Shipping and logistics firms often cite that it is the last mile of delivery which is the most expensive and complex in coordinating. And seasoned runners report that it is the last mile of a race that often seems most difficult. Some may say the middle mile is challenging – too far to turn back and yet a long way to go. Nevertheless, it is that final mile which requires every drop of will power and can seem significantly greater in distance compared to earlier miles. As one who does not run long distances regularly, I participated in a Thanksgiving Day “Turkey Trot” with my family and neighbors, perhaps to justify eating too much and watching football later that day. It seemed do-able and fun when signing up a month before. And as we began, it seemed easy at first to keep pace with my 11-year-old son; but fatigue seemed to set in early. I’m certain there are other examples where the challenge seems to grow toward the finish. Might the same prove true with respect to lowering inflation without causing significant economic pain?

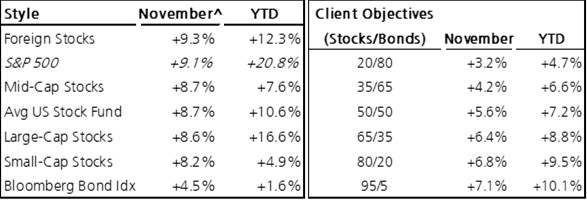

After 3 consecutive months of market weakness, stocks and bonds leapt higher in November. Interest rates eased off recent highs of around 5% as investors received encouragement in recent CPI readings. Inflation is significantly improved from a year ago but still remains elevated compared to the past 20 years. Lower inflation and a resilient economy (3Q GDP accelerated to 5%) provides encouragement to the investment community that 1) the Fed can officially conclude its aggressive rate-hiking campaign (or at a minimum remain on “hold”); and 2) that the unicorn “soft landing” might still be possible. Soft landing, in other words, means inflation resides near its long-term target levels without creating significant economic pain. That causes many to wonder, is the current rally “real”, or little more than a “Santa Claus rally” that arrived a couple weeks early this year?

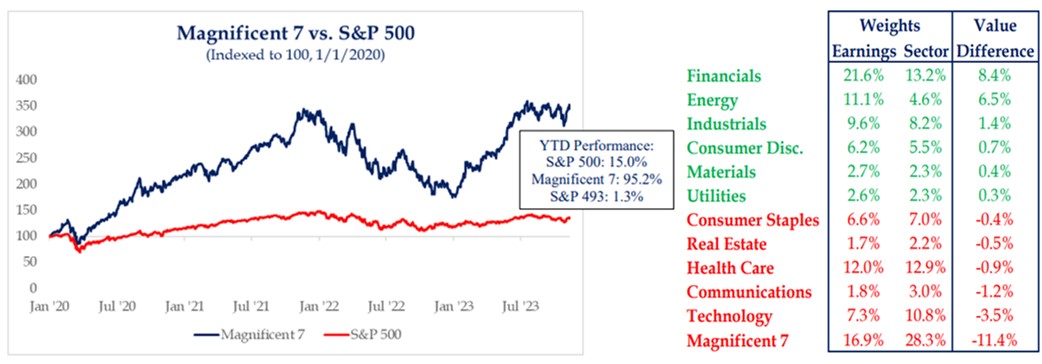

Like most years, 2023 feels like a roller coaster type ride containing numerous hills and valleys. The stock market was up nicely despite several volatile periods as it concluded July, especially when looking at indexes like the Nasdaq or S&P500 which are heavily skewed by the “Magnificent 7”(1) group of stocks. Then, worry resurfaced as government spending awakened “bond vigilantes” in August, September, and October. Vigilantes pushed yields quickly higher on US government bonds from 3.85% to 5%. The abrupt increase in the cost of financing created “spooky” pressure on both bonds and stocks. Investors replaced optimism with concerns that tighter financial conditions would finally sink the economy and usher in recession.

But just as quick as retailers clear out Halloween products/decorations and turn their focus to Christmas, the market seemed to follow-suit. The rebound of stock and bond prices in November was powerful; stocks enjoyed their best performance since the October 2022 bear-market low. There are some signs that market strength is broadening out, but as highlighted by us frequently this year, it’s hard to find many years where so much performance is owed to so few stocks. The “Magnificent 7” are responsible for more than 28% of the weight of the S&P500 and largely responsible for its 20% return YTD; yet when all 500 companies in that index are equally weighted the YTD return is just 8%.

Client portfolios own the “Magnificent 7” via inclusion in the Schwab Large-cap Growth ETF (SCHG), but not to the extent they are represented in the S&P500 or Nasdaq. (It’s nice that portfolios avoid the “Filthy Five”, “Nasty Nine”, and especially the “Dirty Dozen”[sarcasm]). See charts below. Recent strength is yet another reminder to remain invested for the long term, because the market often turns when the mood is sour.

