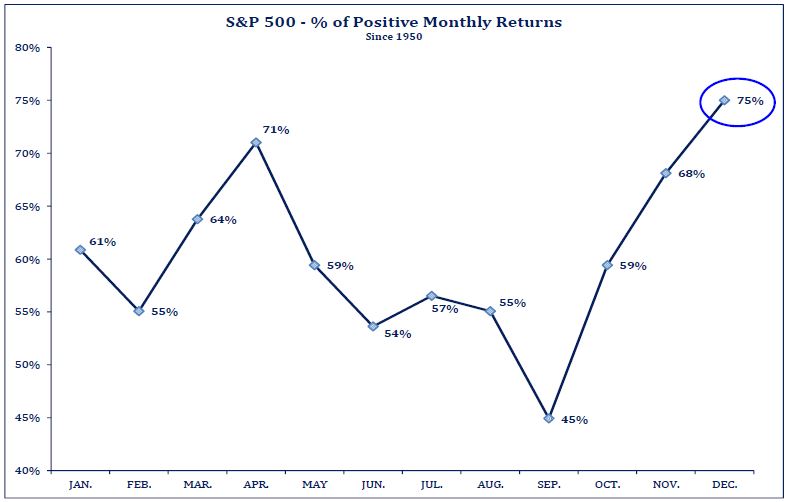

All the historical hype surrounding favorable mid-term election year investment returns is yet to materialize as we conclude 2018. Since 1950, every mid-term election (17 of them) resulted in strong end-of-year stock performance because the unknown of political change concluded. A different stock market stat, again since 1950, reflects that 75% of December returns are positive; that is the highest single month probability of upward performance for any of the 12 months (next highest is April at 71%, and November with 68% of the time being positive – see chart below). This year, the 4Q experience to-date seems stark opposite.

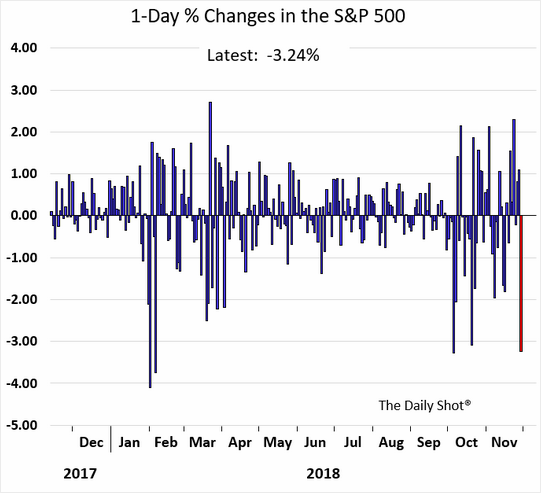

US stocks stabilized in November but remain well below their YTD highs reached in late September. During November, the S&P500 recovered +1.8% as the final week propelled all indexes to positive returns, thanks to Fed Chairman Powell’s remarks on 11/28. For the year-to-date, most asset types remain fractured after a punishing autumn experience, the second market retreat this year.

Several key factors make up the backdrop of current uncertainty for the financial markets. Most investors acknowledge the current bull market is 117 months old (approaching 10 years since March 9, 2009). It is old compared to the historical average life of a bull market (60 months), and consensus does not expect much. Additionally, recent economic stats are deemed by many to be as good as they get. Investors are keenly watching, or worrying about two things: 1) the Fed’s path to normalizing interest rates and 2) the current tariff negotiations with China. Both are contributing a higher level of uncertainty for domestic and global economic growth, and both are influencing prospects for the stock market to log further advance.

First, the Fed seems set to raise interest rates a 4th time in 2018 this month, for a total of 100 basis points. This is not the only domestic monetary tightening that is occurring though. Because US interest rates are attractively high compared to most other sovereign rates, the US dollar is also strengthening while the global economy is moderating. A rising US dollar strains our domestic ability to export products at higher prices, which can result in slowing export sales and slower domestic economic growth in general. Further, the Fed is shrinking its balance sheet by not reinvesting proceeds from maturing bonds it purchased under years of QE action; this is another tightening event that takes money out of the financial system. Too, most all investors and economists anticipate additional interest rate increases in 2019 and into 2020. Altogether, monetary policy is tighter – becoming visible as demand for housing and autos are sliding as interest rates rise. Too much too fast can break the economy, and markets. So, what’s the rush?

