On July 20, 1969, American astronaut Neil Armstrong became the first person to walk on the moon when he stepped out of Apollo 11 in an area called the ‘Sea of Tranquility’. Scientists suggest that the force of gravity is 5 to 6 times weaker on the moon than here on earth. Would that make you feel like you were almost floating as you walk or run? By contrast, Bill recently enjoyed a bicycling trip in Nova Scotia, Canada. He shared that on several days the force of gravity was very much on his mind as the route often felt like a never-ending climb. More than half the group riders opted for e-bikes, or bikes that are assisted by an electronic motor. When climbs occurred, those on e-bikes used “turbo-assist” to zoom by with ease. This experience is a lot like investing – gradual ups, then downs; some rises were fast and steep followed by a fall. [On a bike, the rise was work, and ride down was fun; in financial market, the rise is work and declines are frustrating.] We generally don’t think about gravity; we take it for granted unless falling out of bed. Nevertheless, it does act on everything, unlike being on the moon.

Research firm Strategas presented this “gravity” concept on several occasions during the last 12 months. For investors, both money and energy prices are forces that can be related to gravity. Businesses and consumers need and use both money and energy. During much of the past decade, both items were relatively cheap, allowing financial assets to leap with ease. Since mid-2022, the cost or price of both money (interest rates) and energy is up significantly, adding weight and/or economic pressure. Interest rates are akin to the force of gravity (in the physical world), giving weight to financial market valuations.

Generally, when interest rates (and energy prices) are low, valuations of stocks expand and even soar. Vice versa, when rates rise or stay high, stock valuations tend to fall/decline. Much of this year seems to be defying gravity. While interest rates and energy costs remained elevated over the summer (June and July), stocks appeared to be wearing moon boots, leaping higher with little weight. The investing community appeared to buy into the idea that with employment strong and company earnings better than expected, a soft economic landing (instead of recession) might still be possible. What a difference a couple weeks can make. On August 1, Fitch Ratings downgraded the US’ credit rating because the trajectory of US debt is worrisome. Too little action by policymakers to address both spending and tax revenues is problematic. Adding new debt at the same time maturing government debt needs to be refinanced at higher interest rates is not good fiscal management. The rating downgrade plus rising trend of interest rates, sparked a quick adjustment higher on US government bond yields. The US 10-year Treasury bond yield increased roughly 35bps to a high of 4.34% on August 21 (recent peak). This change may not seem like much, but it represents a 9% increase in the cost of money from the rate in late-July. At the same time, oil prices jumped more than 15% since June. Sensing renewed economic pressure, the S&P500 dropped -4.75% during the first three weeks of August. The final week of August provided market relief because a few economic stats reflected new economic strain. Investors/markets took signs of economic strain as a “hope” the Fed will not pursue additional interest rate increases. Bond yields hold the key to an emotional market that can change quickly.

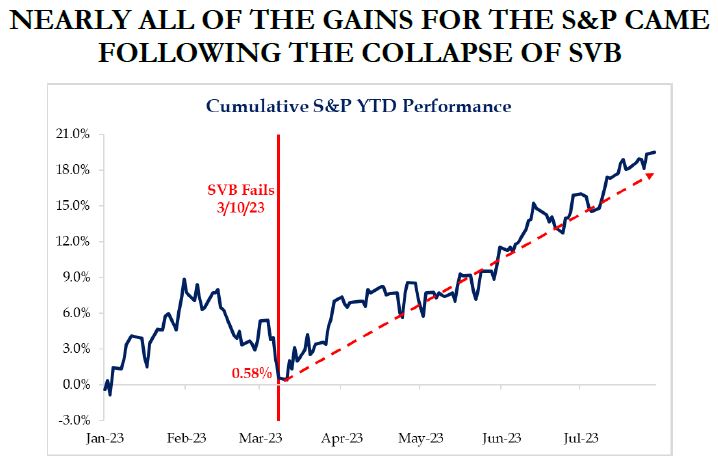

YTD performance is surprising to all participants in light of many distracting events. We are generally encouraged by the YTD returns, but also “feel” frustration, particularly with the narrowness of the advance. Almost 76% of the +17%+ YTD return for the S&P500 Index was produced by just 10 stocks (with most occurring since the failure of Silicon Valley Bank in March).  There is a disconnect between indexes like the S&P500 and Nasdaq, versus returns from a larger number of stocks. The stock market is in transition. Client portfolios, which are more diversified, generally trail performance of indexes that are heavily exposed to a few names (cap weighted). We maintain conviction that the forces of economic gravity – focusing on attractive valued fund strategies – will provide benefit long term with less risk. Expensively valued companies are “priced to perfection” with little room for error. In a market where momentum is anemic, nothing (sector or stocks) is untouchable or sacred.

