Special Market Alerts are generally undesirable to write. That’s because we never intend to raise alarm or create uncertainty. How should investors think about the first 10% correction of this new bull market? Certainly a correction was due following 23 months since the March 23, 2020 bear market bottom. From that time, the S&P500 jumped +121.1% to its last closing high on January 3, 2022 without even a 5% pullback. Since early January, investors ramped-up their worry about everything – sticky inflation at +7.6% (highest pace in 40 years); persistent supply and demand mismatches for products, services, and workers, creating shortages. When demand is greater than supply, prices will rise. In fact, someone said “Inflation is an economic problem, and also a psychological proxy for things being out of control.”

Stocks and bonds are considering what’s next – 2022 is the year of rates. Will upcoming interest rate increases by the Federal Reserve to combat high inflation be too much, and thereby stall a growing economy? Will geopolitical issues – Russia/Ukraine, China, Iran, and energy – exasperate inflationary pressures? Often the American public is happy when the economy is growing rapidly, and workers are experiencing higher wages. But, with inflation and energy prices significantly higher, real wages (after the effects of inflation) are moving backward. Polls show discontent is widespread – inflation, shortages, and lingering pandemic. The public is experiencing elevated political and economic policy uncertainty.

Russia/Ukraine is a temporary geopolitical event. Financial markets dislike uncertainty, particularly geopolitical, but history reveals that markets move past these issues fairly quickly. Might we be near “peak Russia”? 2022 is also a mid-term election year which bodes for some volatility during the second part of the year. Key for investors – it’s the year of rates, both the rate of inflation and interest rates. Hopefully, we are near “peak bottleneck” wherein supply disruptions are easing. If consumers cool their purchases some, they can help the Fed arrest inflationary pressures. That means we may also be close to “peak inflation”. The Fed will begin raising interest rates in March – that hits Main Street. And they must start to address the huge Federal balance sheet created from 2 years of buying bonds in the financial markets – considering runoff or liquidate slowly; this will be an issue affecting “Wall Street” (big financial firms and big public companies) increasing the future cost of financing. Policy changes need to be monitored closely – it’s said that it’s the last rate increase that hurts.

At this time, maintain your long term investment goals. We observe there is a shift in market leaders; client portfolios are already tactically adjusted to experience the better valuation benefits that exist. Please consider current depressed investor sentiment and elevated policy uncertainty as contrarian indicators. It may not “feel good”, but when sentiment is depressed (worries possibly near “peak”), the markets are creating a pause that refreshes; an opportunity for future market rise. After all, the market bumps are what we climb on.

“You don’t have to be smarter than the rest. You have to be more disciplined than the rest.” Further, “to invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework.” Warren Buffet

Call; email; or better yet, schedule a time to visit with us in the near future.

PS: In early March, we will send our monthly market commentary – preliminary title is Turn! Turn! Turn!”

Bill Henderly, CFA | Nvest Wealth Strategies, Inc – 2/23/2022

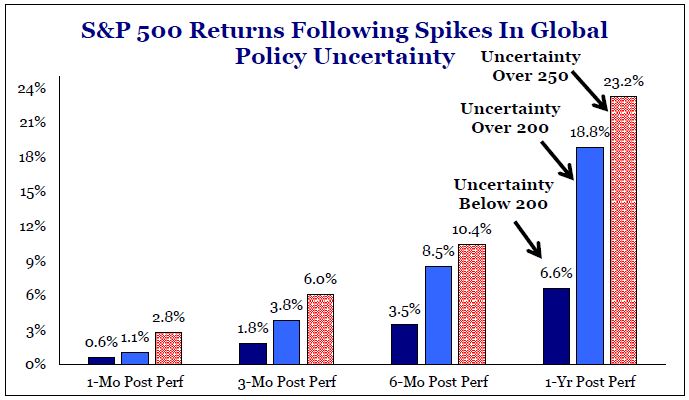

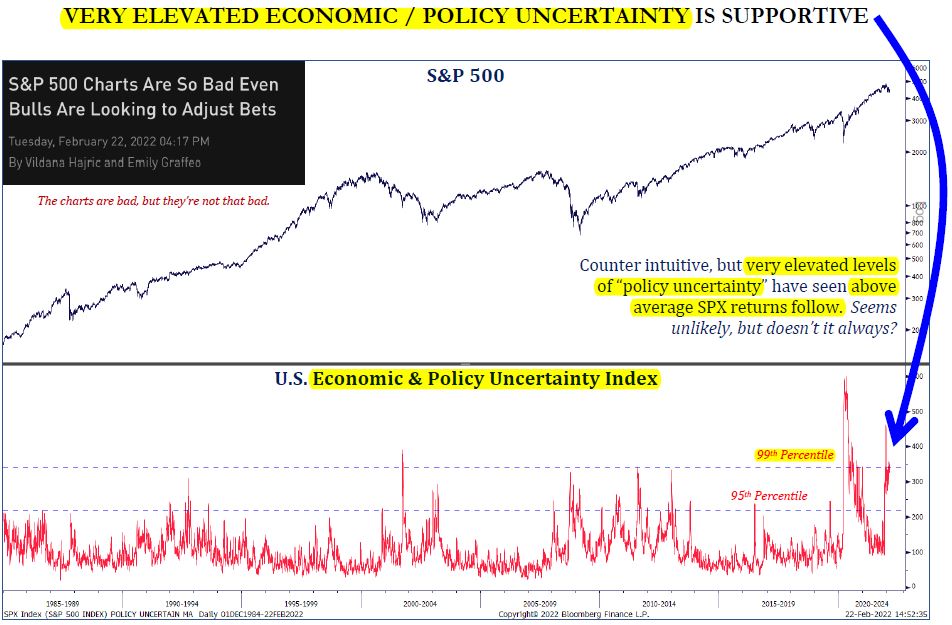

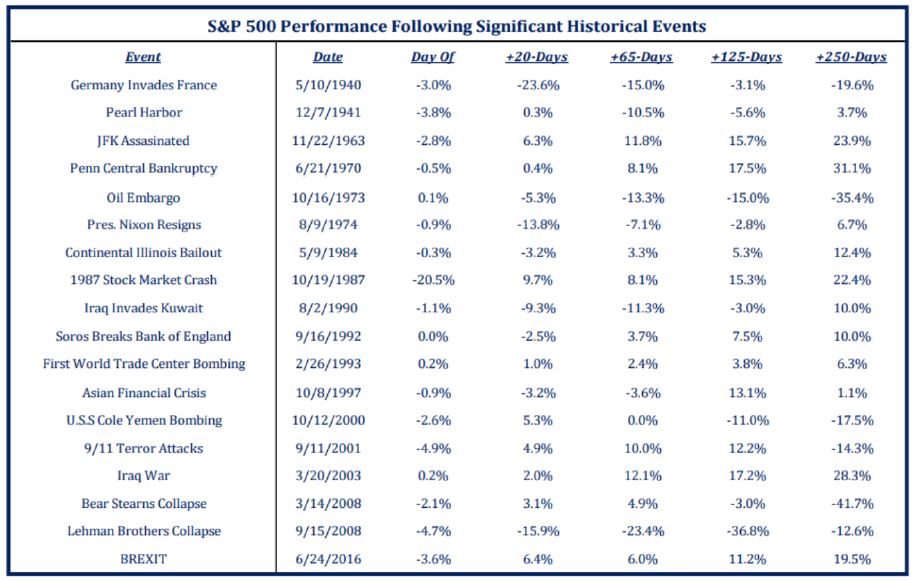

Charts of Interest (source: Strategas Research Partners)