Might Could

“Might could” is a southern way of saying “might.” It refers to a possible willingness or ability to do something. Grammatical “experts” claim you cannot link two verbs – “might” and “could” – next to each other unless one is a linking verb. “Might” is informal and used with less likely events (“May” is formal and used relating to actions more likely to happen). “Could” is used to express ability and often refers to past actions. How about a few more southern phrases…”I’m fixin’ to”; or “pitchin’ a fit”; “more than one way to skin a cat”; “you could drive a preacher to drink”; or “as all get out.” [Special thanks to our own Diane Carpenter, Client Concierge, for recently sharing about “might could”; that’s often how commentary titles arise!]

“Might could” may be a good way to respond to someone attempting to predict future market returns and the economic path. Predicting the future for the balance of 2023 or into 2024 and beyond is challenging. Starting 2023, very few would predict that the S&P500 would rise +20.5% or the NASDAQ index with a lot of tech names would jump over +44%… by the end of July! But saying it “might could” is appropriate. The month of July continued to boost client portfolio values and returns. In general, “risk-on” sentiment continued to prevail across assets. Beginning 2023, and 7 months later, it’s easy to feel uncertain about future returns. But, it “might could” go up, pause, or retreat some. It just “might could.” The key is being a long term investor.

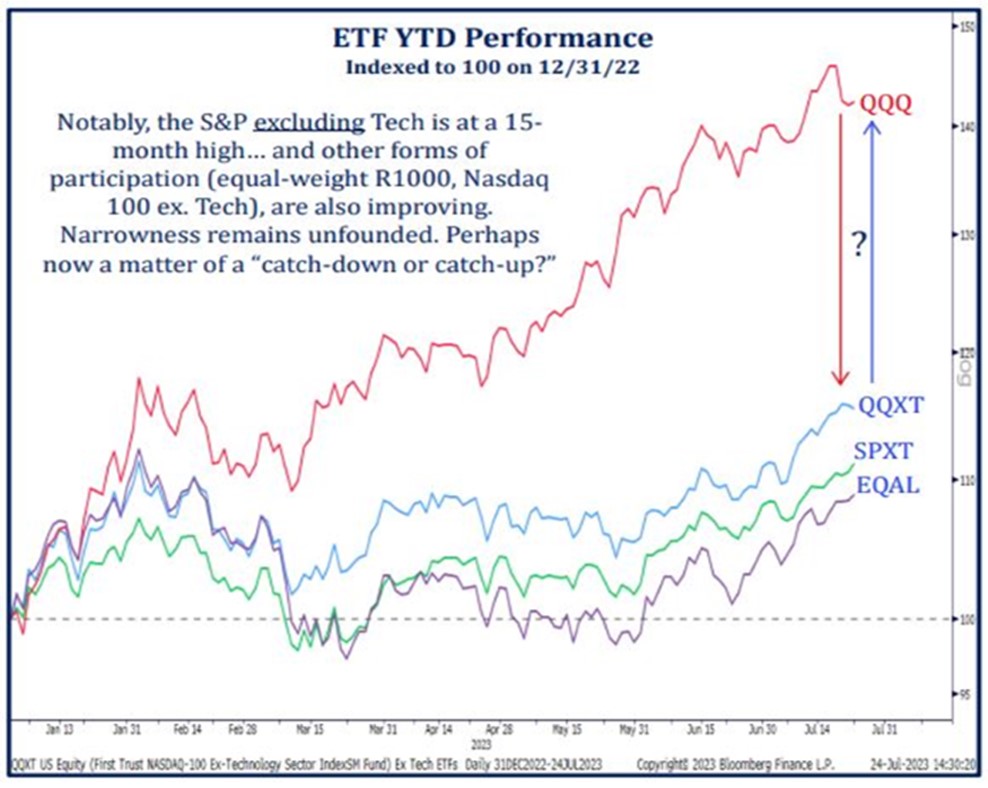

Encouragement should exist with these monthly and YTD returns. Yet, we do attempt to overlay results and future expectations from a valuation perspective. First, many stock market participants are puzzled by the narrowness of stock returns during the 1H2023, where the “magnificent seven” tech names led the charge. Noting the performance for the YTD, the QQQ (NASDAQ index) owns the “magnificent seven” stocks. If these tech stocks are carved out, the resulting performance is graphed by QQXT; the S&P500 without tech (SPXT), and  the equal weighted S&P500 index (EQAL). The takeaway is the narrowness of the recent market advance. If not for the performance of 10 stocks generating 70%+ of the 1H return, the other names were non-contributors. In general, the stock market has components that look very expensive. Second, IF the economy remains soft because higher interest rates slow down consumer buying, that bodes for careful investing tactics. High interest rates, contracting money supply (M2), student loan repayments due to resume, together suggest a slow growth economy “might could” occur. And, that suggests a soft stock market return outlook.

the equal weighted S&P500 index (EQAL). The takeaway is the narrowness of the recent market advance. If not for the performance of 10 stocks generating 70%+ of the 1H return, the other names were non-contributors. In general, the stock market has components that look very expensive. Second, IF the economy remains soft because higher interest rates slow down consumer buying, that bodes for careful investing tactics. High interest rates, contracting money supply (M2), student loan repayments due to resume, together suggest a slow growth economy “might could” occur. And, that suggests a soft stock market return outlook.

