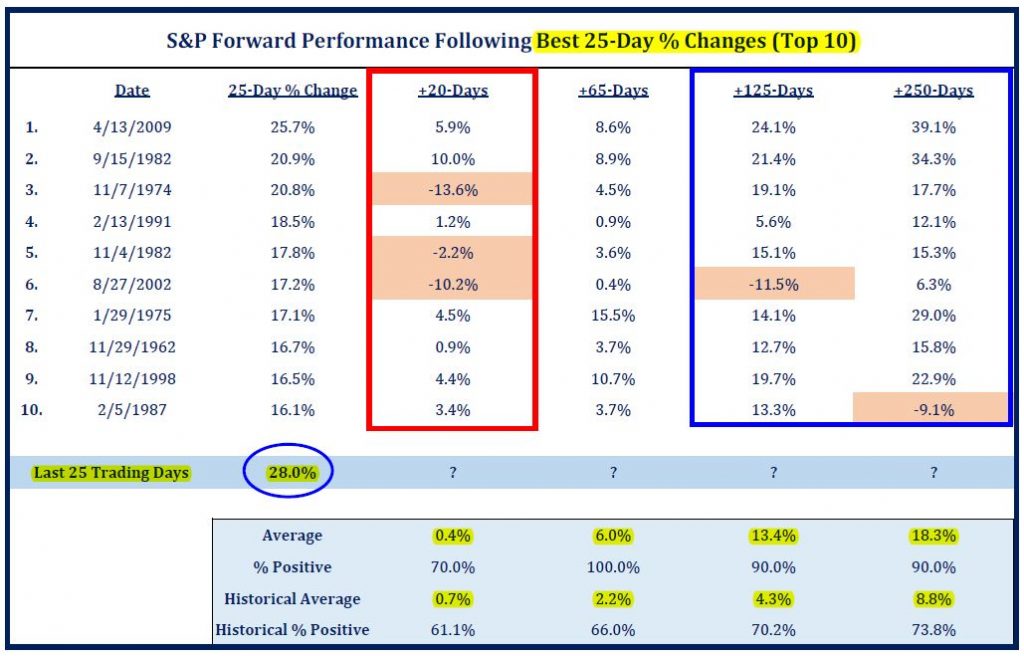

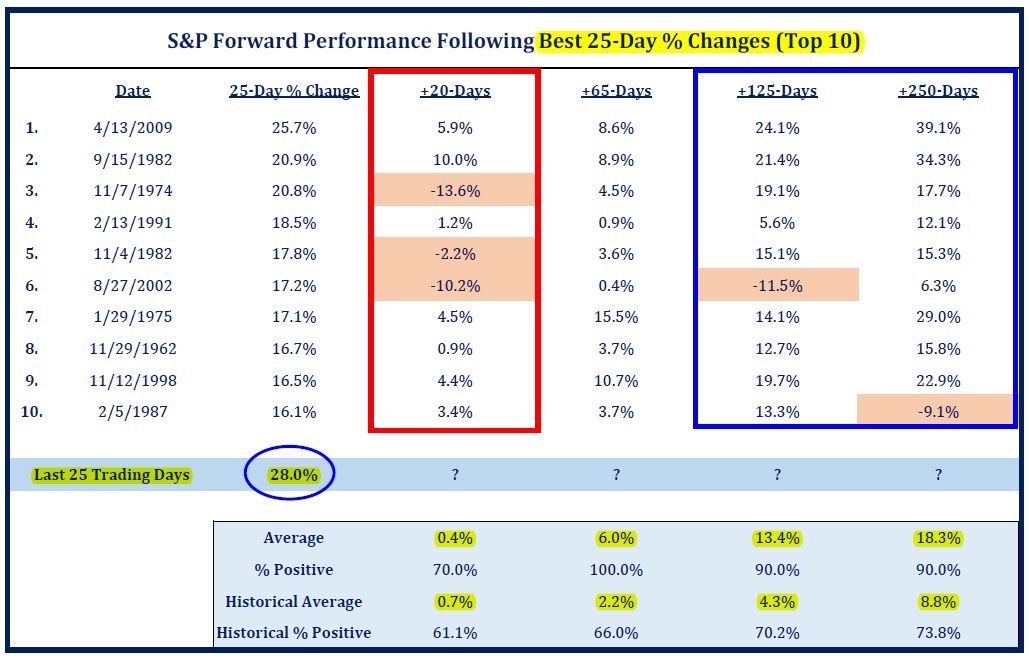

- Bear market action is often down, up, down, up – almost “W” appearing. The first rally off the low ranges between +13% and +43% with +24% being an average; this recent rally was +30.4% (see chart on top of next page). Then, rallies usually slow and/or retrace via a pullback of -10% on average. This historical pattern may unfold because there is so much unknown about re-opening the economy; extreme uncertainty on fundamentals. How massive will GDP decline be in 2Q (market already anticipates this info)?

