As we enter the 2nd half of 2019 it is difficult to recall a time when the market was hitting new highs but investor attitudes felt so indifferent. Rather, sentiment is guarded. This is likely due to a Federal Reserve that raised interest rates 4 times in 2018 and now appears to be “too tight” when also considering persistent uncertainty from international trade and tariff talk. Taken together, investors perceive the global economic outlook is at risk.

As this quarter’s Nvest Nsights newsletter highlights, the good news is those worries seem to be keeping the close attention of those with the power to resolve. “Can’t Live There” and “Missing – Reward” are efficient reads on the key items driving financial markets and context about the current (and now longest) economic expansion in US history. Strong starts to a year bode well for the balance, but we also submit that the path of both the market and policy (trade & monetary) adjustments may not be smooth. We also share several “Frequently Asked Questions” being received recently from clients; we hope you find those relevant and helpful.

Click Here to Download the printer-friendly PDF version of our newsletter or continue reading below.

“CAN’T LIVE THERE”

Often, we look to the past with fond memories, wishing the “good old days” were today. Life seemed more simple, fun and easier. During the second quarter, investors experienced a net good experience – the S&P500 rose +4.3%. The bulk of the 2Q returns were derived in April (recall and reread our May “Four for Four” commentary). Optimism vanished in May after tariff talk with China broke down; the market dropped over -6%. In early June, the Fed communicated it would monitor the economy closely because of trade tensions, and respond with a rate cut(s) if the outlook deteriorated. This news generated a best June performance since 1955, with the market index rising +7%. In general, the full quarter was positive adding to a strong 1Q start. But the 2Q experience was quite volatile moving from start to finish.

It’s difficult to imagine a time when the market was hitting new highs, yet investors feel so indifferent (if not even hostile) to economic and market events. Investor sentiment is very guarded as money moves out of stocks into expensive priced (low yielding) bonds. After raising interest rates four times in 2018, the Fed is too tight for a trade war; and the trade war is sticking around. History shares that the Fed often tightens – raises interest rates – until something breaks. That is a policy mistake. At the moment, the market is communicating that the current mistake is small – the Fed only overtightened by one hike, but the Fed should make an adjustment.

At the start of 3Q, three market takeaways exist:

- Economic forecast shows some downward data revisions, likely due to business leaders being uncertain of the future, thereby placing a hold on making too many future plans;

- Tariffs look deflationary – they are slowing the global economy and outlook;

- Central banks (US and many globally) are responding (ready to ease if necessary = important).

Good news: just a day or so ago the US and China announced that tariff discussions will resume. This is net positive for the markets. Yet most investors recognize talks are fluid, and the process will need to play out; it could be drawn out. In the meantime, deteriorating business confidence could lead to weaker economic growth and earnings. Good though, the Fed made clear that it is ready to help.

Investors wish they could suppress the politics so affecting the markets. A simple tweet can swing the mood of the markets quickly. Yet, we all know it is impossible to turn back the clock and return to more simple market trading days. Creating investment success requires remaining invested though the noise and distractions, through the good and bad. We can alter risk in the course of managing investment portfolios. Pursuing an established investment objective is a key component to achieving long-term goals. Remember the investor mood just six months ago: in December 2018 after the market drawdown of -19.4% was followed by a rebound of +18.5% during the first half of 2019. Being out of the market would miss the rebound and subsequent new highs. “It’s okay to visit the past; it’s inappropriate to live there.”

“MISSING – REWARD!”

“Wife and dog missing. Reward for Dog.” Or another… “Wedding dress for sale; never worn. Will trade for .22 pistol.” Bad humor; sorry.

The current Bull market and economic recovery are both setting additional or new records in July as the current Bull market is now 124 months old, AND now the economy becomes the longest expansion in US economic history. This economic expansion and bull market can “grow older” if a policy mistake does not create its demise. Given these historical age marks, managing portfolios is challenging. We still pursue an established client investment objective (stock/bond mix), but are dialing back risk as we tactically manage the stock and bond allocations. Dialing-down risk means we are limiting exposure to expensive areas of the stock and bond market and giving slightly greater emphasis to lower priced or less expensive areas. Recent news is net positive. It is important to remain a long-term “in the market” investor to continue to capture the up; but dialing-down risk will generally cause a slower performance experience. One objective at this stage however is to capture less down market action should the environment deteriorate.