So…will the markets continue their advance in 2023 and into 2024? Always a tough question. We do not use a crystal ball but it “might could”. What should long term investors do; what are we doing with this investment backdrop? Glad you asked. These conditions suggest pursuing a “slow-walk” path for portfolio growth. Owning bonds (of short and intermediate maturity) provide yield not available over the last 10+ years; and bonds provide diversification benefits. Along this path investing in mutual funds and ETFs that focus on better quality companies – less debt, and with dividend income – is appropriate. The common “theme” is seeking dividend and interest income during uncertain times. It’s the “tortoise and hare” concept. Keep earning returns even if the environment looks soft. Because, the historical trend of market returns DO support a long term winning strategy!

Mission NOT Accomplished

Just one year ago, reported inflation topped 9.1%. At the same time, 10-year Treasury yields were 3.07%; some -600 basis points lower than the inflation rate (CPI). That was the peak spread between inflation and bond yields. Today, reported CPI is nearing 3% and the 10-year Treasury yields roughly 4%. For the first time in more than a decade, bond yields are higher than CPI rates (referred to as “positive real rates”). Both inflation and bond rates are lower than their peak. But we should understand that declining from peak inflation does not mean mission accomplished.

While rates seem high relative to recent years, the yield on 10-year Treasury bonds exceeded or was higher than inflation rates more than 80% of the trading days since 1960. Current 10-year yields are now above the CPI rate. Typically peak bond yields occur about 6 to 9 months after peak inflation.

What does this mean for investing and portfolio management? Three things: 1) Nice to be earning a yield on bonds again (for the past 10 years, the Fed’s zero interest rate policy kept interest rates sub-normally low); 2) As interest rates may too be peaking, owning intermediate maturity (5-10 year) bond exposure should prove rewarding; and 3) Bonds provide better diversification benefits to stocks, like historically the case. In general, because interest rates are up, bond prices are “discounted” and offer good value. If interest rates are near their peak for this cycle, the return path for bonds is more certain and less variable than that for stocks.

Some components of inflation are very sticky – rents/housing and food prices. Agg-Inflation, or inflation on food items is anticipated to remain sticky; an ongoing inflation item. If inflation remains sticky and economic growth is slow (not recession), the Fed could remain active by further raising interest rates, and/or hold them high for longer.

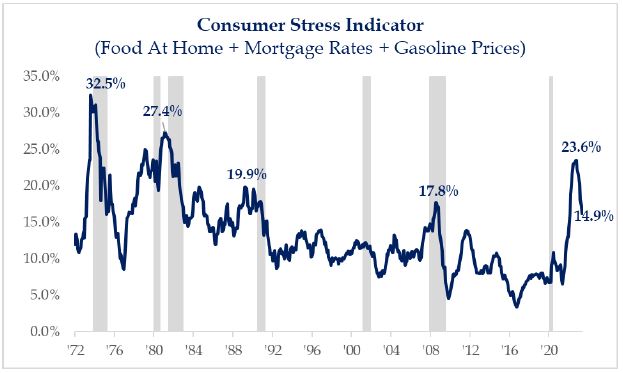

Another (last) interesting thought…, market performance in July seems to suggest the consensus idea of a recession is no longer so certain. We sh ared about the Consumer Stress Indicator (see chart); it moved to its lowest level since January 2022, now sitting at 14.9% down from its high of 23.6%. And, while the Consumer Stress Indicator is improved, the reading is still elevated.

ared about the Consumer Stress Indicator (see chart); it moved to its lowest level since January 2022, now sitting at 14.9% down from its high of 23.6%. And, while the Consumer Stress Indicator is improved, the reading is still elevated.

Thus, the question remains – is the Fed nearing the end of its tight monetary policy (to fight inflation), even if they are likely to remain tight and hold rates high for longer? A good number of investors are concluding, IF the Fed is nearly done and no recession occurs, then stock markets should perform better. This recent idea is providing support to the stock market even if economic growth prospects look slow. The Fed likely believes it is early to say “mission accomplished.”

