After nearly two years of strong market gains, investors experienced their first meaningful pullback during the first quarter of 2022. While it is typical for markets to experience pullbacks and a higher level of volatility after the initial 12-18 months of a new bull market, it is never welcomed or comfortable. That is probably because the uncertainties that usually accompany them are always unique. Present uncertainties include a still fractured global supply chain, a Federal Reserve that finds itself needing to raise interest rates and tighten monetary policy in pursuit of arresting inflation that is running at the hottest pace in 40 years; and of course Russia/Ukraine which muddies both challenges further.

This quarter our Nvest Nsights newsletter shares what we’re watching and perspective to the topics/questions we’re most frequently hearing from clients. Perhaps it “Goes Without Saying” that the backdrop highlighted above implies 2022 will likely remain a challenging year; but there are also some important messages to be heeded from history. There is also the saying that “A stitch in time saves nine”; while ‘main street’ consumers may not welcome rising interest rates and the impact on the cost of borrowing (or the markets in the short term) it is nonetheless appropriate for the longer-term health of the economy. The markets are adjusting to a changing investment landscape. We close the update with our personal finance theme article with a change coming to employer 401k statements this year. Will the new “Lifetime Income Estimates“ being provided help you feel more secure?

A printer-friendly version of the full quarterly newsletter, including benchmarking and fund performance data, can be obtained here: Q1 Nvest Nsights

As always, please do not hesitate to let us know if you have any questions or would like to coordinate a time to visit.

GOES WITHOUT SAYING

“It goes without saying.” This phrase refers to something that is so obvious that it doesn’t need to be mentioned or explained. For example, it goes without saying that most people look forward to their vacation days from work. Who doesn’t like a vacation?

Following almost two years (21 months to be exact) of strong market rise since the Bear market low on March 23, 2020, investors experienced their first meaningful pullback (>5%) during 1Q2022. The S&P500 finished the quarter with a -4.9% decline; the average stock fund lost -6.2% and many individual stocks lost near -20%. Even the average bond fund – deemed the “safe” investment – recorded its worst quarter in 40 years evaporating -4.1% (while the Barclays Bond Index lost -5.9%). At mid-March, the correction in the stock index was -12.7% from its last high achieved on January 3. A rebound during the last 2 weeks of March narrowed the quarter decline, likely providing some encouragement (we are skeptical of the durability; the rebound is fragile). It’s appropriate to use care when investing during a period in which the Fed has little choice but to tighten monetary policy, especially if their path is quick and aggressive. Inflation and oil are creating that challenge in 2022. For seasoned investors, it goes without saying that stubbornly high inflation accompanied by higher interest rates makes it likely that valuations for bonds, stocks and real estate will display volatility; they will likely adjust lower in the short term.

1Q portfolio performance followed the market path – lower for both stocks and bonds. Only exposure to energy (or commodities) provided positive return relief, acting as inflation hedges to persisting economic supply chain issues. Investors are showing signs of worry and confusion regarding the prospects for the future. Many clients are asking questions about inflation and market action.

