We are thankful for your continued support and for receiving our guidance and advice on investing and “LIVING LIFE” financial planning during the last year – a year which could either be characterized as a “tragedy” or a “miracle”.

Whatever your perspective, 2020 offered BIG surprise (global pandemic, lockdown; or the financial market response to it all?). In this quarterly newsletter we provide brief articles below which aim to provide context about the year we all just experienced and the reaction of the financial markets; what we are focusing on in the year ahead with the dawn of both a new President and congressional political composition; and ponder what unexpected developments might occur.

Our personal finance article this quarter, “Light Bulbs Reveal a Better Idea“, discusses how helpful a big-picture view of your financial position is when the market inevitably encounters unexpected surprises. We observe clients who partner with us in our “LIVING LIFE” financial planning effort so often experience a “light-bulb”, epiphany moment.

A printer-friendly version of our quarterly newsletter can be obtained here: Q4 Nvest Nsights

FOR ALL, GIVE THANKS!

In all things; for all things, give thanks – whether small or big; even when pondering great concerns, it is good to flavor all things with thanks. That’s an attitude of gratitude. During 2020, there was much for which thanks was appropriate. Here are three ideas to consider:

- Family, friends, and our clients – we are thankful for the privilege to work on your behalf. Thanks for your support and for receiving our guidance and advice on investing and “LIVING LIFE” financial planning.

- Financial markets should receive our thanks – rallying for vaccines, medical treatments by first responders; and for the Federal Reserve’s quick action when markets were starting to panic.

- US consumers – who continued to buy products and services despite unprecedented hardships, aiding the US and global economy to keep moving albeit sluggishly.

Please give thanks for the many blessings received, including health, healing, and encouragement from so many good relationships. We express our thanks and wish you many blessings for this New Year, 2021.

–Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

TRAGEDY OR MIRACLE?

2020 could be characterized as a BIG surprise. Depending on your point of view, last year might be deemed a tragedy; or a miracle. What’s the biggest surprise – a pandemic; a global lockdown; or the financial market response to it all? Someone defined golf as an endless series of tragedies obscured by the occasional miracle. “Resolve never to quit, never to give up, no matter the situation” (Jack Nicklaus).

Last year provided all investors with a time of tragedy. The March 23 low (2192) for the S&P500 undercut the prior year low (2444), declining -35% in a month. All investors felt pain; a tragedy. Yet, the year-end close (3756) was above the prior year’s high (3248), generating an attractive +18.2% for the full year. The index exploded off the 3/23 low, rising +70.3% in 9 months. 2020 was a BIG surprise: 34 new market highs after the market low. Simply WOW!! The huge continuous volume of negative news would never allow anyone to expect a rebound like that. All financial assets zoomed upward due to huge fiscal spending (stimulus checks) and monetary support to the economy and financial market systems, both in the US and globally. Client portfolio values were handsomely higher as well. In essence, money growth was the “miracle” of 2020. It far exceeded what was needed to finance the economy, growing by a huge 25%. Excess money goes somewhere, and last year it flowed into financial assets whose prices soared.

History shares only 3 other examples in the last 90+ years where price action undercut the prior year low, and the final days of market action exceeded the prior year high. Those 3 years were 1935, 1982 and 2016. In each case, the following year provided double-digit advances of +28%, +17%, and +19%, respectively. The data sample is not many observations, so take it with a grain of salt, but it would be nice to add 2021 to that history set. At this point, there are few hints of market fatigue – economy shows signs of recovery; huge stimulus money provides support. We don’t expect the robust market action of 2020 to continue in the New Year; volatility will likely be ever present.

The events of 2020 share that while every crisis may be unique, the market’s interpretation or reaction to each crisis is not particularly unique. COVID was different than the financial bubble (2007), or dot.com (2000), which was different than 1987, or others. Intense fear creates market capitulation from many different catalysts. And rallies that follow seem to be accompanied by much intense skepticism. Markets rarely lead you down a wrong path too often or for very long. Investing does not require being cute, pursuing the latest fad, or “soup de jour”. Successful investing is best when keeping it simple. Remember, you don’t get too many opportunities to buy a market down -35% or -40%; it always appears that it could get worse, but probably not much. Tragedy or miracle? Both usually arise as a BIG unexpected surprise.