The current Bull market can continue to advance, as/if the economic backdrop provides underlying support. Presently, the Fed is too tight for a trade war, and appears ready to respond should economic growth and business confidence soften too much. Market interest rates on the 30-year Treasury Bond is about 2%, or 50 basis points lower than any expectation to start the year (the 10-year Treasury is 90bp lower since YE). Most anticipated interest rates to continue to rise, yet current market rates are the lowest since 2016. Slow growth with “lower for longer” interest rates should remain the story-line until tariff issues with China are resolved. [Some recent monetary information that is not making the news – the M2 measure of money supply is growing. If it continues, a growing money supply often results in asset prices rising because excess money makes its way into investments. That’s good news.]

Portfolios are advancing with the markets. Interesting to us, large stocks are generating higher YTD returns than small; and expensive growth-style continues to beat value by a wide spread. This may continue through the balance of the current Bull market. Further, dialing down risk is working – increased exposure to large stocks is aiding portfolio performance as small stock performance is soft. Also, portfolios own growth and value. Value is performing but at a slower upward pace. But, during times of market drawdown, like in May, value investing provided better portfolio drawdown protection than if growth exposures dominated the tactical strategy. In bond world, we continue to focus on quality, traditional, time-tested bond fund strategies that behave like bonds. There are too many new “go anywhere” bond strategies that reach for risk via owning long maturity and/or low quality to provide higher yield. Those funds provide less safety and will get crunched when a flight to quality event occurs during troubled times. Bonds are meant to provide diversification and risk reduction. We try to achieve attractive total returns from bonds, but with understandable risk. Keeping bonds simple provides better “sleep at night” experiences when bad weather arises.

So, how does the title fit with this commentary? Not sure! But, we would alter the reward poster. It is better to reward for the return of a treasured wife, than for a dog, even if a dog is “man’s best friend.”

FREQUENTLY ASKED QUESTIONS

The S&P is at all-time highs…what’s next? With the S&P trading to new all-time highs in recent weeks, investor sentiment is not confident. There is not excitement or exuberance for owning stocks. From a contrarian perspective – equity funds continue to see outflows, while monthly data inflows into cash/bonds look extreme. The US Economic Policy Uncertainty Index also remains elevated (trade, tariffs, China, Iran, etc.), which historically and surprisingly is consistent with above average forward returns. Thus, as we manage client portfolios, we first pursue client investment objectives (stock/bond mix) while second, being mindful that a policy mistake could end the longest running Bull market and economic expansion in US history. We expect the current bull market and economic expansion can advance further; a resolution in tariff/trade talk should provide further support for advances.

When markets action turns ugly, is “selling everything” appropriate? When client portfolio values drop because of a “rainy day” in the stock market, some desire to “sell everything.” This is referred to as “loss aversion sentiment.” Investors simply don’t like big losses. Investors should always recall: 1) Investment objectives, if correctly established before starting to invest are to aid achieving long-term plans. 2) All client portfolios own “buckets of time” assets, wherein MMF/bonds will dampen a stock market “rainy day” and allow one to weather the time without making emotional wrong decisions (selling when the market is down and locking in lower values); “buckets of time” assets provide portfolio and financial flexibility. 3) History reveals that stocks beat bonds, often and by a lot; thus a long-term investor must “weather rainy days” that occur in every asset class. Timing the market never works, as reinvesting (after selling) is very difficult and the loss of recovery value is great.