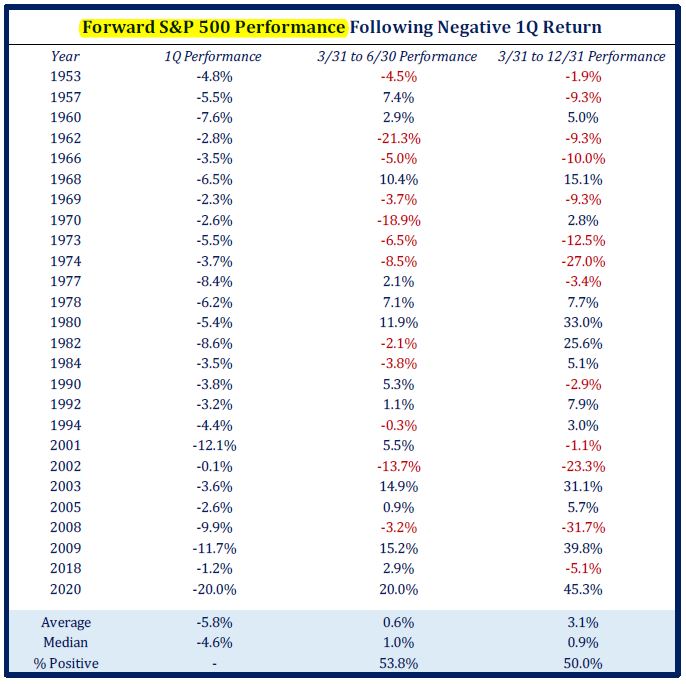

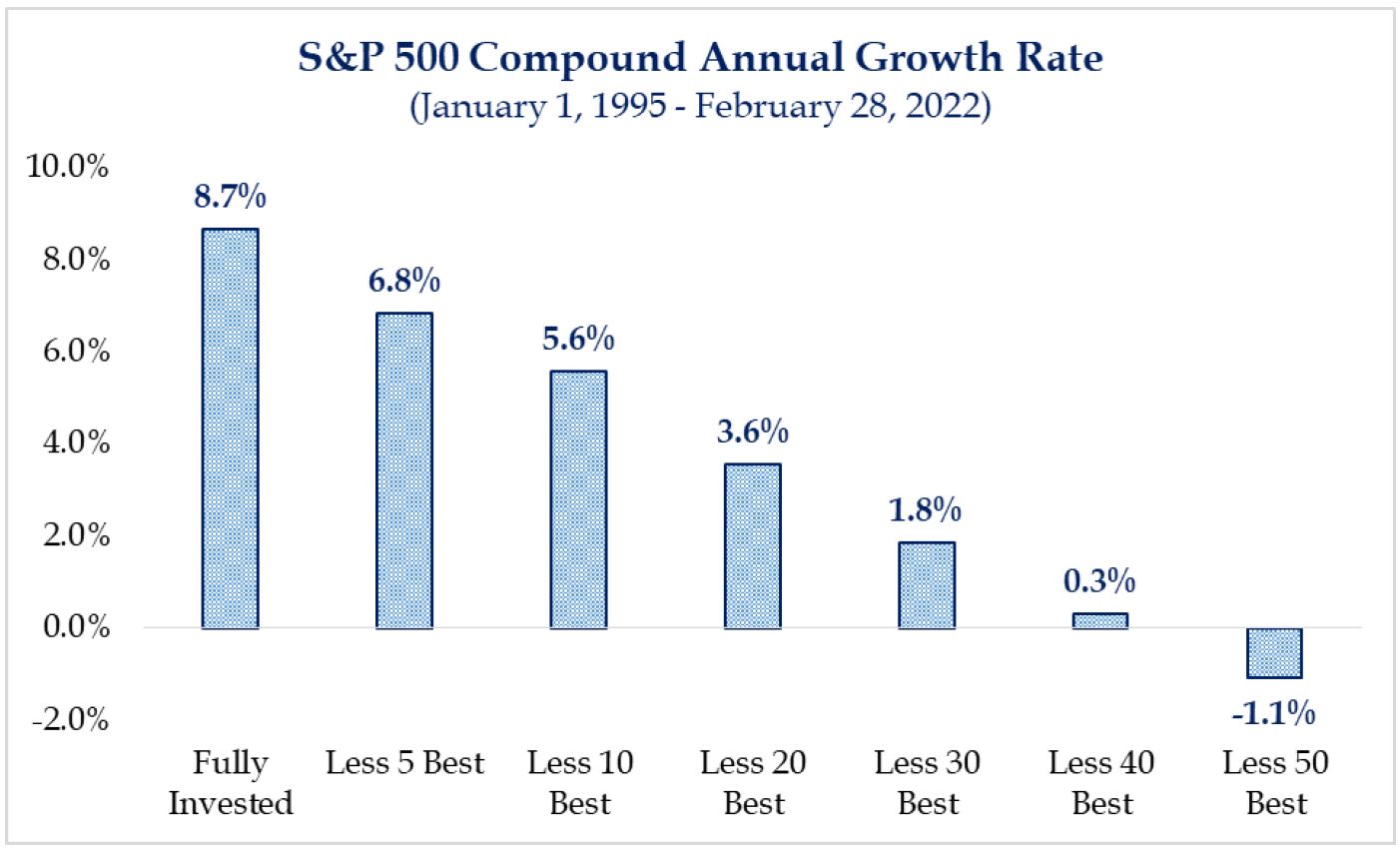

History provides perspective about future performance of stocks following negative 1Q returns. Looking at 26 years where the 1Q generated a negative stock return, the next 3 months provided a small +0.6% average advance higher; that was 54% of the time. Further, forward returns for the remaining 9 months of the year (after 1Q), produced a +3.1% return on average, 50% of the time. In other words, returns during the balance of a year where the 1Q was negative foretell an unexciting near-term return experience.  One additional important thought… even if the balance of 2022 proves uninspiring while global risks appear many, investors should not step away. It’s all about “Time IN the Market” rather than timing the market. Consider this: investors remaining fully invested enjoy stock returns of nearly +9% which is +1.9% higher than missing the 5 best days. Average annual returns are worse by -3.1% if 10 best days were missed; and -5% if missing the 20 best trading days. Historically, many of the market’s strongest days occur in close proximity to market lows and heightened uncertainty. Recall the start of this new Bull market run: missing the first 3 trading days after the March 23, 2020 market bottom (states were just starting the Great Lockdown related to COVID and the Fed/government was not yet implementing the flood of monetary stimulus), resulted in missing a +15% jump higher by the S&P500 index. By April 8, 2020 the S&P500 recovered +23%; that’s just 12 trading days off the low. Wow!! The challenge when hitting pause is missing the beginning of the rebound. Emotion leads to timing; and timing leads to poor performance experiences.

One additional important thought… even if the balance of 2022 proves uninspiring while global risks appear many, investors should not step away. It’s all about “Time IN the Market” rather than timing the market. Consider this: investors remaining fully invested enjoy stock returns of nearly +9% which is +1.9% higher than missing the 5 best days. Average annual returns are worse by -3.1% if 10 best days were missed; and -5% if missing the 20 best trading days. Historically, many of the