We hope this note finds you and your family well and enjoying the beginning of Fall. Unfortunately, “enjoyable” is not a word we’d presently associate with the financial markets. The 3Q marked the first time since 1976 where both stocks and bonds were simultaneously negative 3 quarters in a row. As we interact with clients, some jokingly request that we not send this quarter’s update as they are doing their best to not focus closely. That may not be the worst strategy!

Our newsletter this quarter includes the following brief perspectives:

- “A Fresh Pair of Eyes” – 2022 remains all about rates (interest & inflation), and the dynamics are very different than when the year began.

- “Always Late” – What’s it like to always be late? Maybe we should ask the Fed. Recognizing that monetary policy always acts with a lag, it is understandable the market is concerned by the aggressive changes pursued over the last 9 months. Will the Fed go too far before we see the impact of their actions?

- “The Times They Are a Changing” – What’s the market saying about the future; what can help the markets stabilize and ultimately turn the negative trend around?

- “Buckets of Time – Dead, or Alive?” – With bonds experiencing their worst stretch in over 40 years, some may be wondering if the “buckets of time” approach remains appropriate in today’s environment.

The printer-friendly version of the newsletter, including benchmarking and widely held fund performance data, can be obtained here: printer-friendly PDF version.

With so many issues affecting the current investment climate, we hope that these updates are helpful. Please do not hesitate to call, email with questions, or to coordinate a time to visit together.

A FRESH PAIR OF EYES

The earliest attempts to create eyeglasses occurred in the 1200s. Can you imagine going through life with everything out of focus? Today, when we think of things out of focus, it’s pictures and videos. In the days before corrective lenses there was nothing that could be done if one was near or farsighted. It would be like watching an out-of-focus film every waking moment. Imagine trying to catch food for dinner or step on rocks to cross a stream; it could be challenging without help. Amazing how we often take for granted the significant health and medical/optical accomplishments that enhance our lives.

As investment reports are opened, it may feel appropriate to remove the glasses and avoid seeing any detail; close your eyes. September lived up to its often horrid reputation with the S&P500 declining -9.2%. And for the 3rd quarter, both stock and bond indexes lost roughly 5%. No place to hide so far during this bear market. While bonds are down roughly half as much as stocks YTD, they are not providing their usual benefit/hedge – now 3 consecutive quarters for both bonds and stocks producing negative total returns. That has not occurred since 1976 (187 quarters). There is no joy in achieving history with negative experiences.

This year remains all about rates, rates, rates… interest and inflation. The price pressure in stocks is a reflection of turmoil about high inflation and rising rates in the bond markets. The Fed raised rates 5 times during this year, with the last 3 being “triple-sized” 0.75% hikes; the Fed claims more rate hikes are coming. Central banks around the world are following the similar script – raising rates aggressively to battle high inflation that is broadening into “sticky” areas. Key question: will governments (central bankers and government policy makers) collectively do too much too fast and thereby create an economic challenge?

Do your eyes sometimes play tricks on you, on what you think you saw? If confusion sometimes sets in, like “what’s happening?” consider this thought from Matthew West’s “Wonderful Life” – “It’s a broken and beautiful; Gone mad and magical; Awfully wonderful life.” Are those lyrics relatable? Life events can create confusion; financial markets often create confusion. 2022 financial market action appears confusing and out of focus. For investors with experience, they understand confusion, particularly during storms cause loss; but it is only temporary IF you remain invested. The challenge is waiting, continuing to look with “eyes afresh” for indicators that components of confusion are lifting. Another quote also seems appropriate:

ALWAYS LATE

“Timebenders” struggle with punctuality. Every group knows one person who is “the late one.” Invariably, we all miss a deadline, miss an appointment; but repeatedly…? There are few habits as annoying as making others wait. How do others react to someone always being late? Perceptions of unpunctual people are almost always negative. Jokes are even shared that they will be late for their own funeral. To alter always being late, take the punctuality challenge – become disciplined at starting tasks or departing for appointments early, before due; and avoid trying to do that “one more thing” quickly (that’s me; stop).

So, what’s it like to be always late? Maybe we should ask the Fed (Chairman Powell)? Maybe it’s easy to look back and raise questions. Was there too much stimulus applied to boost the economy during Covid; was Fed accommodation of no/zero interest rates and QE too much and too long? Inflation is the product. Was the Fed perspective of “transitory” inflation a detrimental interpretation? Did “being late” make their next actions (reactions) late? Now, as inflation is proving “stubborn”, is the Fed acting from behind, trying to catch up? If so, will the Fed raise interest rates and initiate Quantitative Tightening that is too much, with the results not known until too late? Do government policies that alter spending, taxes, and regulation cloud tighter monetary policy and further raise odds the Fed is “late”? The Fed appears resolved to “wrestle inflation to the ground.” They are about 1% away from being “neutral” – where interest rates and core inflation are anticipated to be similar – around 4% to 4.5% (moving rates above that level would imply that policy is then restrictive). It’s probable that historians will debate how we arrived at this time in international finance, wherein interest rates were suppressed (zero) for nearly 10+ years. Is the bill for those years now coming due via higher interest rates and inflation?

