Ever hear someone say “horsefeathers”? It’s peculiar, so when it’s exclaimed a puzzled look often occurs. “Horsefeathers” is politely spoken when something did not go right – like I made a bad pickleball shot or missed an easy putt; or a goofy mistake occurred that could be anticipated. It’s amusing that I used this word for years and decades. As I considered using “horsefeathers” for the title of this commentary, I’m taken back by its age and origin – originating from the 1900s. It was used in several film gags from the Marx Brothers’ (Groucho, Zeppo, Harpo, and Chico) in “Fun in Hi Skule” (1932). “Horsefeathers” is slang for nonsense, foolishness, rubbish; indicates disbelief; like “Oh, that’s just horsefeathers, and you know it.” Sometime in the future maybe I’ll share about Mr. Kadiddledopper, or the idea of “enjoying your snooze cruiser.” [NOT, you may develop thoughts that I’m crazy.]

“Horsefeathers” is my mild expression for the 2022 financial market experience resulting from COVID government responses. For most of the year, investing proved disappointing. Yet, the final 3 months of most calendar years is a historically attractive season where the stock market often enjoys its best days. Even if this month provides a very strong performance, it’s highly unlikely the stock or bond market can fully recover the drawdown from earlier this year. Investors must be careful thinking the recent 4Q rebound is the start of a new bull market; don’t create false expectations. During October, the S&P500 stock index recovered +8.1%; November added another +5.6%, bringing the 2-month advance to +14.4%. That’s encouraging… but it still seems most likely to be a relief rally occurring during the best seasonal time of the year. If so, this will be the 3rd “dead cat bounce” rally this year (a Wall Street term based on the perhaps morbid rationale that “dead cats” don’t bounce very high). That’s because the current market backdrop needs much repair before one of these rallies turns into the next new bull market. Assuredly, a new bull market will develop; we just don’t know when. Investors should expect continued market action to be churning – up/down – this volatility creates frustration, maybe even irrational exasperation that provokes many to finally “give up” (that point is the bottom).

Client portfolios, owning various mutual funds and exchange traded funds (ETFs) produced attractive November and two-month rebounds. YTD portfolio returns improved albeit still reflect one of the worst years since 1935; diversifying with stocks and bonds did not hedge risk like historical experience.

In November market areas leading the rebound were starkly different from the leaders of the last few years. On top of that, prior leaders (FAANG+ stocks, which also comprise an outsize weight in market indexes like the S&P500) still appear the most at risk. But the tone and leadership is changing. During November, some economic stats and Fed comments suggested progress in the inflation fight. The Fed may be approaching a terminal rate on interest hikes. Bonds recovered nicely during the month, but still report one of their worst annual performance experiences ever. Stocks that pay dividends (growing, not yield only) and value are doing better than growth (including tech stocks focused on fast growth). And, who would guess that foreign stocks were the best performing area during November (hey, Russia/Ukraine and other geo-political issues are still evolving)?

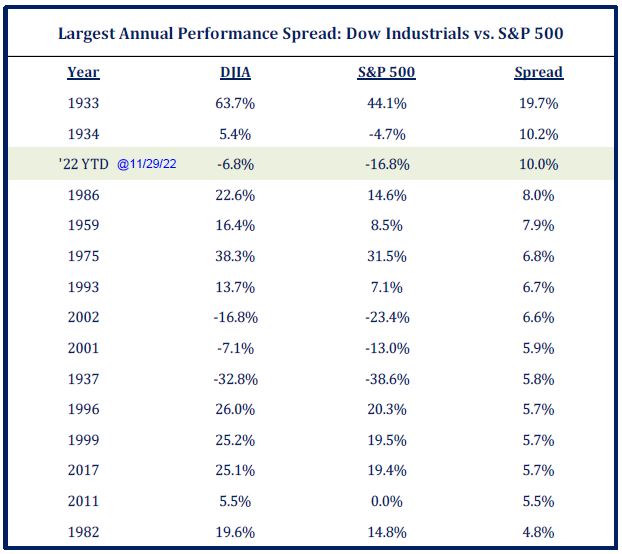

Not to get too technical about the market tone change… Did you notice the YTD performance of the Dow Jones Industrial Average (DJIA, an index comprised of the 30 largest US companies) is off -2.9% while the S&P500 is down -13.1% (following the attractive +3% day on 11/30); the NASDAQ (where many tech stocks reside) is worse yet at -25.6% through November 30? The DJIA is beating the S&P500 by +1000 basis points YTD; that’s big!  The best performing sector, all year for most any time interval is Energy; traditional energy. The energy sector is also interesting to watch as it is an indicator for economic growth (falling off when recessions appear probable). In early December when labor stats were strong with wage increases +5%, that “good” news suggests more aggressive Fed rate increases that would slow the economy and elevate recession worries. Some may recall the “Dogs of the Dow”, an older themed investment approach that own the10 lowest priced stocks with the highest dividend yields (in the DJIA) purchased for one year; those names are performing better than the S&P500 this year. The “average” quality stock is doing better than FAANG+ and the big indexes – S&P500 and NASDAQ. Unfortunately there are still not enough “average” stocks advancing at the same time – a few new “generals” (leaders) and not many “soldiers” to create a bull market that defeats the bear.

