Nvest (Bill, Steve and Jordan) wishes for you and your family/friends good health, safety and wellness from this COVID-19 virus and the economic challenges. We are greatly concerned by the very real human health impact and ongoing crisis; praying for a timely cure for these current health and economic challenges. Let us know of your worries and if we can be helpful. While it would be unwise to meet in person due to social-distancing protocol, we can visit virtually via web meeting to review your needs, portfolio reactions, and discuss LIVING LIFE financial planning questions. Call or email to coordinate a time to visit.

This quarter you will find several timely updates. First, “The Price is Right?” reviews how swift was the transition from bull market into bear and shares historical perspective; places the size of recent government responses in context; and what we are watching to signal that durable recovery may be near or developing. “Framework for a Path Forward” examines whether the market low observed on March 23 was “a” low, or “THE” low. It is important awareness that retests are normal during periods of market stress, but the market will offer clues beneath the surface about where we are and when/what actions are appropriate to position portfolios for recovery. “Thoughtful Comments for Careful Consideration” is a compilation of notable quotes from highly respected individuals that can be helpful during challenging environments.

A printer-friendly version of the newsletter can be obtained here: Q1 Nvest Nsights

THE PRICE IS RIGHT?

Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

“Seeing Clearly in 2020” is challenged by significant uncertainties surrounding the aggressive spreading coronavirus and the related economic and financial market contraction. The longest running Bull market (started March 9, 2009) officially ended on February 19, 2020, being just days shy of 11 years old. The Bull rapidly declined into a Bear market status (decline in excess of -20%) in just 16 trading days – way too fast and furious. The 1Q2020, losing -19.6%, was the worst quarterly performance since 4Q’08 and the fifth worst quarter of the last 75 years.

Volatility in all markets created a most stressful experience for investors. Many probably entertained great fear, maybe even thoughts to sell everything. No financial asset area (domestic and global) was spared – stocks were banged, bonds were bruised, commodities were hit oil off -66% YTD), as investor confidence evaporated. It is impossible to know at this point if the low established on March 23 with the S&P500 -33.8% from its recent peak (2/19) is “THE” low, or only “A” low. Many market observers believe the dramatic daily market moves – some very violent – relate to algorithmic, computer high-frequency-trading of passive asset ETFs and derivatives (including use of leverage). These HFT actions exasperate both highs/lows of the peak-to-trough and intra-day price moves at great financial and psychological cost to savers/investors and the Fed (providing market liquidity); from our perspective such activity should be suspended and/or curtailed.

“It never feels like the bottom near the bottom.” It is not uncommon to see +15% to +25% moves off the bottom, followed by retesting and/or establishing a lower low. This retesting often further exhausts investor emotion. History shares many examples of this Bear market action. It would be extremely unusual for a Bear market duration to be less than 3 months (two occurred in August 1987 and the other was July 1990 – see chart); the average Bear market duration is 20 months producing an average decline of -38.4%. But, this bear market developed much, much faster than typical, too.

“It never feels like the bottom near the bottom.” It is not uncommon to see +15% to +25% moves off the bottom, followed by retesting and/or establishing a lower low. This retesting often further exhausts investor emotion. History shares many examples of this Bear market action. It would be extremely unusual for a Bear market duration to be less than 3 months (two occurred in August 1987 and the other was July 1990 – see chart); the average Bear market duration is 20 months producing an average decline of -38.4%. But, this bear market developed much, much faster than typical, too.

Because of very quick Fed response – adding liquidity and dropping the prime interest rate to zero – and the addition of Washington’s mammoth $2 Trillion stimulus aid package, these actions are stabilizing the financial market drop at this time. Hopefully the March 23 low proves to be a durable low. Asset values appear depressed more than probably appropriate. The dominant pre-requisite to establishing the low, is containing and providing cure of the virus. This will allow the public to “walk-back” to life (work and social interactions) and provide economic and financial market recovery to be sustained. In the short- to intermediate-term, continued market volatility should be expected relating to new case spikes in COVID-19 and uncertainty around when more normal life can resume.