Let me share a few more golf statements for New Year humor. “It took me 17 years to get 3000 hits in baseball. It took one afternoon on the golf course” (Hank Aaron). “The older I get, the better I used to be” (Lee Trevino). “I have a tip that can take 5 strokes off anyone’s game: it’s called an eraser” (Arnold Palmer). For sure, “They call it golf because all the other four letter words were taken” (Ray Floyd). “The value of routine – trusting your swing” (Lorii Myers). The most important shot in golf is the next one” (Ben Hogan). True also with the investment routine – trust your process over and over again. Your next investment decision is very important. Golf in January in Ohio? No way; just wishful thinking for a “miracle” of warm temperatures without gray. Important in life – humor is the best medicine for the soul.

IN THE BLINK OF AN EYE

“In the blink of an eye” means quick, very quick; in a short time, or abbreviated. A person blinks every 4 seconds – that’s about 15 times per minute, or over 20,000 times a day (depending on your hours awake). Each blink lasts about a tenth of a second and is enough to clean and lubricate the surface of the eye. Thus, the phrase appropriately means extremely quick.

We shared comments on how amazingly fast the markets rebounded during a short 9 months to end 2020. We also shared that the market advance was propelled by government policies which acted like “rocket fuel” via rapid money growth in excess of amounts needed to finance the economy, both in the US and globally. Rapid money growth beats all else. It seems that the best trends that occur in business or investing move faster than one would ever guess, and exceed even the most optimistic of expectations. (Examples: oil dropped to $0 in February and now trades at $50/barrel; the Japanese Nikkei average surged from 23,000 to 27,500; Bitcoin moved from $12K to $35K in a matter of weeks). It happened in the blink of an eye. What does that mean for investing in 2021? Generally – positive, with several ideas to keep in mind.

The economic recession of 2020 appears over, except for those unemployed (at the lower-end of the pay/education scale) and small businesses that remain at risk. With savings already substantial and income replacement front-loaded due to Washington stimulus, growth should not be scarce in 2021. There are still risks near-term with health lockdowns (regional, not national) and still slow US mobility. Economists expect solid growth in both the US and globally. This should provide support for further financial market advance. In fact, the market rise is making that statement, growth is occurring.

Money growth will support economic prospects in early 2021, but may spell trouble in 2022 and beyond. During recent years and in 2020, it appeared that governments operated without rules – the only rule was there were none. The world governments discarded fiscal operating goals to flood the system with stimulus support. As we progress through 2021, fiscal spending rules will likely appear nonexistent because governments (US and other sovereigns) will pursue large spending actions to displace the negative economic effects from COVID and the Great Lockdown. The US election will transition to new leadership and policies. With the Georgia Senate runoff election complete, the composition of legislation and government action in Washington will change for the next couple of years at a minimum. With the same party controlling the White House, House of Representatives, and the Senate being 50/50 wherein the VP breaks ties, there will likely be less divided government or “gridlock”; financial markets historically prefer gridlock due to slower-moving policy change. Nevertheless, this partisan shift in Washington will be viewed as a mandate for bold action. A changing field of playing rules can be unsettling for business or the financial markets. Markets are anticipating another round of $2000 stimulus checks; Georgia’s senator changes provide that opportunity. More fiscal stimulus and deficit spending helps growth in early 2021, but creates headwinds for 2022 and beyond as budget reconciliation rules require repayment over 10 years; that will likely lead to tax increases and other regulations.

Stocks usually provide a positive return experience in the first year of a new administration, but with increased volatility. Investors should not expect robust returns of recent times to continue. Valuations of all investment types are extended. To normalize lofty valuations, company earnings need to continue to grow while asset prices stabilize and allow the current valuation gap to narrow. A new administration will announce new policy direction, which will create uncertainty to the market and investors. As an added result, volatility rises, and this too will dampen the upward pace of returns during 2021. Thus, stocks should provide for a positive return experience at a slower pace, with increased volatility – anticipate pullbacks or a correction.