- Until there is a medical solution (vaccine/drug) to the medical problem (virus), the economy cannot function as it did previously; walking back the economic pain associated with the great lockdown takes time. Even under the best of circumstances it may take a year or more to reach the level of economic activity, employment, and earnings established in 2019. Concerns about a second wave of the virus are likely to slow the global re-opening.

- Globalization is changing/being questioned – may entail greater emphasis toward “made in America.”

- A square-root-shaped recovery (down a lot, up a bit, and then sideways flat) is possible because stranded assets cannot be fully re-engaged. Social distancing will slow bringing assets (retail, leisure & hospitality, travel-related) and industries back to performance success. Also, huge government aid provided during the lockdown may keep big government involved longer in the “lives” of business and people.

How are we investing portfolios with awareness to domestic and global monetary and fiscal policy responses, the economic outlook, and market action?

- Nvest employs the principle of portfolio flexibility – owning “buckets of time” consisting of cash (money market funds for needs within 12 months), bonds (money needed in 2 to 5 years), and growth assets (stocks and/or real estate; money with a time horizon of 5+ years).

- History and recent market action reveals that mid and small company stocks tend to rebound faster and to greater amounts than large company stocks. Further, given the financial damage suffered by many companies (of all sizes), it is critical to focus on stronger, better financed business that will succeed with economic recovery following this recession. Active managed strategies are generally better positioned to evaluate financial and management viability than a passive (own it all) index strategy.

- Tactical strategy, as written in our quarterly newsletter, is being adjusted to position portfolios for an economic recovery. As bonds performed better than stocks during the market drawdown, their exposures exceed the portfolio objective (stock/bond mix), and thereby provide opportunity to rebalance back to objective.

- Bond allocation adjustments involve boosting exposure to convertible bonds (which we minimized over the recent 12+ months), while continuing to focus on active managed bond funds with defined quality and maturity management disciplines. High quality and duration are always keys to how we manage bond allocations for portfolio diversity and protection.

- Stock allocations remain diversified – pursuing almost style neutral exposure between value and growth while placing slight increased exposure to mid- and small-company stocks. We continue to include active managed funds and specialized-focus ETFs in the tactical strategy; active foreign stock exposures offer attractive valuation opportunities.

What do negative oil and negative rates really signal? This may seem to be diving too deep into the financial and commodity market weeds; too technical a topic. Recent oil market action showed that negative yields and negative commodity prices are both the result of the same phenomenon – a deflationary world.

- If allowed to persist, deflationary economic environments are unwelcome and nasty to overcome. When deflationary pressures grow, banks cannot profitably lend (they are the financial transmission for the economy to grow) because regulators turned them into money warehouses (Europe, US, and Japan for the past 20 years). Yields turn negative because fixed costs of regulations amount to high storage costs. Likewise, when a commodity is losing value rapidly because of declining demand (supply building), like recent events with oil, storage costs rise.

- When a rare event happens, it brings with it critical new information – telling us the world changed and a new “regime” is arriving. While this is a microstructure issue, it highlights a macro issue which would not happen if inflation were present and/or higher. Negative-priced oil signals deflation is present. There exist two choices – let it become permanent, or inflate it away.

- Japan (since 1998) and European responses of BIG government – more regulation, greater percentage of spending by state/central governments, more liquidity made the situation worse.

- Arrival of negative rates, global terrorism, massive central bank interventions, negative oil, and even virulent COVID-19 are not one off events; future government policy action is critical. One said to those taking wagon trains in the early 1800s “carefully consider which rut you choose as you will be in it for a long time.”

“Keeping it ALL in perspective” means,…

- Markets don’t bottom on good news.

- “The investor’s chief problem, and even his worst enemy, is likely to be himself” – Benjamin Graham

- “Look at market fluctuation as your friend rather than your enemy. Profit from folly rather than participate in it.” Warren Buffett

- “Buy when everyone else is selling, and hold when everyone is buying. This is not merely a catchy slogan. It is the essence of successful investing.” J. Paul Getty

- “The key to making money in stocks is not to get scared out of them” Peter Lynch

- “Trying to predict the future is like trying to drive down a country road at night with no lights while looking out the back window.” Peter Drucker

Author: Bill Henderly, CFA – May 5, 2020

Printer-Friendly PDF Version

Chart Source: Strategas Research Partners