Happy New Year! 2021 provided a second, actually a third, consecutive year of double-digit investment returns for stocks (most forget 2019 because of how quickly the mood soured in early 2020).

This edition of our quarterly newsletter, Nvest Nsignts provides “the lowdown” on what themes drove the financial markets during 2021. Perhaps of greater interest is our sharing of what we believe will be the biggest focus for investors as we “Journey into 2022“. Our personal finance focus this quarter, “Healthy Habits” shares several easy-to-implement “resolutions” that can pack a powerful punch to enhance your long-term financial posture as you set plans for the New Year.

A printer-friendly version of the full quarterly newsletter, including benchmarking and fund performance data, can be obtained here: Q4 Nvest Nsights

As always, please do not hesitate to let us know if you have any questions or would like to coordinate a time to visit.

LOWDOWN ON 2021

2021 provided a second, actually a third consecutive year of double-digit positive investment returns for stocks. Most forget that the S&P500 jumped +31.5% in 2019 because of the shocking peak-to-trough drawdown of -34% in 1Q2020 as the magnitude of COVID to the economy weighed on financial markets; yet 2020 (full year) advanced +18.2%. For 2021, the S&P500 advanced +28.6%. In the 21-months since the March 23, 2020 low, this young bull market return grew to almost +120%. This new bull market was powered by gigantic fiscal and monetary stimulus that the economy was/is unable to fully use to finance its growth, but it powered asset prices skyward. This stimulus is also in part responsible for the hotter inflation being experienced. Investors would not want to miss this market journey; and attempting to time the market would be a near impossible strategy (if you got the COVID story right, you probably got the market call wrong). For those that wanted to deploy new money last year, a keenly involved investor understands the 2021 advance was also a story of challenge. The greatest pullback was only -5% which never allowed anyone the opportunity to invest at lower values.

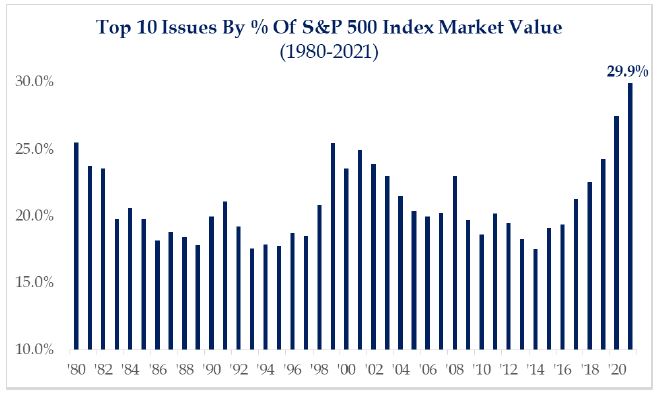

Further and perhaps more important, a different performance story existed under the surface. Very few stock investments (mutual funds, ETFs or individual names) finished as strong as the S&P500 index, other than 5 or 10 BIG companies that produced the oomph. Those few names really powered the S&P500 to its final new market highs (total of 70 for the year) as the last quarter of the year concluded. The top 10 names comprise nearly 30% of the overall index making it more top-heavy than ever (historical average is closer to 21%; Apple is the single-issue largest weight of 7%). The average stock is down -13% to -20% over the past few months, while the index is making new highs. Momentum really faded from the start to the end of the year.  Stating it differently… ending 2021 was very different than it began. Beginning the year, more than 90% of S&P500 stocks were continuing in an uptrend, trading above their 200-day moving average. That’s most everything performing quite strongly. As we start 2022, roughly 74% (was 65% on 12/5) of stocks in the index were trading above the 200-day moving average trend line. That is still a strong reading, but also testimony that the mood of investors is changing. As reference, when the market hit its low on March 23, 2020 (start of the current new bull market), when most everyone felt bewildered, only about 5% of S&P500 stocks traded above their 200-day moving average.

Stating it differently… ending 2021 was very different than it began. Beginning the year, more than 90% of S&P500 stocks were continuing in an uptrend, trading above their 200-day moving average. That’s most everything performing quite strongly. As we start 2022, roughly 74% (was 65% on 12/5) of stocks in the index were trading above the 200-day moving average trend line. That is still a strong reading, but also testimony that the mood of investors is changing. As reference, when the market hit its low on March 23, 2020 (start of the current new bull market), when most everyone felt bewildered, only about 5% of S&P500 stocks traded above their 200-day moving average.

