Buying USA

This commentary offers three ideas with a common theme centered on valuation. We monitor various economic, market and political research to understand the current financial market backdrop. We hope these topical writings share our thinking about investing in today’s environment.

Don’t Fight the Fed

Investing in early 2023 remains challenging. A disconnect between the financial markets and the economy currently exists. The US economy started 2023 with momentum – employment continues to be robust, with recent stats showing a historic low rate of unemployment at 3.4%. The burst of momentum is occurring in an unbalanced economy. This backdrop boosted investor confidence toward investing in risk assets, like common stocks with the S&P500 advancing +6.3% in January. Then, as economic news became too good in February, stock market returns turned negative as wiser investors understand “good news is not good news” when the Fed is raising interest rates to slow high inflation; “good news” is viewed as “bad news”. The S&P slipped -2.4%, slimming the YTD return to +3.7%. Both stock and bond values retreated in February believing the Fed would need to 1) raise rates further and 2) keep them higher for longer. The Fed is unable to declare “mission accomplished” fighting inflation. And until that time, there remains risk to economic growth, company earnings, and financial markets. Investors should expect market action to remain bumpy, as this is typical during the bottoming process of bear markets. February and YTD portfolio returns, and the returns for different asset classes, reveal disconnect; it really appears beneath the surface as a tug-of-war.

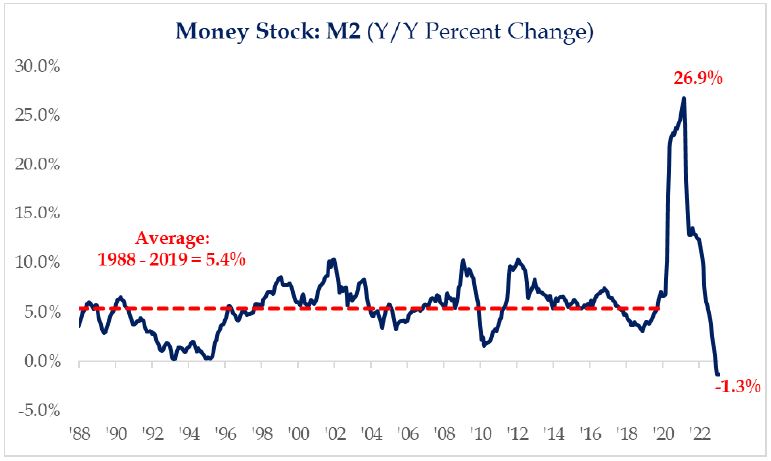

So, which is better – fight the Fed, or fight the tape (market)? Neither option seems all that appealing, especially in the short term. In an unbalanced economy where one area is benefitting and others are faltering, rising interest rates make economic growth uncertain. There exists today a widely-held perspective that a recession could develop. Monetarists reflect on the speed of money supply growth (M2). Recall during the Great Lockdown in 2020 (due to COVID), money supply grew at almost 27% to finance an economy that was arguably closed. Adding Zero Interest Rate Policies (ZIRP) created a huge policy mistake – INFLATION. To reverse inflation, the Fed (and other central bankers) ended accommodative policy actions – aggressively raising interest rates and reducing M2 growth, now contracting at -1.3%. Negative M2 growth will slow the economy over time. It also suggests the stock market will not receive excess money flows as a shrinking supply is inadequate for economic growth. Monetary policy acts on the economy with a 6 to 9 month lag; can be longer and variable. The time lag depends on other factors, like how long inflation remains sticky and other government policy mistakes (raising taxes and/with continued spending, and burdensome regulations).

Negative M2 growth will slow the economy over time. It also suggests the stock market will not receive excess money flows as a shrinking supply is inadequate for economic growth. Monetary policy acts on the economy with a 6 to 9 month lag; can be longer and variable. The time lag depends on other factors, like how long inflation remains sticky and other government policy mistakes (raising taxes and/with continued spending, and burdensome regulations).

Financial market values are largely influenced by interest rates and money flows. “Don’t fight the Fed” is one of those forever market axioms. Investors should always be aware of Fed monetary policy direction. If you don’t and invest without Fed understanding, you can experience uninspiring returns. In essence, be careful – invest with care while retaining a long-term focus on financial goals and the Fed.

Time to Buy Bonds?!

