“Geopolitical conflicts and/or exogenous events do more to reinforce trends already in place, rather than act as a catalyst for change (in the markets) – Strategas Research Partners.” Gold is rallying; oil is in a bull run higher; value style is besting growth while Tech is a pronounced underperformer. And Bitcoin –who’s strongest advocates claim it to be an alternative currency – is yet to offer any hedge or stability to risk assets. These trends don’t change (because of geopolitical issues), just the urgency of them. The horror and uncertainty of the Russian/Ukraine invasion is extreme; it is terrible, inappropriate, and immoral. It is most challenging to offer thoughts on how it will play out, as no one knows. We can pray that it is a temporary geopolitical event which will hurt Russians economically, and will slow Germany and Europe economies (to a lesser degree), and will marginally slow other global economies depending on their connections to Russia/Ukraine. At present, the US bond market is functioning normally (unlike March 2020 when COVID hit and the Great Lockdown was initiated). There is increased volatility in all markets, but there is not dysfunction. There is the normal, predictable flight to safety. Please read our Special Market Update, “Market BUMPS to Climb On” from February 23 on our website, at www.nvestwealth.com.

A Grammy Hall of Fame favorite song of many “Turn! Turn! Turn!”, by the Byrds, was first recorded in 1965. Fun fact about the song – its lyrics were written almost 3000 years ago by Solomon, which are recorded in Ecclesiastes 3:1-8. The lyrics of the song and Bible verses convey that everything is always changing. “There is a time for every season!” Even “a time of love, a time of hate; a time of war, a time of peace; …And a time to every purpose, under heaven.”

A key idea for 2022 is the year of rates – inflation and interest rates. The early part of 2022 is very much characterized by volatility relating to investor worry about rising rates. Americans normally are happy when the economy is growing rapidly. One would guess joy would abound with higher wages. But, inflation is running hot at 7.6% (40-year high) and erasing those wage gains. Add continuing product shortages from supply-chain disruptions and a lingering pandemic, plus geopolitical issues (Russia/Ukraine; China; Iran), and the result creates widespread discontent. The public experiences elevated political and economic uncertainty. That’s not a good current mood for the financial markets.

In actuality, there may be a “regime change” occurring. You could say this is the first time in “QE era” that bond yields are rising during a market correction. The quantitative easing era (of the last 13 years) is ending. During this time, central bankers in the U.S. and globally pegged interest rates at zero while also buying bonds in the open market, providing a super-accommodative easy money policy. The result of this era was growth-style investing ruled the performance charts; value-style trailed often, sometimes by a lot, and was deemed by many as “dead.” But accommodative QE is ending as the Fed and others are ending bond purchases and are poised to begin raising interest rates to combat rising, sticky inflation. That poses a tricky issue because price inflation is high for both goods and services. The Fed can no longer ignore it. “Inflation is an economic problem, and also a psychological proxy for things being out of control.” It’s appropriate to say, “The times they are a changing” (Grammy Hall of Fame song written by folk singer Bob Dylan, in 1964).

For two consecutive months, market and portfolio action is challenged. Stock markets entered their first correction (10% pullback) of this new bull market (since March 23, 2020). It was displayed with volatility – up/down action – during February as the Fed shares plans for addressing sticky inflation. Stocks and bonds retreated in February and YTD; the S&P 500 was down -8.6% since the last market high on 1/3/2022. For the economy and financial markets, they are uneasy if the Fed will do too much; will they raise interest rates too high or too long and cause an economic contraction? With supply and demand not yet balanced, inflation continues to hinder real economic growth. Watch the yield curve – if it inverts (when long rates are lower than short rates), the economic outlook is deteriorating. Pending more clarity on several policy issues – monetary policy, fiscal policy and geopolitical issues – the market action is likely to remain volatile.

We recently made several tactical changes to the stock allocations in client portfolios. These early-year adjustments trimmed exposure to high-valuation growth stock areas in favor of adding weight to value style (better valuations and increased dividend focus) with less risk. Further, we added an exposure to oil/energy (or other commodity) ETF for its diversification and return benefits during inflationary and geopolitical challenges. We also believe this current market correction is likely a pause that refreshes, creating a more attractive buying opportunity than since this new bull market began. “Turning” dynamics mean that grabbing risk is waning. These recent tactical adjustments align with the following themes.