Recall, no client portfolio owns the S&P500 for many valid reasons – the key being risk. Stock allocations include large-cap (S&P500 exposure), mid- and small-cap (size) company stocks, and foreign. Plus, each cap-size incorporates both value and growth-style disciplines pursued by the various no-load mutual funds or ETFs. Diversification is a key/core principle to managing risk. Looking at the performance of the general stock allocation compared to the S&P500 reveals an underperformance (for market-action reasons cited above). Encouraging though, the tactical strategy employed since the market low is generating positive alpha above a static benchmark for each client investment objective – see Benchmark page. Each benchmark includes static exposure to both bonds and stocks (domestic and foreign). Our tactical strategy employed in client portfolios attempts to slightly adjust exposures based upon valuation and risk characteristics. Valuations and risk rise together. Managing risk involves awareness to valuation – buying low (cheaper valuation with less risk) and selling (rebalancing) at high valuations and risk. An example in simple terms – US/domestic stock valuations are high compared to many other global/world markets. Our focus is to keep advancing you toward your “LIVING LIFE” financial plan goals.

We expect 2022 to continue the new bull market advance, albeit at a slower and more choppy pace. It will be critical to not get distracted by market volatility, even a market correction, while pursuing a long term investor focus.

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

JOURNEY INTO 2022

In John Eldredge’s little book “Epic”, he writes that “life does not come like a math problem which can be solved by plugging numbers into an equation to get an answer. Rather, life is like a story – waking up each day in the middle of this journey that is sometimes wonderful, sometimes awful, usually a confusing mixture of both, and we may be without a clue how to make sense of it all. The plot may thicken as we don’t know how a day, a month, or the year may end. We must live one day at a time.” So too is a new year – viewed as the end of one chapter and often considered the beginning of another. A better metaphor is describing life being a journey – a path or road trip along life’s journey. There is a beginning for every journey, even an opportunity to start again. Each of us also experience our own individual investment and financial journey. There was a beginning which continues over our entire lives. The investment journey in 2022 will evolve; it will be different than guesses offered at its start. As we begin 2022, let’s suggest what the path could look like, keeping in mind our “flash light” is somewhat dim or unable to shine ahead very well.

We begin 2022 with a different market tone than last year.

- It’s all about rates. Low interest rates and lots of excess money sloshing around in the financial system neutralized index volatility last year; volatility will likely be different in 2022 as the Fed and other central banks raise interest rates and tighten monetary policy to combat rising inflation. Excess money in the financial system is being consumed; not much new will be added. So, 2022 change will occur because of a shift on the monetary policy front – “quantitative tightening”; it will be reflected first by watching the bond market (rates rise), which then creates stock market reaction. Key – monetary policy changes should proceed with care (not speed, which could kill the economy and market).

- “Washington, we have a problem.” Inflation surge, the highest in 39 years, is stickier and longer lasting than Fed/central bankers desire due to supply chain and delivery bottlenecks that will gradually ease. “Transitory” needs defining. Because inflation is proving sticky, it means longer than 1 year, maybe 3 to 5 years depending on how shortages (labor, products, etc.) return to “normal.” In any case, inflation is the “Grinch” that steals. We are likely at “peak bottleneck” which should lead to “peak inflation”, but the Omicron variant may create a small setback.

- Earnings that power stock prices higher should grow at slower rates than 2021. That suggests existing valuations should not expand but could contract. Analysts expect earnings to be softer in 2022. Yet, could estimates prove understated if/as inflation remains sticky and companies raise product and service prices; albeit still growing slower than during 2021? The economy can handle a continued short disruption in demand due to bottlenecks; it also has access to sufficient cash to finance growth; and there is a remedy (vaccination) to the problem (COVID virus and variants) to avoid another Great Lockdown. Key – bringing the health “emergency” to an end and moving life and business activity more normal. This would be especially helpful to foreign vs. domestic investment performance.