market’s strongest days occur in close proximity to market lows and heightened uncertainty. Recall the start of this new Bull market run: missing the first 3 trading days after the March 23, 2020 market bottom (states were just starting the Great Lockdown related to COVID and the Fed/government was not yet implementing the flood of monetary stimulus), resulted in missing a +15% jump higher by the S&P500 index. By April 8, 2020 the S&P500 recovered +23%; that’s just 12 trading days off the low. Wow!! The challenge when hitting pause is missing the beginning of the rebound. Emotion leads to timing; and timing leads to poor performance experiences.

We anticipate the market will remain unsettled during 2022. It goes without saying, 2022 is a year of rates – inflation and interest rates. The Fed just started to address inflation with its first interest rate hike. The world will be debating the atrocities of the Russia/Ukraine war. Plus, voters will be sharing opinions about Congress’ and the Administration’s work via the mid-term elections (appearing in market action mid-year). Yes, it goes without saying 2022 will likely be a challenging year for investing. And, it goes without saying that any errors in this work (writing) are my own.

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc

STITCH IN TIME

“A stitch in time saves nine.” A cat has how many lives? Nine! Why 9 in these two well-known sayings? The number 9 has significance to many early cultures. To the Greeks, it represented a magic number and was associated with the gods; believing it took 9 days to fall from heaven to earth. The Egyptians revered cats with the myth that they helped the species disperse around the globe. With “globalization”, so did the myth of multiple lives. Nine is associated with the Chinese dragon, which is a symbol of power. The Welsh used 9 steps to measure legal distances. In Spain, cats were viewed having 7 lives – again a magical number relating to good luck. In any case…“A stitch in time saves nine” is a sewing reference first recorded in a book from 1723. The phrase means it is better to solve a problem immediately to prevent it from becoming bigger. Problems, like Goliath, only get bigger with procrastination.