Value remains cheap compared to growth. Growth stocks were in high demand; their prices were elevated, particularly popular technology and FAANG stocks. Expectations for rising interest rates also increase the discount rate used to value future earnings of all stocks. A higher discount rate lowers the present value of that stream of future earnings. In other words, a company without yield and trading as a high multiple of sales (current and future) are the stock equivalent of zero coupon bonds. They will acutely feel the effects of higher inflation and interest rates. (Sorry for being too technical). That means risk resides within highly priced growth stocks, which generally do not regularly return cash to investors via dividends. Growth stocks are considered long-duration assets. Alternatively, value stocks often pay dividends and are considered shorter-duration assets. Their valuation is a return of earnings and cash that is received currently, giving dividend-payers an attractive value which is non-existent with non-dividend paying (growth) stocks.

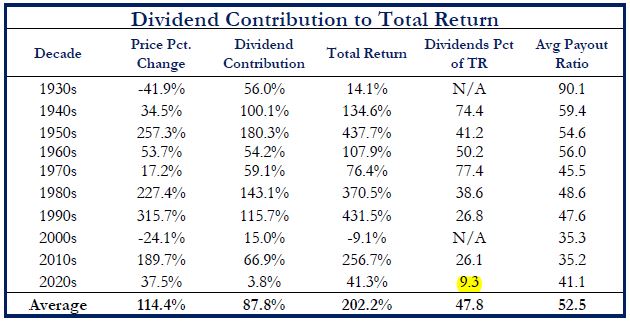

Dividends are likely to play a larger role in returns. Historically, dividends (paid) provided near 50% of the total stock market return since the 1930s. Every investor receives “total return” – the combination of dividends plus price appreciation. The entirety of non-dividend paying stocks’ total return is from price change. Price change alone can produce quite variable experiences over various time intervals. Dividends, usually paid quarterly, can boost or offset the rising/falling price change component; thereby smoothing-out the total return experience. In the 1960s and 1970s, the dividends paid by the “Nifty-Fifty” stocks provided 50% and 77%, respectively of the market’s total return. This was an era of dividend-focused investing. Interesting too, the 1970s experienced hyper-inflation and very historically high interest rates. Dividends provided returns when stock prices were struggling. For the past 20 years (during the era of zero interest rates), dividends provided relatively small contributions to total return; more return was derived from price change. Specifically, dividends provided less than 10% of the market’s total return; almost 90% of the market return was via price change.

So why “Turn! Turn! Turn?” Could it be “the times they are a changing?” The end of QE and start of QT (quantitative tightening) may usher in a change in style focus that benefits value and dividend-paying stocks. Short duration assets could provide better returns than growth or long-duration assets that pay small or that are non-dividend paying. Remember, client portfolios own both value and growth style funds, with tactical strategy favoring value at this time. Sticky higher inflation that is causing the Fed and others to implement tighter monetary policies are the catalyst for the change. Thus, 2020 is dubbed the year of rates.