It is difficult to determine how quickly a restart can occur following the economic “sudden stop.” Extending virus-distancing guidelines suggests the economic “freeze” in America and global growth expectations is not currently in sight, and will take time to thaw. At present, growth expectations are still deteriorating. Likely, the global economy entered a recession during 1Q, which will last through 2Q and possibly into 3Q. A drawn out restart because of prolonged shutdown, could create a slower recovery relating to reducing unemployment (highest level since the 1929 Great Depression at 24.9%). It appears very unlikely a depression will occur. There are huge global monetary and fiscal responses to mitigate economic fallout. The US collective effort is already approaching $4 Trillion (monetary and fiscal actions). Fiscal actions alone represent 9.3% of the US GDP (compared to 5.5% of GDP to overcome the financial debacles of 2007-2008). This government action is 180 degrees opposite of policy mistakes made during the Great Depression (1929 to 1937) – key to avoiding a depression.

“You make most of your money in a bear market; you just don’t realize/understand it at the time.” This thought is counter-intuitive, but very true. Financial markets always provide opportunity to invest – making tactical adjustments to place the portfolio structure into position to recover more quickly as a new Bull market begins. NO ONE knows the bottom, and much money and wealth is permanently destroyed when investments are sold and proceeds moved to the sideline. The great challenge by moving out to find “rest” (psychological relief) is almost

assuredly being late to reinvest; most who attempt buy back in well after the market rise is underway which misses the biggest moves upward. That is where lost money and wealth occur. The only correct way to invest for the long term is remain invested and be opportunistic. Bear markets historically test the resolve of bears just as an initial decline tests the resolve of bulls.

We are all in this together. Stay healthy; stay safe. As for investing, remain invested – Bear markets provide an extra-ordinary buying opportunity with attractive 3 and 5 year rewards.

FRAMEWORK FOR A PATH FORWARD

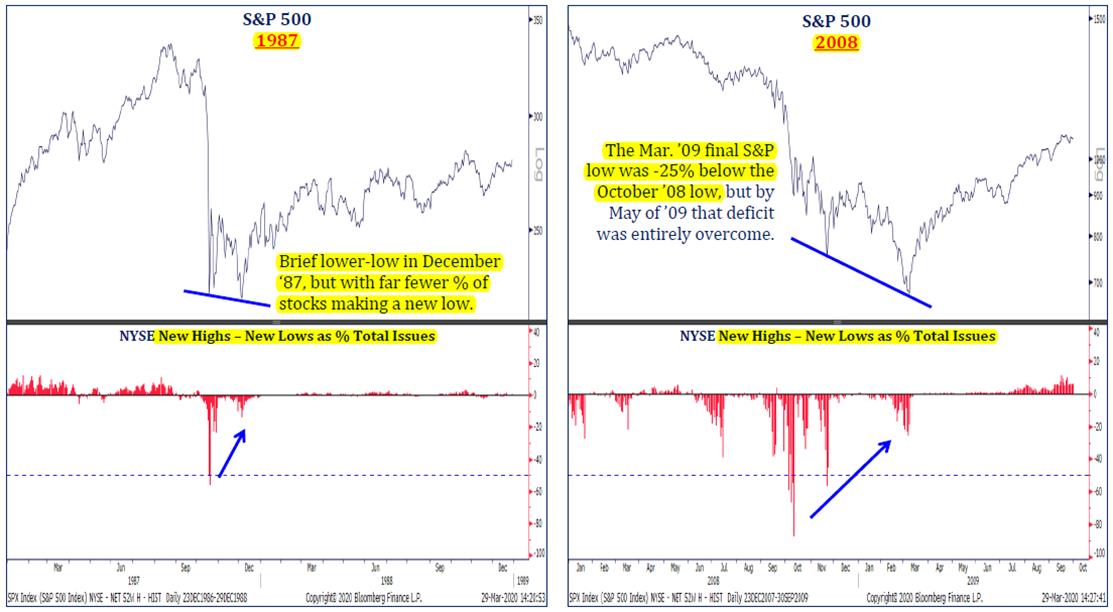

Was the market low on March 23 “A” low, or did we experience “THE” low? As noted in the first article, a review of other bear market experiences indicates “A” low is often retested; both 1987 and 2008 retested and actually formed a lower low that became “THE” low. One way to tell that “THE” low may be forming is by observing the percentage of stocks making new lows is declining (fewer stocks making new lows; suggests individual companies are selectively beginning recovery). “THE” low often occurs a couple/few months after the initial first low. In both 1987 (most similar) and 2008, the low produced a climax of “New 52-week Lows”; fewer stocks made fresh lows several months later when “THE” low was established. “It never feels like a low near a low.”

During Bear market activity, staying invested is most important; there is portfolio management work to do.