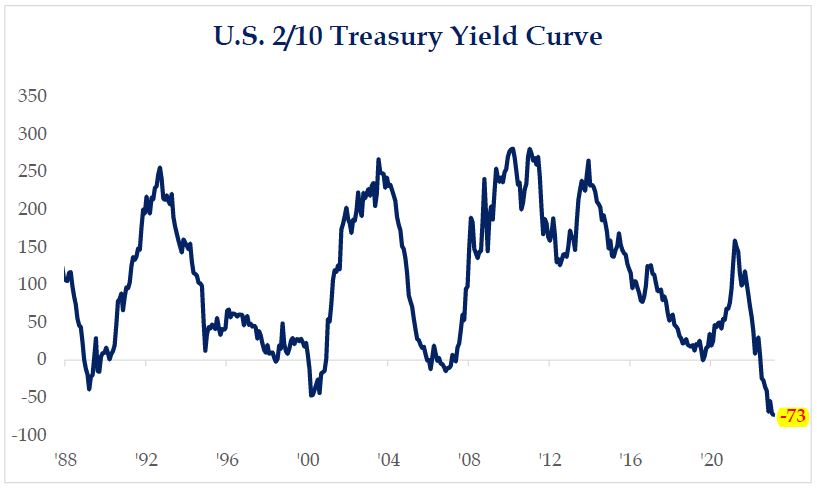

Bear market drawdowns are always a function of time and price. Unfortunately, neither is easy to quantify. It’s even more challenging with an inverted yield curve that exists today. An inverted yield curve (see chart on pg 2) where bonds maturing in the next year or two provide higher yields than longer maturities is abnormal. Usually, long bond maturities pay higher yields than short maturities. An inverted curve also, like high inflation, signifies government policy mistake. Inverted yield curves often, not always, suggest a recession may occur in the future and slower economic growth is very probable.

During times of slower economic growth conditions, where inflation is taking its toll on valuations, investing with care is appropriate. Today, there exists opportunity to earn attractive yields from shorter maturity bonds. Shorter maturities (1-year Treasuries) are nearing 5% and are subject to less price volatility than longer maturity or lesser quality bonds. Bond yields are rising in most other major countries as well. Today, bonds offer “value” compared to the past 10+ years when accommodative monetary policies and ZIRP were in play; plus bonds provide renewed diversification benefits for stocks. If you consider that stocks still sport valuations of 18x earnings (P/E ratio), a multiple still toward the higher-end of historical range, then owning bonds provides both return and diversification benefits worth pursuing during the short term.

Don’t be surprised if interest rates stay higher than many investors expect. Prior to 2008, the 10-year US Treasury yield exceeded the rate of inflation 91% of the time. With the current 10-year Treasury yield at almost 4% and the latest CPI inflation reading at 6.4%, it’s not unreasonable to think that yields could move higher and stay elevated, even as inflation continues to decline (perhaps more slowly from here). As this historical relationship reoccurs, bond credit quality is important for investors, because borrowers (individuals and businesses) will experience new financing challenges with higher rates – money is no longer nearly “free” to anyone who can “fog a mirror”. At the moment, short maturity bonds offer attractive return during a confusing market backdrop. Short maturity bonds offer attractive yields (better “value”) and diversification benefits not available in 2022.

Remember though, history shows that stocks and growth investments are the best fighters against inflation and taxes (investor’s two enemies), and provide the best growth prospects of capital over time. Buying right is critical to earning attractive long-term return experiences. That means, investors must capitalize on what the market is providing at any point in time.

Let’s Get Political (not Physical*)

COVID “booster shots” are rolling off. The governments’ fiscal and monetary stimulus policies are not providing the “fertilizer” to economic growth. They were a major contributor to sticky inflation, and are now causing many to feel “poorer” even with low unemployment and higher wages. Government policy must always be careful to not go too far in its pursuits to make things “better.” It seems that even Newton’s third law of physics applies: “for every action, there is an equal and opposite reaction.” From an economic perspective, government cannot fully “manage” the economy by spending and/or taxing without creating future unintended experiences on its citizens. There is no free lunch in life; also true with investing.