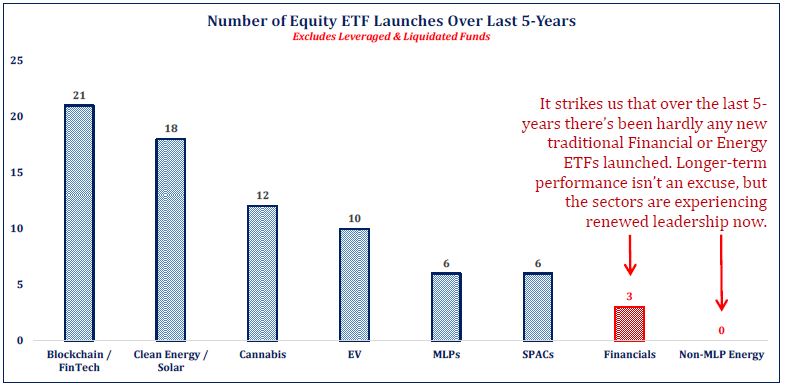

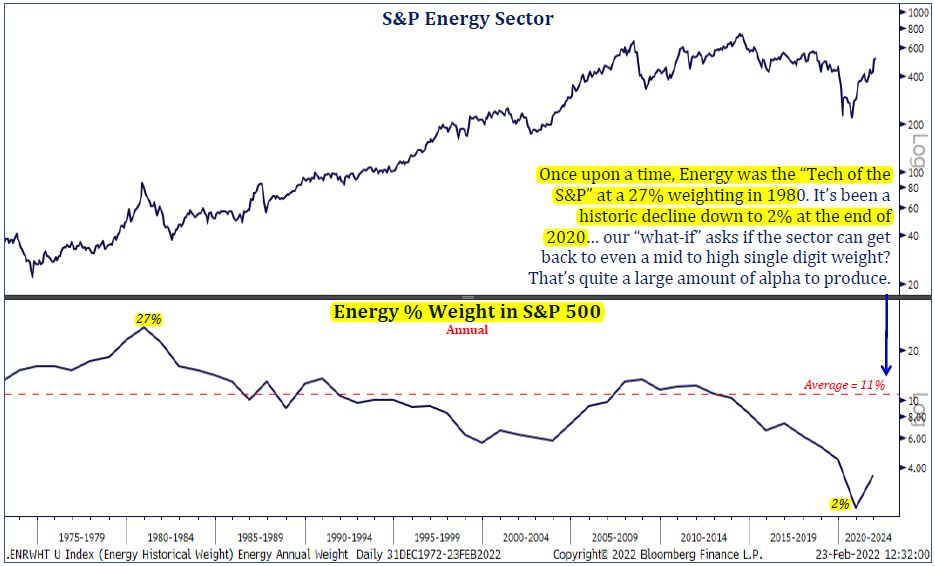

Desire another contrarian tactical thought? Over 900 Exchange Traded Funds (ETFs) were launched in the last 5 years. Thematic funds are running at record paces – whether Blockchain and FinTech focused (21 launches), Clean Energy (18), Cannabis (12) or even SPACs. And 90 ETFs were launched with some form of ESG (environmental, social and governance) mandate. [Amusing: many look so similar to the S&P500 index with 5 times higher operating expenses than the index fund, but were applied an ESG label; many were overweight Tech.] On the contrary, only 3 traditional Financial ETFs were launched and zero focused on traditional Energy.  Lackluster performance was clearly responsible. Most funds/ETFs own little exposure to traditional energy names, which currently only accounts for about 3% of the S&P500 index (in 1980 it represented over 27%); energy was the “tech of the S&P. With focus on clean alternative energy and sources, it will be many years before such a conversion is largely accomplished. A political supply imbalance was created which is boosting prices; it’s occurring at the same time as demand climbs following the Great Lockdown and the Russia/Ukraine geopolitical conflict. The energy sector sports a dividend yield of 3.4%, better than the S&P500 as a whole and higher than 10-year Treasury Notes. As we know, higher energy prices are like a tax to consumers, reducing other usual spending/saving. Is this not an irony, or contrarian investment idea? When others dislike…, it’s probably a worthy consideration. Another: “Turn! Turn! Turn!”

Lackluster performance was clearly responsible. Most funds/ETFs own little exposure to traditional energy names, which currently only accounts for about 3% of the S&P500 index (in 1980 it represented over 27%); energy was the “tech of the S&P. With focus on clean alternative energy and sources, it will be many years before such a conversion is largely accomplished. A political supply imbalance was created which is boosting prices; it’s occurring at the same time as demand climbs following the Great Lockdown and the Russia/Ukraine geopolitical conflict. The energy sector sports a dividend yield of 3.4%, better than the S&P500 as a whole and higher than 10-year Treasury Notes. As we know, higher energy prices are like a tax to consumers, reducing other usual spending/saving. Is this not an irony, or contrarian investment idea? When others dislike…, it’s probably a worthy consideration. Another: “Turn! Turn! Turn!”

As noted at the end of our special market update last week, “You don’t have to be smarter than the rest. You have to be more disciplined than the rest.” Further, “to invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework.” Warren Buffet

Printer-Friendly PDF – March Commentary 2022

Bill Henderly, CFA | Nvest Wealth Strategies – March 2, 2022

Chart Sources: Strategas Research Partners