- Capture losses to offset/erase YTD realized gains. Why pay taxes on realized gains in taxable accounts? The market provides losses to capture and thereby offset gains (current or future). This portfolio action is undertaken where appropriate and sale proceeds are reinvested in like-kind investments so to not miss market recovery when it occurs (which it will).

- Rebalance portfolios to the Investment Objective (stock/bond mix). With the “rainy day” in the stock market, bonds now represent an excess relative to target. If bonds are not needed to provide for periodic distributions, excess value in bonds (which retained value better than stocks) can be shifted into the stock allocation to re-establish the Investment Objective goals. As stock market recovery occurs and they become overweight to goal, rebalancing occurs again boosting bond allocations and manage risk via asset allocation goals. The beauty of rebalancing when using “buckets of time” investing, allows disciplined investment management to invest in “cheap” assets (underweight) when others are more “expensive” (overweight). It removes emotional from the investing process.

- It’s time to modify portfolio weights and/or holdings – adjust the tactical strategy in stock allocations. Reviewing historical market recovery action provides a forward looking recipe to what performs faster during recovery. That involves prudently dialing risk up (depending on investment objective) – small companies often advance faster than large in market recoveries; style (growth or value) is a more challenging call, with value doing better if/when interest rates are more normal (not zero).

- Modify tactical strategy in bond allocations – continue to focus on quality and pure bond fund structures. Bonds are good portfolio diversifiers, with most clients owning them for their safer market action. Tactical adjustments can offer better risk/return opportunity, providing benefit to total bond allocation returns.

What is your mindset – loss or opportunity? How should an investor turn panic into opportunity? If last month convinced you about being too heavily invested in stocks and hindered sleeping well at night, then take your lumps and dial back your risk (it will be a permanent loss of value). But, if you’re waiting for a sign to buy again, hold your nose, add new money or rebalance your allocation to stocks, and learn to “love” bear markets. How should an investor (not trader) turn panic into opportunity? It’s your mindset – rebalance and work in the bear market. More money is made in a Bear market than is temporarily lost when remaining invested for the long term. It’s not life’s storms that make us fail; it’s how we respond to them. Remain opportunistic (in mindset and action)!!

THOUGHTFUL COMMENTS FOR CAREFUL CONSIDERATION

Dwight Eisenhower (34th US President, & General) – “In preparing for battle, I always found that plans were useless, but planning is indispensable.” All of life, even storms contain unknown elements. Planning for the future is imperative – you must adopt, improvise and overcome!

Walt Bettinger (CEO, Charles Schwab) – “Panic is not an investment strategy and trying to time the market is futile.”

Warren Buffett – “I will tell you how to become rich. Be fearful when others are greedy. Be greedy when others are fearful.”

Peter Lynch (Fidelity Magellan) – “Far more money is lost by investors preparing for corrections or trying to anticipate corrections than is lost in the corrections themselves.”

Benjamin Graham – “Individuals who cannot master their emotions are ill-suited to profit from the investment process.”

Shelby Davis – “History provides a crucial insight regarding market crisis: They are inevitable, painful, and ultimately surmountable.”

“Volatility vs Loss: It’s important to remember that Volatility is different than Loss. Volatility is normal – it’s what the market does. Loss is something that happens when you sell” and don’t reinvest.

Oprah Winfrey – “The greatest discovery of all time is that a person can change his future by merely changing his attitude.”

Market stats:

- Recall the History of the Financial Markets chart – “All long-term stock market charts are up and to the right, with dips, pull backs, corrections, and bear markets along the way. It’s a one-sided mountain that keeps growing upward over time.” Key: being long-term focused.

- Since 1871, market downturns were recovered as follows:

- 33% of market downturns recover within a month

- 50% of downturns recover in two months

- 80% recover within one year

- 95% of the time those big “once or twice in lifetime drops” return to even in three years.

- Collectively, since 1871, the time it takes for the market to recover (top to bottom to top again) is a mere 7.9 months

- The Cycle of Market Emotions reminds – successful investors react the opposite of their normal intuitions (feelings) – buy low (when no one likes); sell high (when all is loved). Challenging!

We are 11 days (rising) into self-isolation and it is really upsetting me to witness my wife standing at the living room window gazing aimlessly into space with tears running down her cheeks. It breaks my heart to see her like this. I am thinking very hard about how I can cheer her up. I am even considering letting her in…but rules are rules (sent by a client).