Would you buy the USA if it were a stock? Let’s get political (not physical*); and review post mid-term election years. The US debt to GDP ratio is projected to average 106% over the next 10 years, up from 102% just 9 months ago. The governments CBO recently shared these statistics as Congress addresses the US debt ceiling this summer. Given high spending levels during COVID and the recent addition of $22 trillion more debt budgeted into law from FY22-33, the US debt to GDP ratio is forecast to jump from 97% in FY22 to 118% in FY33. US debt to GDP will be close to 130% after 10 years. This year, higher mandatory government spending (Social Security, Medicare and Medicaid due to inflation) along with higher interest expenses from Fed rate increases place the deficit trend line on a new higher path.

The USA is entering a period of forced austerity due to rising interest costs. For the past 30 years, the US was able to increase spending and cut taxes without an increase in its debt servicing cost. Those days are most likely over. The debt service cost will average almost 17% of tax revenues over the next 10 years up from 13% in May 2022. Financial markets seem to react negatively and forces austerity on policymakers once that rate rises above 14%. Interest costs are projected to exceed defense spending by 2028. If so, it could “crowd out” spending on things like national security during a time of increasing geopolitical tensions. Also, many states will begin to see their tax revenues decline as COVID relief to citizens and governments concludes; those states with high income taxes and citizen migration are already pursuing tax increases to shore up budgets. Policymakers will address difficult choices in raising the debt ceiling – continue spending to meet “demands”, or cut spending, and/or raise taxes. These are difficult choices during a time when the Fed is engineering slower consumer spending and softer economic growth to fight inflation.

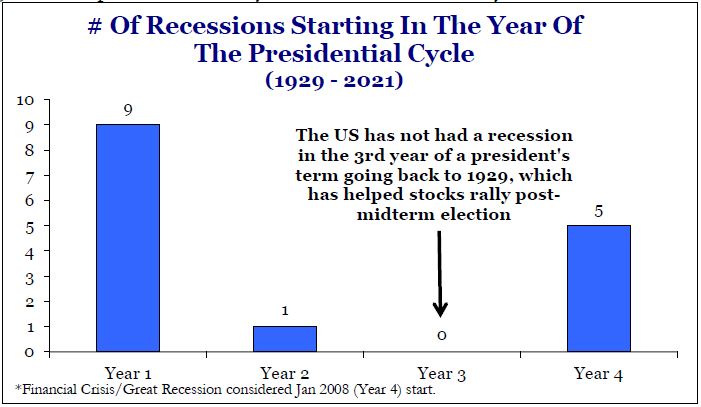

One more thought: history shows the 3rd year of a President’s term is usually good for financial markets. Yet 2023 seems unlikely to match historical experience. Amazingly, the US economy never experienced a recession during the 3rd year because both monetary and fiscal policies boost growth ahead of a presidential election year; stocks advanced to higher levels and valuations. But, given structural issues – the lag effects of monetary policy and pending austerity challenges relating to the debt ceiling – economic growth appears constrained.

One more thought: history shows the 3rd year of a President’s term is usually good for financial markets. Yet 2023 seems unlikely to match historical experience. Amazingly, the US economy never experienced a recession during the 3rd year because both monetary and fiscal policies boost growth ahead of a presidential election year; stocks advanced to higher levels and valuations. But, given structural issues – the lag effects of monetary policy and pending austerity challenges relating to the debt ceiling – economic growth appears constrained.

Given the choice, would you buy the USA if it were a stock? It currently seems expensive, valued in total. But, not all stocks are unappealing; stock “A” may be more appealing than stock “B.” In other words there are attractively valued areas of the US market such as dividend paying stocks whose characteristics are comparable to short maturity bonds (short duration). Inversely, fast growing stocks – not paying dividends or with high valuations, and/or with high levels of debt – appear risky in this environment. Keep in mind, bear markets are a function of time and price; it corrects excesses (over-valuation) and risk, and often provides new leaders for the next bull market. Today, foreign stocks offer better valuations than the USA. Most of us usually feel more “comfortable” owning American (many, many attractive attributes). Again, we advocate Investing with care for the long term. After all, the markets offer future rewards not available last year.

*Olivia Newton-John recorded a song in 1981, “Let’s Get Physical” – seemed catchy relative to current political climate.

Printer-Friendly PDF of “Buying USA” – March Commentary

Bill Henderly, CFA | Nvest Wealth Strategies, March 2, 2023