Should my investment portfolio own passive (index) funds; less active managed funds? [“Fun” question!] Index funds can be appropriate to include in client portfolios – they offer good tax control, often lower fund operating expenses, quick diversification, and are usually easily sold. We utilize some passive with active funds in client portfolios. We seek active first, because a selected fund demonstrated strong historical performance via executing a repeatable investment process/discipline. An active fund operating expense ratio is important, and we seek as low and reasonable compared to peers, as possible; historical tax efficiency is also important. A passive (index) fund may be utilized to achieve greater tax efficiency, and when a similar active fund strategy is not currently available. It is important to understand that passive strategies capture all the up and down of the market sector or index being replicated. Active strategies by contrast generally display favorable down market capture and drawdown protection. Passive and active fund strategies can be owned together, and have a place in client portfolios.

How much taxes (how many exemptions) should be withheld from my pay (retirement) check? Please be aware that Nvest employees are not CPA tax advisors; we understand many aspects of taxes and can offer thoughts. Tax withholdings seem complex, particularly because of recent tax reform. But determining withholdings is not too difficult. Rather than trying to determine 3, 4 or more “exemptions” to claim on your W2 tax withholding form, consider specifying a dollar amount of tax to be withheld as an “override.” To derive the dollar tax override review an IRS federal tax table to determine your individual or married (filing jointly) tax bracket and apply that percentage to the adjusted (annualized) total gross income less your standard or itemized deduction. The process is more likely to result in withholdings that more closely match your actual tax liability. Please reach out to us for additional detail on how to work through what is a relatively straightforward override calculation.

What a deal! The first recipient of a monthly Social Security benefit in January 1940 was 65-year old Ida May Fuller of Vermont. Did you see/read this story? During 3 years before Fuller retired, she paid $24.75 in payroll taxes (in total, not per year). Fuller lived another 35 years before dying at age 100 in 1975. During her retirement, Social Security paid Fuller $22,889 in retirement benefits. In other words, she received $925 for every $1 she paid into the program (source: Social Security).

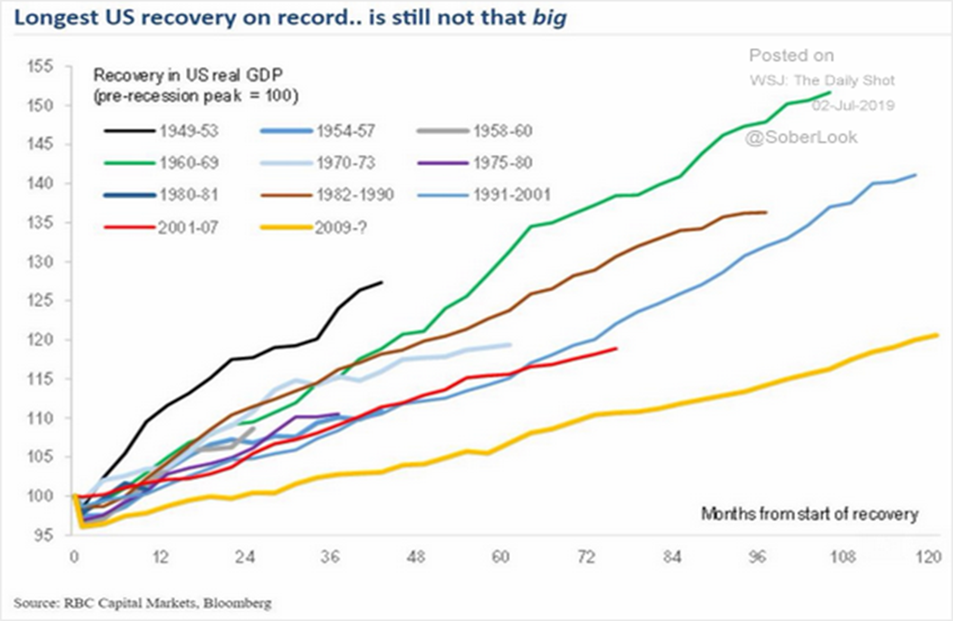

Economic Recovery/Expansion in context:

As shown to the right, the current economic expansion (yellow line), just became the longest in US history. Unfortunately, the pace of growth is the slowest.

If trade/tariff talks resolve, the economic expansion can easily run longer barring no other policy mistakes.