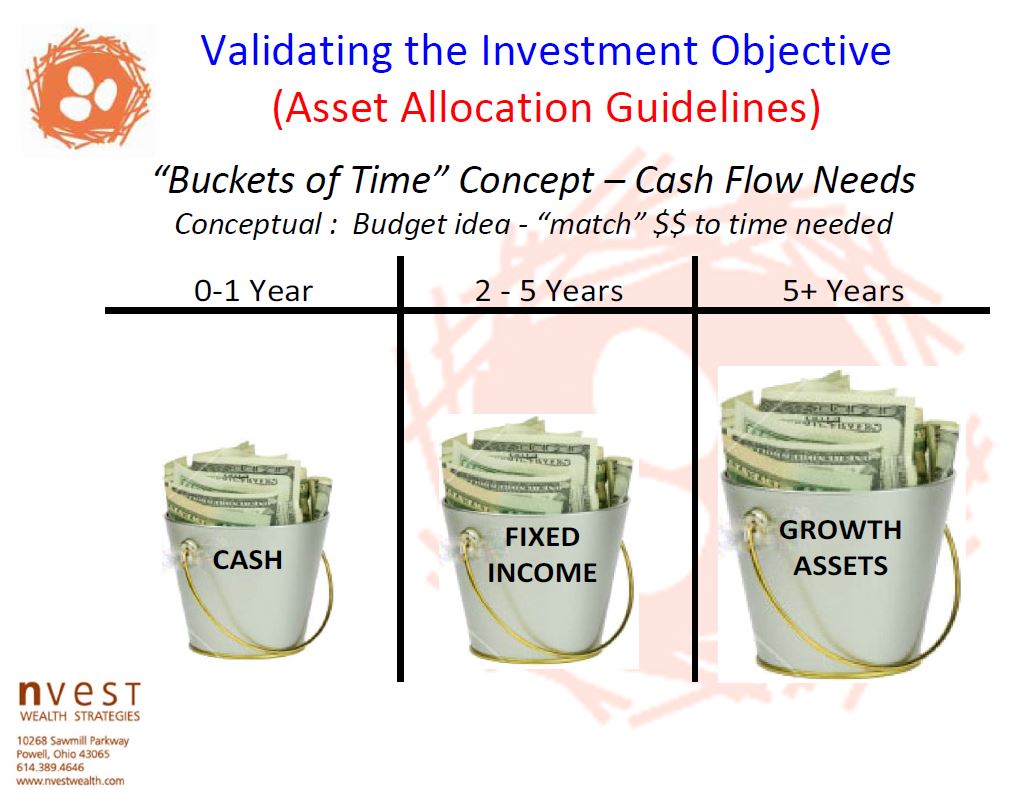

Perhaps the most unsettling aspect about 2022 is not the degree to which the stock market is experiencing pain (not that unusual), but it’s the “double whammy” of also seeing meaningful depreciation in traditional safe fixed income. A recent headline, “The worst year in US history for the 60/40 portfolio”, underscores there being no place to hide in this bear market. During these challenging days, we continue to encourage maintaining a longer-term perspective. One way to do that is recalling “buckets of time” investing. Our well-seasoned clients may recall our “buckets of time” framework to unemotionally establish the investment objective (asset mix) for each account. This process helps align a client’s time horizon and purpose to investing the account.

As we journey through the various stages of life – from being a “person at work” to a “person living off money at work”, and during other seasons (events requiring money) – the buckets of time approach may adjust the investment mix accordingly. This buckets of time approach advocates that individuals maintain short-term money needs in cash and attempt to “live life” (day-to-day, month-to-month) primarily at the bank; investable monies that exceed what is needed in 1 year or less; budgeting the monies needed in 2-5 years can be confidently invested in bonds; and the excess amounts are deemed to be 5+ year money that can be invested among growth-oriented assets (stocks, real estate, etc). History shows the chance of losing money in the fixed income (bond) “bucket” during 5 years is highly improbable; while the 5+ money invested in “growth” achieves higher long-term returns, which can “pour over” into other buckets to refill them, maintaining the investment objective (stock/bond mix).

With bonds experiencing their worst stretch in over 40 years, one may wonder – does the “buckets of time” approach remain appropriate in today’s market environment? From our perspective, the answer is a resounding YES. Keeping perspective on the purpose and time horizon for portfolios is intended to remove emotion from investing. The discipline of buckets of time investing does help remove emotion from making ill-advised timing decisions.

During this “goofy” time for bonds, we must avoid the temptation to assess their merit in the rearview mirror. Following the swift rise in yields, expected forward returns from bonds are higher today than they’ve been in a long time. Current Treasury yields are around 4%; these kinds of yields seemed improbable a year ago. Yet, these yields are much more normal by historical standards. For the first time in a long time you can earn meaningful yield in your portfolio with an asset that’s relatively safe. This higher yield rewards bond investors going forward. While stocks remain the best investment over the longer term to battle our dual enemies of inflation & taxes, the fixed income portion of portfolios can again add meaningful income to the 2-5 year “bucket” and provide significantly more stability than stocks (that’s diversification).

For those still unconvinced of the benefit of bonds (or the merit of “buckets of time”), be aware that after a -20% return for the 60/40 portfolio (a very rare occurrence), such a mix went on to produce double its normal return over the next 5 years on average (the interesting study can be found here: MarketWatch.com)

Maintaining a disciplined approach to portfolio management rewards investors time and time again. We are happy to meet anytime to share additional thoughts and color around this important topic, including a review of whether your “buckets of time” are still appropriately sized for each account’s anticipated time horizon and purpose.