Will the Fed successfully execute the improbable soft-landing? The soft-landing scenario requires that inflation continues to trend lower and unemployment weakens only enough to curb wage pressure, but not so much that it dents consumer confidence. This would allow the Fed to cut rates from current restrictive levels to stimulate economic growth, rather than slashing rates aggressively to stimulate a faltering economy. Lower interest rates would reduce financial pressure on consumers and businesses, and help earnings grow… again without fanning a new wave of inflation. The most bullish economists suggest they are seeing some indications that productivity is rising, most likely driven by technology (like AI). This helps reduce labor costs and improve profit margins. Other economic stats reflect some improvement in growth and productivity.

Is it possible that the “last mile” of this race to normalize inflation will be easier and less painful than earlier miles? What could allow these desired conditions to materialize? Can the Fed engineer the improbable soft-landing in 2024? History reveals that inflation rises, then falls, and they rise/fall in cycles. Food and housing inflation could likely remain elevated. If so, the Fed could be driven to keep rates higher for longer, so inflation does not trend higher.

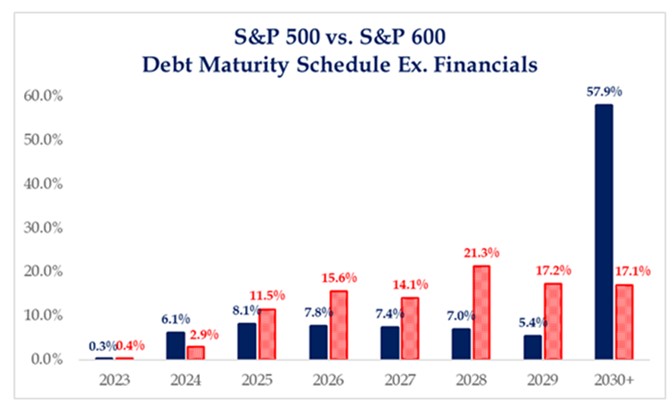

We are cautious however, not outright pessimistic or bearish, but hold some skepticism that it will be easy. First, little is being done to right-size government spending which is too high relative to revenues (taxes). Big government spending, all-else equal, is inflationary. Second, 2024 is a presidential election year, and no politician believes election success is possible by taking things away; rather incumbents like to spend. Third, the economy is yet to see the full effect of higher interest rates hitting consumers who locked in low mortgage rates; or businesses which will experience greater refinancing of existing debt beginning in 2024 and 2025 (see chart). As a result, it seems likely that interest rates could remain higher for longer. The investment environment could remain “confusing” and somewhat “stuck” in a range. Perhaps it’s the effects of traveling the “painful last mile” with inflation and government fiscal policy.

We are cautious however, not outright pessimistic or bearish, but hold some skepticism that it will be easy. First, little is being done to right-size government spending which is too high relative to revenues (taxes). Big government spending, all-else equal, is inflationary. Second, 2024 is a presidential election year, and no politician believes election success is possible by taking things away; rather incumbents like to spend. Third, the economy is yet to see the full effect of higher interest rates hitting consumers who locked in low mortgage rates; or businesses which will experience greater refinancing of existing debt beginning in 2024 and 2025 (see chart). As a result, it seems likely that interest rates could remain higher for longer. The investment environment could remain “confusing” and somewhat “stuck” in a range. Perhaps it’s the effects of traveling the “painful last mile” with inflation and government fiscal policy.

Investors should not lose sight though, there is a huge amount of cash sitting in money market funds, on the sidelines. If investors develop FOMO (a fear of missing out) and interest rates drift lower, could this prove to be a catalyst for further market advance – the Santa rally and attractive start to 2024? Ho ho ho! We hope so!!

Client portfolio construction is anchored by owning no-load mutual funds and ETFs focused on quality companies at fair valuations; this tactical mix should provide solid returns with lower volatility. Time is each investor’s greatest asset for long-term success and investment growth.

Thank you for the ongoing opportunity to work on your behalf and best wishes for the Christmas and Holiday season!!

Did you know? Historically, the month of November is the strongest of the year, with December and January also generally providing better than average returns. It seems that with market trends more favorable again, a tailwind for markets might endure through the end of the year as investors often chase strong performance. Also, a frequent question following such a strong November – does it steal from December performance? No, not usually.

(1) Magnificent 7: Apple, Amazon, Microsoft, Nvidia, Tesla, Google/Alphabet, Meta and collectively account for over 28% of the S&P500 composition; the other 493 names are roughly 72%.

By Steve Henderly, CFA | Nvest Wealth Strategies, Inc.

Printer Friendly PDF: The Last Mile is Often the Longest – Dec23