The big challenge with Fed monetary policy is its lag effect. The impact of tight policy will not be fully known for 12 to 24 months. As the Fed institutes tight monetary policy to curb demand, creating time for supply shortages to catch-up, they will likely see inflation drop because economic growth declines. Some inflation components are already slowing; but wage, rent/housing inflation is sticky.

Ultimately, that will set up the historical pattern where interest rates will then be reduced, which on average occurred about 8 months after the Fed “paused” its rate increase campaigns. High interest rates tend to break a “weak link in the chain.” What will that “weak link” be this cycle? Perhaps it’s some over leveraged (too much debt) financial player(s) who will require financial reorganization. At that point, markets will message the Fed that actions were too much. When a “weak link breaks”, at that point the Fed is again “always late” and usually offers rescue by cutting interest rates. Significant bad events are often buying opportunities; often the start of a new bull market. Investors’ mood is pretty pessimistic and washed-out; maybe approaching exasperated. With the speed at which the markets (currencies, bonds, stocks, and etc) are moving, that point may not be too far away; avoid panic and don’t be late.

THE TIMES THEY ARE A CHANGIN’

What’s the market saying about the future? What can help the markets stabilize? What can turn the negative trend of the markets around?

It is not lost on us that this song by Bob Dylan may be the most referenced for financial market commentaries of any. But alas, “the times they are changing”; the investment landscape is in transition. The markets drop subtle clues which allow one to attempt to assemble a macro puzzle. I often claim to being a “jigsaw puzzle” maker; making a “financial markets puzzle” without a box top picture to show what it should look like. And, the jigsaw puzzle picture is never one that is viewed in total; the financial market picture is always evolving.

Stocks are known as leading indicators for the economy; leading the economy by 6 to 9 months on average. At the moment, market direction speaks of anticipated economic slowdown; maybe a recession (more a question of “when?” because they do happen). At some point while news is still negative stocks will begin a new rally and ultimately a new bull market; it will begin before economic news turns positive. The challenge: knowing when. No one can accurately forecast the “baddest” low point.

What can change the negative market trend; what can help the markets stabilize? Here are several macro items to watch:

- Inflation rates slowing year-over-year; moving toward the Fed’s 2% to 3% targets. It is believed that this will only be accomplished with some rise in unemployment to lessen inflationary wage pressures (“sticky” inflation). This would allow the Fed opportunity to pause from its recent rapid, large rate increases.

- Clarity about the Russia/Ukraine conflict, and easing of geopolitical tensions. Energy and food are presently being “weaponized”, disrupting supply chains and challenging efforts to curb inflation.

- Less political uncertainty in the US. Gridlock is often preferred by Wall Street because it reduces the speed at which policies (regulation, tax, spending) can change. The upcoming midterm election may usher in such a period of gridlock relative to today.

- Slowing economic growth will repair supply chain challenges.

Because inflation is the biggest concern for businesses, citizens… and the market currently, good economic news is viewed by the markets as “bad” because it means the Fed must continue to be aggressive with its tightening monetary policies. Alternatively, bad economic news is viewed as “good” because it suggests the Fed may be nearing its end point of raising interest rates. During “bad” news moments, the stock/bond market will rebound; rallies will appear like this is the new advance. Or, “good” news will cause prices to fall/drop. Unfortunately, single data points can cause fast market swings up or down (volatility). We’re not rooting for “bad” news because it implies broadening pain in everyday life; yet it does signal progress is occurring to reduce inflation and inflation expectations.

Bottoming in the financial markets takes time. It requires testing the lows. Investors may be conditioned to see a low and believe a “V-shaped” recovery will occur. But rallies off the low are often capped. “Dead cat bounces” are those rallies that are broken by “good” news (viewed as bad) and they are unable to break through the “ceiling” where the last market high existed; they’re capped. Testing the lows sometimes looks more like a “U” (long, drawn out recovery) or a “W” (up/down/up/down/up) pattern over time. Lows create a “floor” for testing upon which the market base is formed, and from which a new bull market ultimately develops. Time is a key requirement – it just takes time which is most difficult to quantify.

