Bruce Wayne and Peter Parker were seemingly ordinary citizens that took it upon themselves to correct wrongs they observed. To most, they were viewed as heroes but others felt they were disruptive and no better than the criminals they were squaring off against. In the last couple months, there is talk of bond vigilantes in the financial markets. Who are they – blamed for exacting pain on both stocks and bonds? Are they villains or heroes? The term “bond vigilantes” was coined by analyst Ed Yardeni in 1983 to describe the role bond investors played in disciplining governments by issuing bonds to finance spending, that looked irresponsible. At the time Yardeni wrote, “if the fiscal and monetary authorities won’t regulate the economy, the bond investors will.” With both stocks and bonds suffering a 3rd consecutive month of pressure and significantly erasing what were nice YTD gains to end July, let’s pose the question: are bond vigilantes a hero or villain?

In the last 3 months, yields on 10-year US debt increased from 3.9% to near 5% today – a level not seen in 16+ years. The market is quickly subscribing to the view that rates will be higher for longer due to fiscal deficit concerns and stubborn inflation strengthened by new geopolitical turmoil. While the Fed sets short-term interest rates (Fed Funds rate), it is the market that establishes rates for every other maturity and borrower… including the US Government. In the short-term, bond vigilantes feel like villains as their actions pressure financial assets and renew concern about economic slowdown or recession. Yet in the long run, whether the bond market is a villain or hero depends on your perspective. Is it important for governments to control their spending relative to revenues? Interest expense for the US Government hit 14% of tax revenues in July and is projected to exceed the entire defense budget next year. Strategas Research Partners puts it this way: we can choose whatever size of government we like, but the markets are saying we need to get better at paying for it in real-time. This means, either shrink the amount of spending (government); or increase tax revenue to pay for it. Neither feels particularly attractive to politicians, nor likely heading into a Presidential election year.

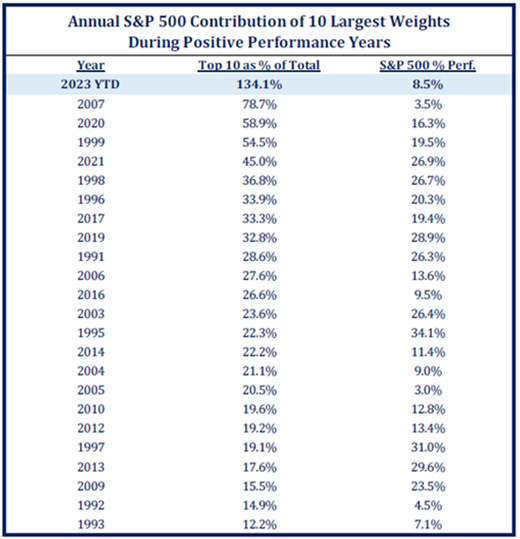

The stock market is likewise feeling the influence of higher interest rates. Since the recent market high on July 31, more than half (56%) of all stock ETFs are down between -10% and -20%. The widely followed S&P500 index declined -8.27% during that same time. Neither is good, but this index is increasingly a mirage, and masks the weakness being felt by all but the biggest companies.  The top 10 contributors in the S&P500 are responsible for 134% of the YTD gain. In other words, the other 490 stocks making up the index are collectively negative! That’s frustrating for fundamental investors (like us) who believe there is benefit to diversification. There are compelling opportunities in mid, small, and international companies as well.

The top 10 contributors in the S&P500 are responsible for 134% of the YTD gain. In other words, the other 490 stocks making up the index are collectively negative! That’s frustrating for fundamental investors (like us) who believe there is benefit to diversification. There are compelling opportunities in mid, small, and international companies as well.

“Storms” like the present are part of long-term investing – the S&P500 bottomed on October 12th, a year ago after losing roughly -25% of its value during the first 9 months of 2022. In the early days off that low, stock advancement was broad. But since March 2023, participation is about as narrow as one can remember. Our communications this year are consistent. We remain guarded that the stock market recovery since last October is the beginning of a new bull market. This perspective is due to awareness that small companies tend to advance strongly in a new bull market, but are negative YTD. Similarly, banks are often referred to as the transmission of the economy but are down 18% from a year ago… a first in over 100 years coming off a bear market low. It is also difficult to feel excited when money flows overwhelmingly skew toward risk-averse destinations such as money market funds; those flows are +25% greater than last year. These market details are uncharacteristic of durable bull markets.

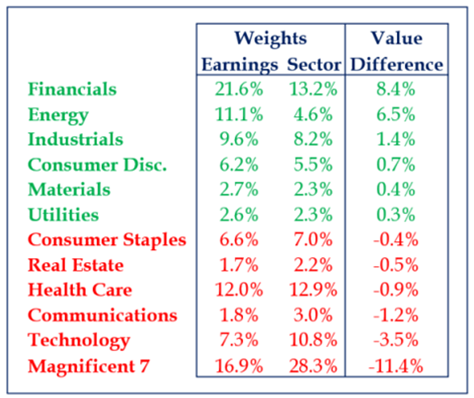

How much longer will current market pressure and narrowness persist? Like you, we struggle watching investment performance evaporate. It is frustrating to observe a few expensive companies like the “Magnificent 7” distort the market. While the Magnificent 7 represent 28% of the S&P500 total price, they only contribute 17% of the earnings. Energy, financials, and industrials by contrast are underappreciated relative to the earnings they contribute. We should not abandon valuation discipline and shift focus from higher quality to lower quality. Risk should not be confused with short-term price volatility, but instead be defined as the permanent loss of money. Paying too much for something can result in permanent loss. While 3 months of weak market performance feels bad; higher yields should slow the economy. Yields that remain higher also likely allow the Fed to remain on pause. Maybe this will allow the market to find footing. We are reminded that interest rate cycles can trend in one broader direction for decades at a time; after a 35+ year secular trend of declining rates, did 2022 mark the start of a new cycle where rates drift up (and imply a different absolute level of volatility and return? See chart below).

The geopolitical uncertainties of war as well as the 2024 US presidential election, suggest a volatile tug of war may continue; experiencing higher and lower action, and winners vs. losers. This supports favoring less expensive areas of the market that also provide current yield.

We are reminded from history that markets can move when investors do not expect it – climbing walls of worry. One must be invested to enjoy these moves despite how challenging the volatility can feel. Invest with a focus on fundamentals and valuation as these ingredients can help you reduce risk and promote success over the long term. Bond vigilantes – hero or villain? To the extent they encourage discipline and “regulate” government, we believe the short-term pain will prove positive for portfolios and our tactical positioning in the long run.

Did you know? A slew of weight management drugs is receiving much hype from the investing public in 2023. Their market chart action looks like a rocket ship lift-off. Is the market, like society, in love with promises of quick fixes for health? Taking a pill is easier than the original Weight Watchers program of discipline and exercise. Are bond vigilantes like “Weight Watchers”? Both monitor and encourage to not indulge, to restrain and begin pursuing more healthy habits. Will government hear the message, or will bond vigilantes need to raise bond interest rates even more?