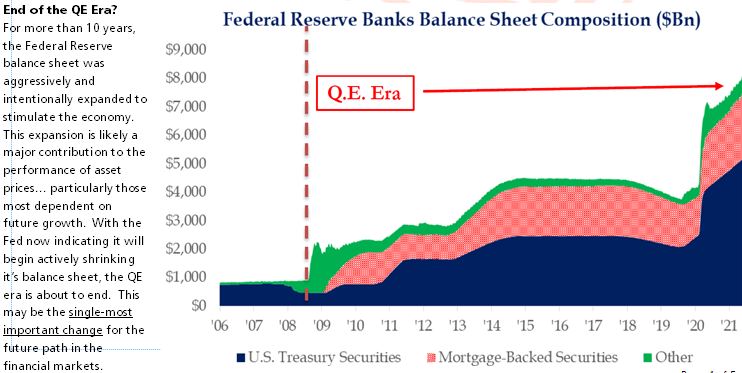

Amazing how 2022 began for the financial markets, so different than 2021. Maybe the last two huge government stimuli, designed to further the recovery following the Great Lockdown of COVID, was too much. Stimuli fertilized inflation. To address mounting issues in 2022, policy change and economic supply chain disruptions are initiating a new era, creating a new backdrop for investing. It’s a turning point. It’s a change by the Federal Reserve from QE (quantitative easing + zero interest rates) to the beginning of QT (rising interest rates + quantitative tightening). 2022 is the year of rates – rising inflation and interest. Together, with several other global worries, market volatility is elevated which creates investor caution and concern. 1Q was a challenge for all investors. The balance of the year is likely to experience continued volatility, and seems likely to generate small returns.

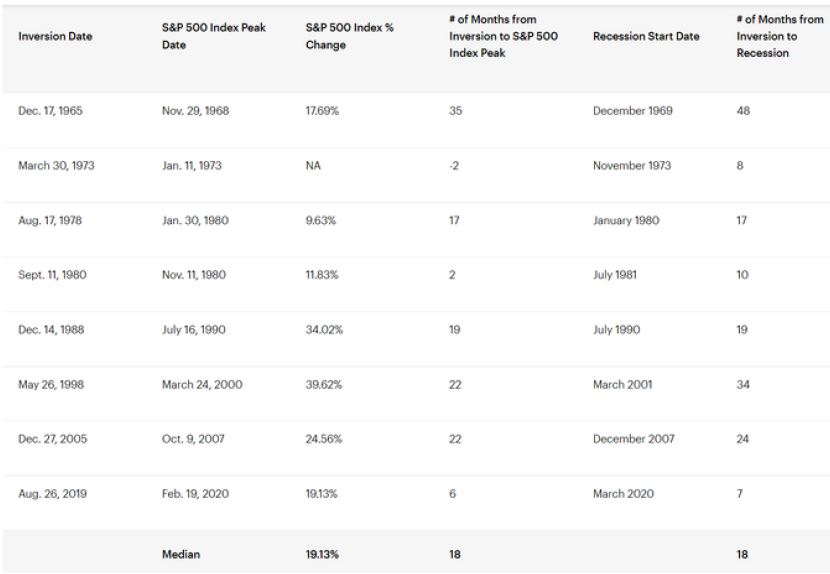

Everyone knows about the many global worries – rising sticky inflation (higher prices for everything including energy) and shortages; Russia/Ukraine war without end in sight; and the Fed’s monetary policy change to tightening. With inflation entering workers’ wages, the Fed is now required to take action. Rising sticky inflation signifies a policy mistake or error. Similarly, an inverted yield curve – where interest rates on short-maturity debts are higher than longer-maturity rates – indicates a policy mistake. Inverted yield curves are not natural. It is unlikely the Fed is making a policy error yet at very low rates (the inversion is positioned at about the 2-year point of the curve, meaning a prospective recession in 2 years; if inversion was at 3 or 6 months on the curve, recession is very near). At present, a recession is not a high probability. Inflation is THE core issue; it’s Goliath requiring a “stitch in time.” Unfortunately, the Fed is deemed to be behind in taking action. Recent market action is sending a message to the Fed – “don’t make a mistake – be careful about how fast (quick) and how much rates are raised.” Something will break – will it be inflation or economic growth? It’s not the first rate increase that hurts, it’s the last. Also the peak rate is not at the start; it occurs later in the rate increase process. History shows that the last rate increase (whenever that is) ultimately causes the weakest financial link in the chain to break. High inflation changes everything. Can sticky inflation be curbed without a recession?