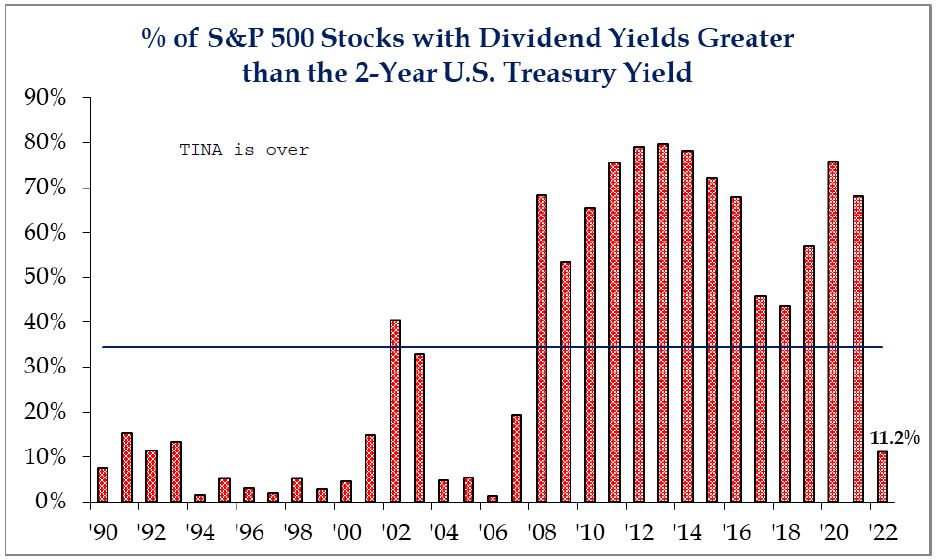

If the “times are changing”, …If the investment landscape is changing in 2022 and into 2023, what investments will do well? Given the degree of inflation (high prices from years of low interest rates and government stimulus) that is built into the system, it may be that the next bull market foundation will be built on solid fundamentals. TINA (“there is no alternative”) promoting own “all” stocks is over (see chart at the end of these articles). High interest rates are providing income investors a new opportunity to manage portfolio risk. Bonds, now sporting higher and more normal yields, are the most attractive in years. They will provide better diversification benefits too. Because higher yields will slow economic growth, owning stocks that provide increasing (growing) dividend returns may become favorites. High-risk assets, non-dividend paying stocks with fast growing revenues (and if they are with high debt leverage) – “Fang & Friends”, and even Bitcoin – are unlikely to be what new market leaders will look like. Further, index strategies may not prove rewarding because they own everything – both the well capitalized and overleveraged names without discretion. Actively managed funds/ETFs that utilize a proven investment process should be better positioned to generate attractive total returns because they can select those investments that meet quality criteria.

degree of inflation (high prices from years of low interest rates and government stimulus) that is built into the system, it may be that the next bull market foundation will be built on solid fundamentals. TINA (“there is no alternative”) promoting own “all” stocks is over (see chart at the end of these articles). High interest rates are providing income investors a new opportunity to manage portfolio risk. Bonds, now sporting higher and more normal yields, are the most attractive in years. They will provide better diversification benefits too. Because higher yields will slow economic growth, owning stocks that provide increasing (growing) dividend returns may become favorites. High-risk assets, non-dividend paying stocks with fast growing revenues (and if they are with high debt leverage) – “Fang & Friends”, and even Bitcoin – are unlikely to be what new market leaders will look like. Further, index strategies may not prove rewarding because they own everything – both the well capitalized and overleveraged names without discretion. Actively managed funds/ETFs that utilize a proven investment process should be better positioned to generate attractive total returns because they can select those investments that meet quality criteria.

During changing times, there will be stress, concern, and worry because of the unknown. No one knows the time when “feeling” better will occur. Caution is appropriate, but it is unwise to make radical changes; small adjustments are not inappropriate and we pursue them. Wise investors understand that time is their greatest ally. Investors must stay the course, or for certain, they will be “Always Late” (like the Fed appears today). Being late as an investor means selling after the storm is underway, and not being invested when the market turns/rebounds. It will turn. Late investors will miss a lot. Their subsequent investment return experience is low and uninspiring. Historical stock and bond returns are 10% and 5.5% respectively. That only occurs when an investor stays invested through the market ups/downs; through recessions which do occur – it’s just a matter of when (time). Rip Van Winkle did investing right; he took a nap for 20 years to awaken with the explanation, “WOW”!! Van Winkle no doubt, awoke to a different looking time. [He earned historical returns. He did not “see” all the up/down worry of the markets.] The strategy is simple, but it sure isn’t easy!

Articles written by Bill Henderly, CFA | Nvest Wealth Strategies, October 4, 2022.

“TINA” No More?

For the decade-plus since the Great Financial Crisis (‘07-09 bear market), stocks benefited from a phenomenon referred to as the “TINA” factor. TINA, an acronym meaning “There is No Alternative” to stocks – that whether one was looking for growth or yield, stocks were the only traditional asset class of appeal. Now with rates more historically normal, only 11% of the S&P500 stocks provide a yield greater than Treasuries. Today, both bonds and stocks offer many portfolio benefits.