Careful! Avoid buying life insurance as a savings strategy! Stop buying it as a tax-deferral vehicle for retirement savings!

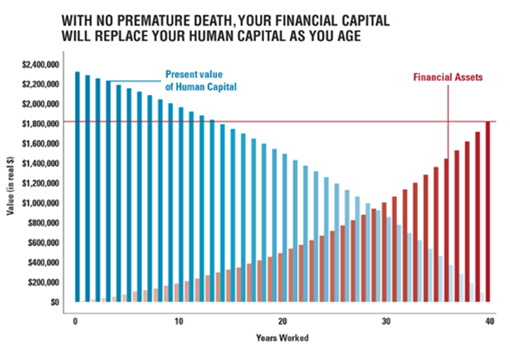

Insurance of any kind is a risk-management tool. From our perspective, an individual should buy life insurance for one reason: because there will be a financial impact on one’s family or business if they unexpectedly die. For most individuals, that financial impact is typically highest early in life when working years ahead are many, financial assets accumulated are low, and financially dependent children and/or significant debts (such as home mortgage) exist. Over time, one’s insurance need generally declines and ultimately reduces to zero at some point prior to retirement.

This “glide path” of diminishing insurance need lends itself kindly to term life structure, providing coverage during a certain period of time.

Life insurance is not a “get-rich-quick” tool or magic bullet. Insurers are in business to make money, and policies are priced in a highly calculated and deliberate fashion relative to probability that your policy will require a payout. Similarly, insurance agents are incentivized to sell as much insurance as possible. Term life insurance is the cheapest form because insurance companies know that most policy owners will outlive the covered period and a payable death claim will not occur. Yet because term is so cheap, it means that the commissions agents receive are quite low. There is a strong incentive to promote other forms of “cash value” or “permanent” life insurance such as variable universal life, whole life, and etc. that pay far greater commissions. Even cute riders bolted onto term life insurance dramatically increase the sales commission for a life insurance agent.

Cash-value life insurance structures may sound appealing in that premiums paid are not totally forfeited with time and can accumulate cash-value. But inspecting under the hood, the underlying cost of insurance remains akin to the premium you pay for term insurance. While one is young, this underlying term insurance cost is low (because your probability of death is low), but as the insured individual ages the price of insurance rises. Agents often encourage buyers of cash-value plans to over-fund policies so that later in life their payments will not escalate due to these rising mortality costs. Yet, observing policy values reveals that rarely does the over-funded cash value grow as was promised. Policies often crater, and/or promised death benefits are reduced.

Remember the sales promise, “cash value grows tax-deferred,” right? True, but life insurance is one of the most expensive ways to save. Whole life policies pay low-single digit dividends (bond-like returns at best), but after the cost of insurance, administrative expenses, and the deduction of other available riders, returns on cash value are eroded. Projections often show a policy must be in effect for at least 10 years to break-even when premiums are regularly paid. Yet in our experience that breakeven period is often overpromised. Variable policies (those accruing based on some market-related benchmark) are very dependent on strong return performances during the first few years, or the insured may be required to pay higher premiums later to maintain the same death benefit.

Hey, also remember that the agent stated the cash value could be withdrawn tax-free in retirement? This is partially true: premiums paid in can be withdrawn tax-free, but to access any growth one must take a loan against the policy to preserve that tax treatment. Withdrawal of earnings anytime, is taxable. As you might guess, “loan” means paying interest at the same time your cost of insurance is rising! In that regard, entering into a permanent life insurance contract actually reduces one’s financial flexibility – especially amid a household budget crunch when life insurance premiums might be the first item a family looks to trim.

Of course there are valid reasons to buy these more complex and expensive forms of life insurance, such as an estate larger than the Federal (or state) exemption; there are dependents who will need more assets than can be passed down; or your privately-held business partners want to fund the purchase of your ownership share if you were to die. Please note, the idea of a “savings vehicle” is not on this list.

In general, insurance should be kept as pure and simple as possible. This means insuring with a correct-fit amount for the period of time needed and avoid costly riders. If your goal is saving (for college, retirement, or anything else), traditional structures are far less expensive, provide greater growth potential, and keep you in total control! If you already own more complex structures, we invite you to share the details with us so we can help you evaluate its merits based on your “Living Life” financial situation. If cash value exists, it may be more effectively deployed to aid achieving your long-term goals.

Source of chart: InvestmentNews, Blair duQuesnay, September 17, 2018