The best performing sector, all year for most any time interval is Energy; traditional energy. The energy sector is also interesting to watch as it is an indicator for economic growth (falling off when recessions appear probable). In early December when labor stats were strong with wage increases +5%, that “good” news suggests more aggressive Fed rate increases that would slow the economy and elevate recession worries. Some may recall the “Dogs of the Dow”, an older themed investment approach that own the10 lowest priced stocks with the highest dividend yields (in the DJIA) purchased for one year; those names are performing better than the S&P500 this year. The “average” quality stock is doing better than FAANG+ and the big indexes – S&P500 and NASDAQ. Unfortunately there are still not enough “average” stocks advancing at the same time – a few new “generals” (leaders) and not many “soldiers” to create a bull market that defeats the bear.

“Horsefeathers!” It feels ‘nonsensical” this year because the Fed was late responding to “transitory” but sticky inflation; they were “too wise” maintaining zero interest rates and QE monetary policy while government fiscal policy provided huge stimulus spending during the COVID Great Lockdown and thereafter. As we all know, inflation exploded. Thus, the biggest change to the financial market backdrop is now, occurring in 2022 – the transition from zero interest rates and Quantitative Easing (QE) to Quantitative Tightening (QT). Central bankers are choosing to fight inflation, even if it means denting the economy and financial markets. In essence, the era of free money is over. This means that access to capital will be rationed and its cost more expensive. The potential slowing of globalization, call it de-globalization, could keep inflation, interest rates, and prices of materials & products higher, with a persistent shortage of labor. Service costs could be higher too. Energy could remain a “captive” of geo-political warfare and sticky inflation component.

What does all this mean for the economy and financial markets? While the economy was decidedly stronger than financial markets (returns) in 2022, we wouldn’t be surprised if the inverse occurs in 2023 – that the market outperforms the economy. That’s because markets are forward-looking and usually lead the economy. Markets know that monetary policy acts on the economy with a long and variable lag. It takes time for monetary policy to affect the economy and even longer to affect inflation. Most Fed watchers expect monetary policy will remain tight – keeping interest rates higher for longer; no start-stop-start again process like in the 1970s. The current yield curve is the most inverted in 40 years at -0.80%, meaning the 2-year Treasury offers +80bps higher interest than the 10-year Treasury.  That creates an unusual chart pattern because long maturity bonds usually yield higher rates than short. It means a policy mistake and often signals an economic recession is likely. That said, if recession occurs it will not be a surprise as it is already most investors’ base case and already being priced into the market. Be assured that if a recession occurs, it will whack inflation; recessions always stun inflation, but also bring declines in corporate profits and stock valuations. Good news though, it appears inflation peaked this late-summer. The Fed’s restrictive policy is generating its desired effect, and will take more time to curb sticky components of inflation (rents, wages, and services). Consumers and wage increases are the Fed’s biggest hurdles to reducing inflation.

That creates an unusual chart pattern because long maturity bonds usually yield higher rates than short. It means a policy mistake and often signals an economic recession is likely. That said, if recession occurs it will not be a surprise as it is already most investors’ base case and already being priced into the market. Be assured that if a recession occurs, it will whack inflation; recessions always stun inflation, but also bring declines in corporate profits and stock valuations. Good news though, it appears inflation peaked this late-summer. The Fed’s restrictive policy is generating its desired effect, and will take more time to curb sticky components of inflation (rents, wages, and services). Consumers and wage increases are the Fed’s biggest hurdles to reducing inflation.

Because of these factors (yield curve, and sticky inflation components), it is our belief that we are enjoying a nice seasonal bear market rally (began October 12th). Rallies in this bear market can continue until an economic stat is released that indicates the economy or employment remains too strong to tamp inflation to desired levels. Good economic news is still “bad news” at the moment, as it means the Fed must remain restrictive, pursuing a tight monetary policy path. On the positive side, Fed rate increases provide investors (today) the best bond yields in a decade. Bonds offer attractive return and diversification benefits in client portfolios while this bear market backdrop evolves.

We don’t need to be reminded that bear markets are painful. Yet we should recall that they create opportunities. History reveals that investors improve their future return experiences by carefully embracing risk at a time when others are selling. When a bear market bottom hits or a new bull market begins (which NO one can pinpoint), the forward 12 month and 36 months returns are +39% and +16% (annualized), respectively. Investors don’t want to miss these return experiences, even when current news is bad. That’s because the financial markets are forward looking by 6 to 9 months.

Important: please keep the main thing, the main thing. That’s straight from the “horse’s mouth”!! So why “Horsefeathers?” We all know horses can’t fly and don’t have feathers; neither do bulls or bears, or dogs. And “dead cats don’t bounce”. Experience should remind us that no one knows things changed… until change continues. Then in hindsight we exclaim, “Horsefeathers; I missed it!” The main thing today is stay invested. AND, most important…

Enjoy a Merry Christmas! So amazing that Christmas started over 2000 years ago, at which time the count of years was reset; and even today the world for this one day seems quiet and reflective. Christmas is a special event! Enjoy a very Merry Christmas with your loved ones and friends!

Printer-Friendly PDF Version, including Style and Investment Objective returns for the month.

Bill Henderly, CFA – December 7, 2022