- Government policy influencers are present. Midterm election years bring about stock market volatility and buying opportunities (as markets pause/correct); wave elections – voters removed the party in power in 8 of the last 9 elections. State governments’ cash coffers are full and even overflowing which could lead to opening their fiscal spigots. “Build Back Better” shrinks in size and seeks to do fewer things better. New regulations on climate change, banks, and big technology are like dark clouds affecting the outlook. Could there occur regulation over legislation? Might Putin (Russia) and Xi (China) press their “bets” against a polarized and frozen western world; at the same time North Korea and Iran press their threats on nuclear and higher oil prices? Key – there are many political “fireflies” that could stir at any time to create new market worry.

What does all this mean; how should investors approach 2022? We believe the tactical strategy implemented coming out of March 2020 remains valid – smaller-size company stocks perform best against inflation; value will be resilient over growth amid rising interest rates and stickier inflation.

Were you ever on a plane near dusk? Recall looking out the window toward the west revealing a beautiful sunset; looking out the east window reveals the blackness of night? One side is beautiful; the other is dark. In either case, the path of the plane is still toward its destination; it’s still the journey. Similar too with investing. It’s all about the path, the journey while staying focused on the destination. Stay on the path. It’s rarely easy moving from early-cycle with big ups to mid-cycle in a bull market. That’s because as we are near/at full employment, returns get more sloppy and volatile. We cannot grab hold of the future if we keep holding on to the past, or being distracted by prospective transitory worries. Look forward, not backward. Investing for a life time, even a short time interval, requires identifying your purpose (for the monies) and time horizon. Then invest pursuant to these key markers.

“Life is a story, in volumes three – the past, the present, and the yet to be. The first is finished and laid away. The second we’re reading day by day. The third and last, volume 3 is locked from sight until eternity.” What we lived, we cannot undo; the past is over. Volume 2 is today’s path along the journey. So keep moving along the path, and keep writing your today.

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

CHARTS FOR THOUGHT…

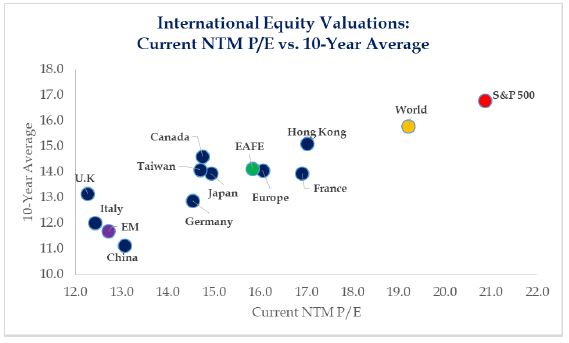

U.S. Expensive Compared to International

The S&P500 remains one of the most expensive global markets. It is no secret that international equities are a relative bargain, but what can be the catalyst for their outperformance? We wonder if a weakening US dollar, AND weaker covid variants which cause foreign governments to finally abandon the idea that rolling lockdowns are an effective or appropriate mitigation strategy, keeping their economic recoveries going, may occur in 2022.

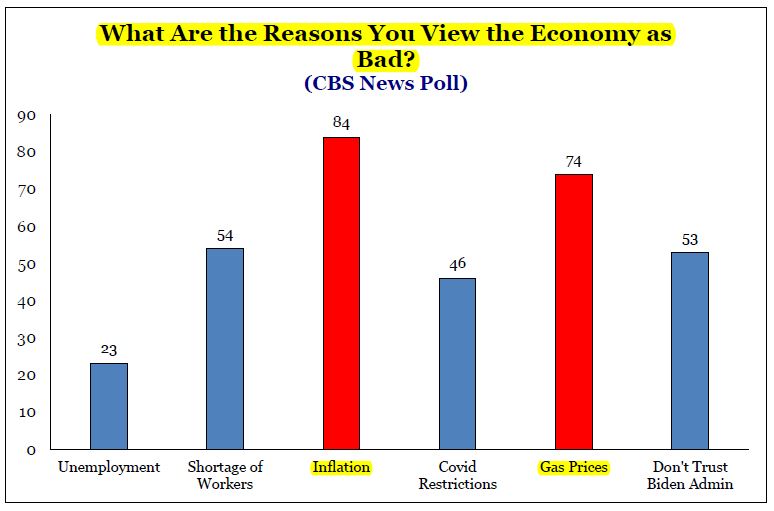

CBS News polls consumers on what is most problematic with the economy…

…

…