Did you know…History indicates that the economy does not enter a recession without the labor market showing weakness? Currently the US economy is in full-employment position. Unemployment is near a low of 3.6% and the labor force participation rate is still rising, now over 62%. The US labor market is tight, and businesses are scrambling to find qualified workers. Even the average hourly earnings rate rose to +5.6% year-over-year. Technically, labor stats display a “green light” for the Fed to remove easy money policy faster with possible 0.5% rate hikes coming in 2022 (could be market unsettling because its larger than usual and not expected). Investors should closely monitor the actions of the Fed – speed and size of rate increases – to address sticky inflation. The yield curve will tell investor’s perspective of the Fed’s effectiveness. In the early steps of rising interest rates, even when the yield curve first inverts, bull markets do not die. History shares bull markets continue to advance an average of +19% over the next 18 months. Several advances exceeded +30%. Issues that greatly affect the magnitude and duration of the bull market advance are inflation, oil prices and mortgage rates. The “Rule of 10” is interesting – add the price of gas (over $4/gallon) + mortgage interest rates (nearing 5%); when the sum reaches 10 there is often trouble. Currently, the “Rule of 10” for US consumers Is approaching 9. A soft landing is what the Fed is trying to engineer.

One last thought on the dramatics of market change in 2022. Recent action somewhat resembles market events in March 2000 when the tech bubble burst. Understand the time sequence: Low interest rates during the last 2 years and much of the last decade, “financed” recent bull markets higher. Low rates were “rocket fuel” for risky, higher-debt growth stocks including the fast growing FAANG and “click” stocks – elevating them to be overvalued. Last year (2021), value style stocks and funds performed strongly because of the economic recovery, reversing a10-year trend of underperformance. During 1Q2022, investors grew increasingly concerned about inflation – fast rising and sticky – requiring Fed action. In March, the Russia/Ukraine war began, further disrupting commodity supplies. Both bonds and stocks showed their concern with meaningful declines. In stock world, tech and growth stumbled badly; the S&P500 dropped over -12%. “Funny” though, once the Fed initiated its first 0.25% rate increase on March 14, investors seemed relieved. It seemed investors believed, “Finally the Fed is acting to address high inflation; and all will be good.” Stock market action shifted to “reboot” upward tech and large cap growth stocks; like saying, “they were the leaders; they are on sale after a 20% pullback; they can do it again” – the reboot. That’s the same action as in April 2000 – a reboot after selloff. But, shortly thereafter (2000) the tech selloff resumed. It seems doubtful that the recent rally of growth stocks is durable; it’s unlikely to endure. Recent split-market action is a “tug of war” between old market leaders (and investment styles), and new. That’s because the Fed is changing policy from QE to QT. The QE era is ending. The Fed and world events are changing the landscape. Globalization is changing. With 2022 being the year of rates – inflation and interest – a shift is occurring. Dividend paying stocks are shorter duration assets because they pay “income” through all market movements. Adding active fund management (which can focus on quality and financial characteristics that passive index investing lacks) to the tactical portfolio mix, is important strategy during rising interest rate environments. These tactics were working in 2021, paused in early 2022, and are anticipated to resume as Fed tightening policy moves forward. The Fed is just starting; it will raise interest rates more.

For investors, “a stitch in time, saves nine” means the markets are starting to react to a changing investment landscape. Market forces are not procrastinating. Politics aside; the market is acting. Unfortunately, it takes some time while the “tug of war” plays on. Buckle in! Watch the Fed and yield curve. Stay invested!

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc

END OF AN ERA?

Prior yield curve inversions and what they often imply (can miss a lot of additional upside):