There is a disconnect between indexes like the S&P500 and Nasdaq, versus returns from a larger number of stocks. The stock market is in transition. Client portfolios, which are more diversified, generally trail performance of indexes that are heavily exposed to a few names (cap weighted). We maintain conviction that the forces of economic gravity – focusing on attractive valued fund strategies – will provide benefit long term with less risk. Expensively valued companies are “priced to perfection” with little room for error. In a market where momentum is anemic, nothing (sector or stocks) is untouchable or sacred.

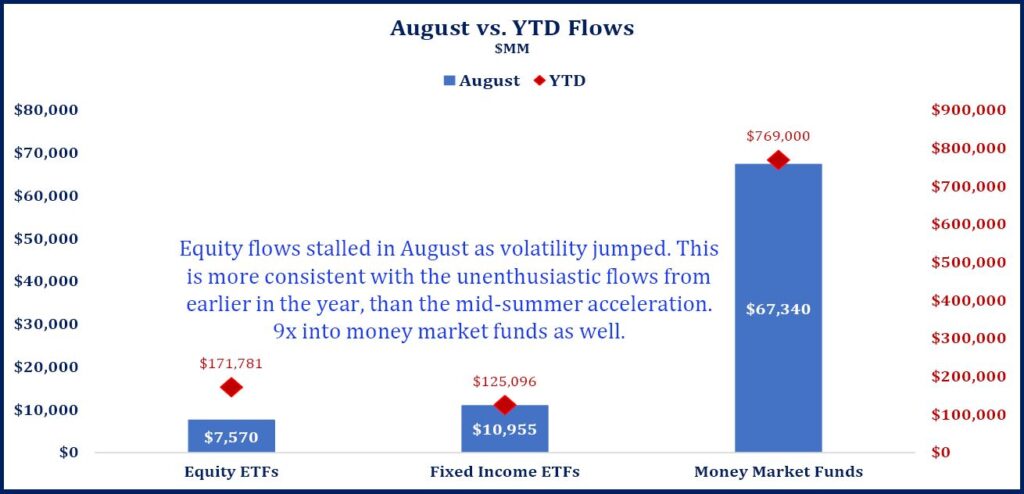

Also interesting: did you know that money flows in August and YTD heavily skewed toward “cash and quality (“risk off”)? Flows into stock funds stalled in August as volatility jumped. Many investors consider yields on many money market funds (paying near 5%) more attractive than low-yielding bank accounts. Their reasoning, “why own risk assets when MMFs provide current attractive yields?” It’s nice to be earning yields again for short term monies.

September is often one of the weaker months of the year from a seasonal perspective. It’s also likely that the cost of government borrowing will recapture the spotlight in the weeks ahead; political analysts suggest a government shutdown may occur as we approach October. Congress will need to pass its annual spending bill that will again challenge the recently raised debt ceiling limits in an environment of increasing, high interest expense (now approaching 14% of annual tax revenue). Historically, market participants do not like interest expense consuming so much of revenue. Also, interest rates tend to stay about +2% higher than CPI inflation. That means current 5% yields high quality money market funds and short-term bonds are likely to remain high for longer. Even as inflation is much lower than a year ago, it too travels in waves – up; down; and will probably rise/fall before settling closer to historical 3% levels. Government policies influence inflation and interest rates, which influences other assets valuation.

Investors should not ignore the laws of economic physics. We strive to keep the concept of “gravity” in focus as we invest client portfolios. While it may feel unsettling in the short-term, history shares that pursing valuation disciplines will lead to growing portfolio values over time. The gravitation pull of higher interest rates and energy prices will likely curb a “moonwalk bounce in the step” of high priced, speculative areas.

By Steve Henderly, CFA | Nvest Wealth Strategies, Inc.

Click here for the Printer-Friendly PDF version of “Moonwalking No More – Sept23”