The autumn market retreat provides a first test to Fed Chair Powell’s normalizing interest rates process. All new Fed chairmen seem to receive a market challenge early in their tenure. In what seems to be an intent to calm markets, Powell is recently conveying a more cautious tone stating that, “Raising rates is like working in a dark room – you need to move slowly to avoid stubbing your toe” [running into something, or falling]. Then, on November 28, Powell mentioned that current rates are near the bottom of their neutral interest rate range. These comments suggest that the Fed may become more data dependent instead of appearing to be on a planned path to higher rates irrespective of the economy. This offers the idea of policy flexibility in 2019. If the Fed is slower to raise interest rates, if they shift to greater sensitivity to economic data, investors will determine the Fed is not proceeding on a regular path of rate increases that could jeopardize domestic economic growth. This is an important first development to modifying the current worried financial market air. It seems appropriate that the Fed moves slow, maybe even pause, while it monitors and then acts when/if needed; they may not need to stop; just go slow. There’s no rush.

Tariff concerns are the second critical influence on domestic and global economic growth prospects. The clash between the US and China is big, and affecting business confidence. This is showing up in slow capital expenditures (CAPEX), which should be advancing due to 2017 tax reform changes providing for immediate expensing. When unemployment is low and wages are starting to rise, CAPEX spending on productivity enhancing processes could boost economic growth and keep this economic cycle going. But, as tariff talk remains in process, markets will likely show increased volatility.

The US economic path forward is slowing, but remains in good shape. Historically, our economy never entered a recession with corporate profits rising. Few predict a recession on the near horizon, and inflation is looking managed, particularly with oil prices dropping recently. Globally, economic developments are softer because tariff issues are draining business confidence and slowing economic growth prospects.

Tariff talk is shaking the markets. The autumn market volatility is proof. But over the past weekend at the G-20 summit meeting, a tariff reprieve developed. A temporary 90-day truce of tariff levies rising from 10% to 25% (effective January 1st) was offered. During this delay, trade talks between the US and China should occur. These talks are critical to US, China and global economic growth prospects for 2019 and beyond. While this reprieve is akin to “kicking the tariff can down the road”, it does delay and potentially eliminates a $60 Billion headwind to the economy in 2019. Slowing domestic economic growth is not desired.

Did you know? Or, we should recall there are similarities with the recent G-20 meeting and the one in February 2016. And, when adding the revised Fed outlook and language about policy reaching neutral rate levels (possibility to go slow), could this be, or maybe this provides an inflection point for financial markets like that of February 2016!? Recall, US stocks advanced almost 2 years from 2/11/2016 without a 5% market drawdown. That’s not our prediction; but it is interesting to observe similarities of market backdrop conditions. Yet, we are encouraged by a Fed that sounds like it is near its neutral rate level and sensitive to economic developments, AND by possible progress on tariffs and trade.

As helpful as several recent days were in offering relief around these two biggest concerns of investors (tariffs and the Fed), it still seems difficult to be a long-term investor. In the short-run, the still flattening yield curve (nearing inversion) seems to be the next big worry for the markets to navigate. Inversion of the yield curve would suggest that interest rates are too high (deemed a policy mistake), and the economy will slow dramatically. Also, too much politics and no-news media can easily drain an investor’s commitment to remain invested pursuing long-term goals. Fear today is prevalent; in fact euphoria is absent throughout this entire 9-year Bull Market advance. This bull remains unloved. Ultimately, stock prices are a function of future earnings and interest rates. Given recent events, it seems prudent to go slow with interest rates – What’s the rush? But, with tariff talk, some haste will calm the markets.

Whatever the outcome of December, it seems likely 2018 will conclude making good on an early year prediction that for the first time in many years the economy (robust) might meaningfully outperform the markets (relatively flat). Turning focus to 2019, tariff talk resolution, stable oil prices, a Fed pause, and foreign stimulus could provide a global boost to economic growth that supports an upward advance to asset prices, and stocks in particular.

We, at Nvest Wealth Strategies, wish you and your family a Merry Christmas and a Happy New Year!!!

Author: Bill Henderly, CFA – December 5, 2018

Printer-Friendly PDF can be downloaded here: “What’s The Rush?”

Additional Item to Note:

Tuesday December 4, was one of the worst days of the year for stocks – probably mostly due to computer trading activity triggered by the inversion of the Treasury yield curve between 2 and 5 years (2-year yields higher than 5-year yields), and uncertainty about success from the tariff 90-day truce. The inversion of the 2/5 yield curve suggests that the Fed may have already went too far and should not pursue any additional hikes, but both developments are largely reversing more encouraging market moves from last week.