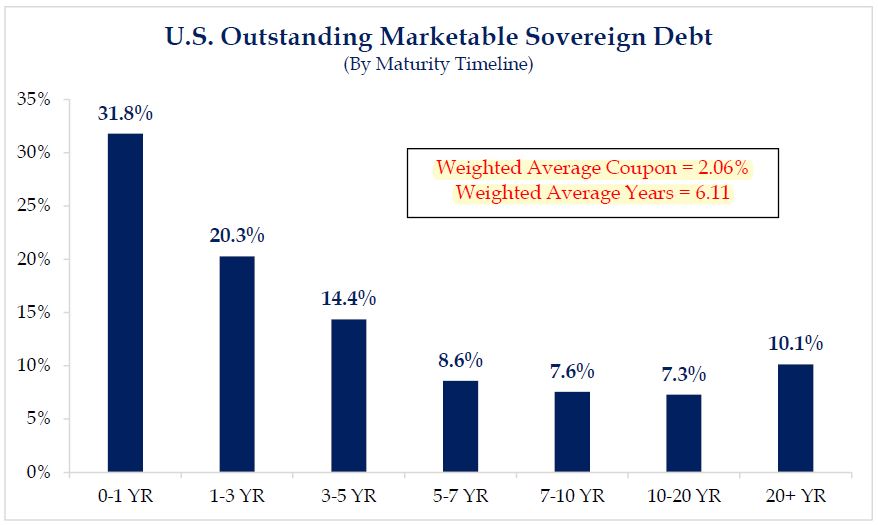

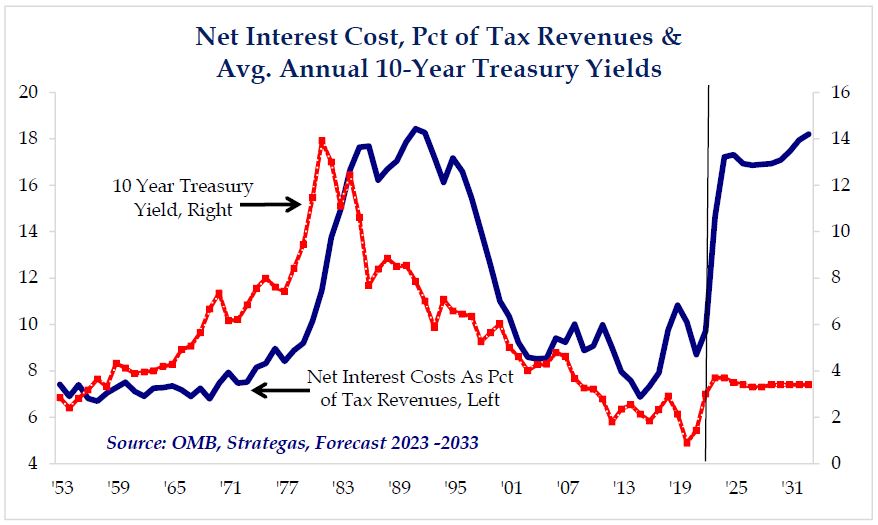

News “flash” from August 1st –Fitch Ratings downgraded US Treasury issues from AAA (highest) to AA+. They stated that the growth of government spending AND with the issuance of so much additional debt is becoming too much. And, they expressed concern about the government’s addressing the issue. Was their statement a proxy for the market’s perspective? Will bond vigilantes, as in the past, raise alarms when debt levels are deemed too great and no meaningful steps appear to right size it; will they put pressure on the government to “wake-up?” The majority of US outstanding debt (over 52%) is due to mature in 3 years or less; almost 67% matures in 5 years or less. The average interest rate on all US debt is 2.06%. With rates currently near 4%, the interest expense for the USA is due to rise quickly as these maturing bonds are refinanced. It seems shortsighted too, that most US financing was and continues to be issued in the short maturity area where rates are highest, than issuing longer dated bonds at lower rates, even as liabilities are mostly long-term? Currently, the net interest costs for all US issued debt consumes over 14% of the annual tax revenue the US Treasury receives. In the 1980s when this 14% threshold was last reached, market vigilantes levied austerity pressure on US policymakers. Related, for the first time in 35 years the US net interest cost is rising, with the debt-to-GDP ratio over 120%. What does this mean?…”surprises often break/occur in the direction of the underlying trend.” When market trends are struggling for direction, it seems more bad news endorses the trend (another recent example was bank failures in March); and vice versa. When market trends are advancing, surprising news supports the existing trend. It means, invest carefully with a conservative focus because the recent trend still exists.

Charts sourced from Strategas

Click here for the Printer-Friendly PDF version of “Mission NOT Accomplished” – Aug23