2021 will provide its own excitement. Most years provide some unexpected surprise. Remember, it happens in the blink of an eye. What’s a prospective big surprise for 2021? Maybe it’s rising long-term interest rates. Most economic forecasters expect 10-year Treasury rates (currently rising above 1%) to finish 2021 between 1.25% and 1.5%. A very small number anticipate rates rising above 1.5%. The surprise is rates rising to near 2% this year. That could be a combo package of higher inflation from an expanding economy and/or the markets imposing its own limits on expanding debt and deficits (approaching 18% of GDP with no apparent cost). Rising rates could test the Fed’s resolve of keeping rates low for a couple of years. Higher rates could also challenge the global US dollar position which enjoys exorbitant privilege in currency markets. As always, higher inflation (oil and commodity prices are rising) and rising long-term interest rates do not define the time or hour of an unhappy “blink of the eye.” But for 2021, stocks should advance at a slower pace as the economy and company earnings rise and thereby narrow the valuation gap, and volatility increases – pullbacks or a correction are probable. Uncertainties (risks) include: sentiment is very bullish/aggressive; valuations are full; and rising inflation/interest rates could surprise.

What ideas are being pursued for client investment portfolios? During 2020, we re-established stock and bond allocations to “risk on” as appropriate for the investment objective of an account. We expected the recession to conclude. From experience, recoveries provide a faster market rise for small- and mid-size companies compared to large. And, valuations were more attractive in value-style (not expensive growth styles) and foreign. Even with bond allocations, we re-established exposures for recovering economic conditions. That worked very well. By the end of 2020, we needed to rebalance portfolios for risk; carving off above-target exposures to strong performing stocks and adding to bond allocations. Tough decision – but portfolio risk management is critical. Plus, if income tax changes are legislated, wherein capital gains are taxed as ordinary income, it is better to realize gains in 2020 when cap gains rates are low. 2020 provided a double tax benefit to taxable personal accounts – capture losses to offset future gains (avoid taxes) and then capture some gains at year-end before tax laws potentially change/rise. We are pursuing being fully invested, because we expect financial market to continue to advance, as written herein.

The history lesson from the financial markets indicates that long term returns are up with stocks beating bonds often, and by a lot. Thus, if you have time on your side, you want to own more stocks than bonds. Of course they also experience more volatility. As a result, the best investors are like Rip Van Winkle – they take a long nap and miss the annual surprises. To be successful, you must be invested before you nap. If you are prone to watch and stay awake, you may be surprised what can happen in the blink of the eye. Look back at 2020. Just don’t react on emotion; that’s trouble.

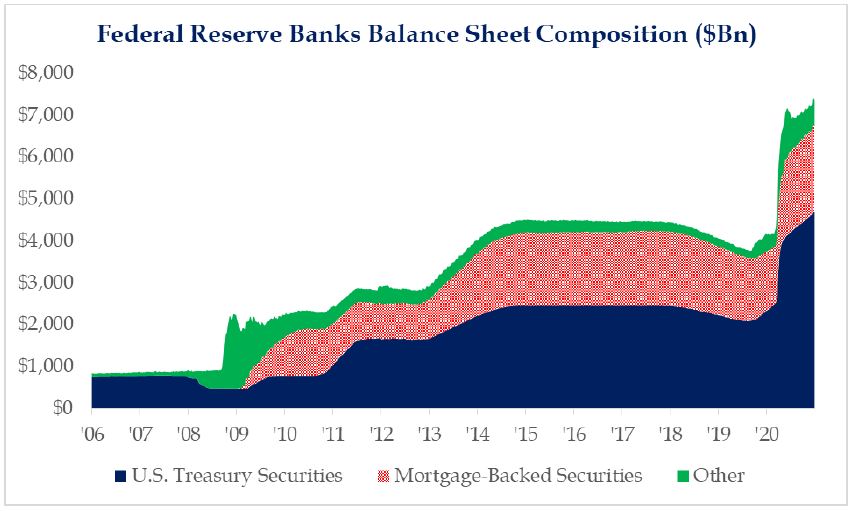

UNPRECEDENTED INTERVENTION…

In response to the economic lockdowns imposed to slow the spread of COVID-19, policymakers around the globe pursued extraordinary fiscal and monetary stimulus in early 2020. In the US, the Money Supply (M2) is up an astonishing +25% over last year and the Federal Reserve grew the size of its balance sheet over 75% by quickly dusting off programs first created during the 2007-09 “Great Financial Crisis”. For now, it appears that governments can operate without fiscal limit, and financial assets are a benefactor.